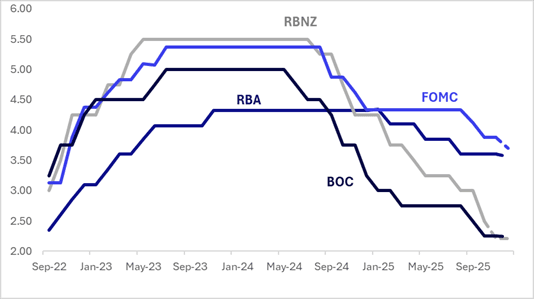

STIR: $-Bloc Pricing Shows Mixed Performance Over Past Three Weeks

Interest rate expectations across the $-bloc have seen mixed performance over the past 3 weeks, with Australia (+25bps) and the US (+15bps) firmer, but New Zealand (-2bps) and Canada (-4bps) little changed.

- In Australia this week, the RBA Monetary Policy Board unanimously left rates at 3.6%, as was widely expected, and sounded generally cautious. With risks "in both directions" and the degree of restrictiveness difficult to assess, the Board doesn't have a stance. Neither a cut nor a hike was discussed.

- Staff trimmed mean projections were revised higher over the rest of 2025 and 2026, with the important 2q/2q annualised rate returning to 3% in Q1 and 2.6% in Q4, which may allow a rate cut from May if this eventuates. Decisions remain highly data dependent and will be made on a "meeting-by-meeting basis".

- In the US, markets appear to be still adjusting to the surprise from the October 29 FOMC meeting, where Chair Powell opened the post-meeting press conference by underscoring the Committee’s divisions on the path ahead: "In the Committee's discussions at this meeting, there were strongly differing views about how to proceed in December. A further reduction in the policy rate at the December meeting is not a foregone conclusion, far from it. Policy is not on a preset course."

- The next key regional event is the RBNZ policy decision on November 26. 28bps of easing is priced for November, with a cumulative 36 bps by February 2026.

- Looking ahead to December 2025, current market-implied policy rates expected easing is as follows: US (FOMC): 3.70%, -17bps; Canada (BOC): 2.24%, -1bp; Australia (RBA): 3.56%, -4bps; and New Zealand (RBNZ): 2.21%, -29bps.

Figure 1: $-Bloc STIR (%)

Source: Bloomberg Finance LP / MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

RBNZ: Larger Cut Gives Sluggish Economic Recovery Extra Boost, Easing Bias

The MPC discussed cutting the OCR by 25bp or 50bp and all members agreed the latter was appropriate given material spare capacity in the economy. Given that this is likely to persist for some time and that while the economy has begun to recover it remains lacklustre, further cuts bringing policy into stimulatory territory are likely. In line with this it said that “the Committee remains open to further reductions in the OCR”.

- The discussion included both 25bp and 50bp cuts. Arguments for 50bp to 2.5% included “prolonged spare capacity”, downside risks to growth and therefore inflation, moderation in domestic inflation resulting in greater confidence inflation is contained, and risk that households and businesses are being particularly cautious. The MPC wanted to send “a clear signal” to support the economy.

- Monetary policy lags, “signs of recovery”, time to ensure inflation returning to 2%, upside inflation risks from “constrained supply and cost pressures” and that signalling further easing for November would ease financial conditions argued for a more cautious 25bp cut.

- The MPC’s inflation concern appeared to shift this month. In August, it said it could ease policy further “if medium-term inflation pressures continued to ease as expected”, whereas this month it seemed more concerned with undershooting the target mid-point stating it “remains open to further reductions … for inflation to settle sustainably” near the 2% mid-point over the medium-term.

- It now expects inflation around 2% over H1 2026 rather than “by mid-2026” which may reflect its marginal revision to spare capacity and risks following the 0.9% q/q GDP contraction and recent modest activity data. Q2 GDP was impacted by a “large seasonal balancing item”, which the RBNZ expects to be reversed.

- There will be no press conference or forecast update today.

BONDS: Richer After RBNZ Cuts 50bps

NZGBs are 3-7bps richer after the RBNZ cut 50bps to 2.50%. Key paragraphs from the RBNZ statement include:

- "There are upside and downside risks to the inflation outlook in New Zealand. Cautious behaviour by households and businesses could slow the economic recovery, reducing medium-term inflation pressure. Alternatively, higher near-term inflation could prove to be more persistent. "

- "The Committee remains open to further reductions in the OCR as required for inflation to settle sustainably near the 2 percent target mid-point in the medium term."

- "The case for reducing the OCR by 50 basis points emphasised prolonged spare capacity and the associated downside risk to medium-term activity and inflation. Domestic inflationary pressures have continued to moderate as projected, giving the Committee more confidence that inflationary pressures are contained. Some members continue to put relatively more weight on the risk that excess precaution by households and businesses and, therefore, subdued economic activity and employment persists. A larger reduction in the OCR could mitigate this risk by providing a clear signal that supports consumption and investment."

- Swap rates are 5-6bps lower on the day.

- RBNZ dated OIS pricing has shunted 15bps softer across meetings. 34bps of easing had been priced for this meeting. A cumulative 62bps of easing had been priced by November 2025 versus 77bps now (including today’s mive).

AUSSIE BONDS: Holding Richer On A Data-Light Day

ACGBs (YM +1.5 & XM +3.0) are holding modestly stronger in today’s data-light session.

- Cash US tsys are flat to 1bp cheaper, with a steepening bias, in today's Asia-Pac session after yesterday's modest rally.

- Cash ACGBs are 1-3bps richer with the AU-US 10-year yield differential at +23bps.

- The latest ACGB Mar-36 auction saw strong demand, with the weighted average yield coming in 0.22bps through prevailing mid-yields, according to Yieldbroker, continuing the trend of firm pricing at recent ACGB auctions. Moreover, the cover ratio nudged higher to 3.4917x from 3.3111x.

- Bidding at today’s auction faced an outright yield that was roughly 10-15bps higher than the previous auction level and about 20bps below the late February peak.

- The bills strip is flat to +2 across contracts.

- RBA-dated OIS pricing is little changed across meetings today. A 25bp rate cut in November is given a 40% probability, with a cumulative 14bps of easing priced by year-end.