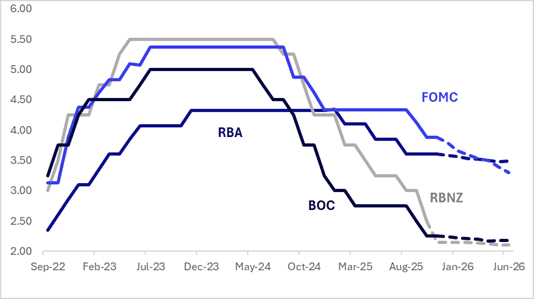

STIR: $-Bloc Pricing Out To Jun-26 Little Changed Over The Past Week

Interest rate expectations across the $-bloc out to mid-2026 were broadly stable over the past week, with all net moves confined within a narrow ±2bp range.

- The main event was Wednesday’s release of the FOMC Minutes from the October meeting (link). While views within the Committee “differed strongly,” the minutes indicated that only a minority may push for a follow-up rate cut in December.

- This aligns with MNI’s assessment that, based on post-meeting commentary, most of the broader Committee is leaning toward holding rates in December — though that does not necessarily imply that pro-cut voices form a majority within the 12-member voting group.

- The next key regional event is the RBNZ policy decision on November 26. 27bps of easing is priced for November, with a cumulative 35bps by February 2026.

- Looking ahead to June 2026, current market-implied policy rates expected are as follows: US (FOMC): 3.30%, -58bps; Canada (BOC): 2.18%, -7bp; Australia (RBA): 3.49%, -11bps; and New Zealand (RBNZ): 2.10%, -40bps.

Figure 1: $-Bloc STIR (%)

Source: Bloomberg Finance LP / MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA PRESS: China Needs New QFLP Reforms - Expert

China should introduce new Qualified Foreign Limited Partner (QFLP) regulation given that the mechanism now extends to mezzanine financing, distressed assets and real estate, according to Zhao Bingyin, equity partner at Zhong Lun (Shanghai) Law Firm. Speaking at a Lujiazui Financial Salon focused on deepening QFLP pilot reforms in Shanghai, Zhao said regulators should ease entry requirements for traditional equity investment while maintaining higher thresholds for asset-heavy sectors such as infrastructure and non-performing loans (NPLs). He also called for better alignment between QFLP and emerging initiatives, including real estate private funds and asset securitisation pilots. These improvements, Zhao added, would help ensure that Shanghai remains at the forefront of QFLP innovation nationwide.

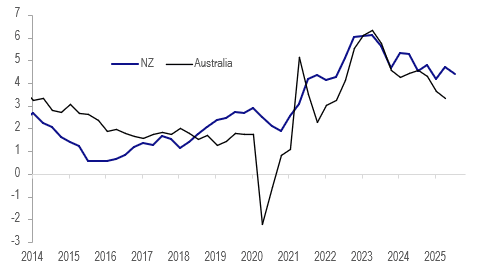

AUSTRALIA: NZ CPI Data Suggests Stable Q3 Australian Core

Q3 NZ CPI was released this week and given high correlations it has some information for Australia’s CPI out on 29 October. The RBNZ’s sector factor model measure of core was stable at 2.7% y/y in Q3 signalling that Australia’s may also remain around Q2’s 2.7%, which is consistent with monthly data. NZ’s domestic-related non-tradeables and services annual inflation moderated while goods and tradeables were higher.

Australia vs NZ underlying CPI y/y%

- NZ services inflation moderated to 4.4% y/y in Q3 from 4.7% while it picked up to 1.2% q/q from 1.1%. There is around an 85% correlation with Australia’s headline annual services inflation and 50% with the quarterly rate. Even if there is an increase in Australia’s quarterly rate in Q3 from Q2’s 0.7%, the 3.3% annual rate should moderate given it rose 1.1% q/q in Q3 2024.

- NZ’s services inflation has been running well ahead of Australia’s and has seen little disinflation since the start of 2024, which may be warning.

- It is worth noting though that the RBA focuses on market services (ex volatile items) which rose 0.6% q/q & 2.9% y/y in Q2. Governor Bullock has stated that the RBA was concerned about some of the components and sticky services prices overseas.

- NZ non-tradeables moderated 0.2pp to 3.5% y/y in Q3 and Australia’s could also ease given the correlation is over 90%. The two have been trending lower for around 2 years.

- NZ goods and tradeables inflation picked up in Q3, which given the global nature of many and high correlations Australia could see this too.

- Australia’s headline CPI continues to be impacted by temporary government electricity rebates and so it is currently not helpful to look at the relationship with NZ.

Australia vs NZ services CPI y/y%

Source: MNI - Market News/LSEG

CNH: USD/CNY Fixing Edges Up, Fixing Error Close To Unchanged, CNH Steady

The USD/CNH fix printed at 7.0954, which is modestly up on yesterday's print (which was a fresh YTD low). The fixing error is close to unchanged at -297pips, so it didn't widen despite the firmer USD index levels through Tuesday. USD/CNH was last 7.1265/70, unchanged for the session. Today's fixing is unlikely to give fresh downside impetus to the pair. Broader USD sentiment is a touch softer with yen modestly outperforming the G10 space (amid a slight downtick in both US equity futures and Tsy yields).