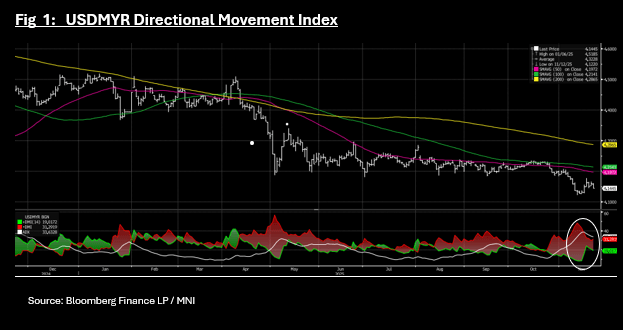

MYR: Directional Momentum Index Suggests USD/MYR Downtrend Weakening

Nov-21 03:56

- USDMYR is strong today with the strongest gains of regional peers of +0.38% taking the Ringgit to 4.1445.

- Today's gains aren't enough to erase a potential 5-day loss; currently at -0.306%.

- The Ringgit is no longer oversold on the Relative Strength Index and maintains its position below all major moving averages.

- The Directional Movement Index however suggests that the momentum in the rally may be weakening. To interpret the Directional Movement Index (DMI), look at the relationship between the +DI (positive directional indicator) and -DI (negative directional indicator) lines to determine trend direction. Currently +DI (green line) is below -D1 (red line)supports the downtrend however the ADX (average directional index) (white line) above the two suggests that the strength of the current downtrend is weakening.

- As expectations for FED cut at the December meeting continue to diminish, the momentum behind the Ringgit has been moderating. The FED December decision could be the catalyst for the next move for USDMYR, given limited key data releases between now and then.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

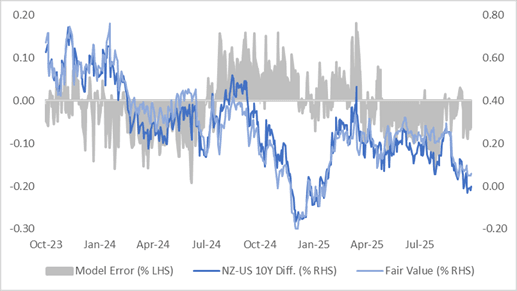

BONDS: Closed With A Bear-Flattener, NZ-US 10Y Diff Looks Too Low

Oct-22 03:51

NZGBs closed showing a bear-flattener, with benchmark yields flat to 2bps higher.

- On a relative basis, the NZGB 10-year has underperformed its US tsy counterpart, with the NZ-US yield differential 2bps higher at flat. (see chart)

- A simple regression of the 1Y3M forward swap spread against the 10-year yield differential over the past 18 months suggests the current differential is 6bps below its estimated fair value of +6bp

- “NZ's central bank considered Hayley Gourley as a potential board member and recommended that option to the government before she was appointed to the MPC.” – BBG

- “NZ is relaxing climate reporting rules due to concerns over the cost to businesses, with companies listed on the NZX only having to provide disclosures if their market capitalisation is NZ$1 billion or more.” - BBG

- Swap rates closed little changed.

- RBNZ dated OIS pricing closed little changed across meetings. 25bps of easing is priced for November, with a cumulative 39bps by February 2026.

- The local calendar will be empty until next Tuesday's release of Filled Jobs data for September.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 4.50% May-30 bond, NZ$175mn of the 4.25% May-36 bond and NZ$50mn of the 5.00% May-54 bond.

Figure 1: NZ-US 10-Year Yield Differential

Source: Bloomberg Finance LP / MNI

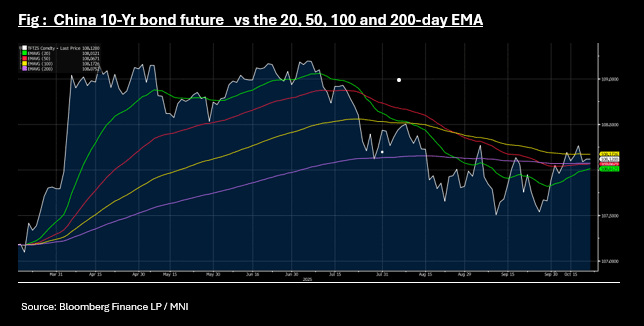

CHINA: Bond Futures Sideways on Quiet Day

Oct-22 03:25

- Given a modest injection in this morning's OMO, bond markets remain subdued today even as equity markets give back some of the gains from recent days.

- The 10-Yr bond future is flat at 108.12 remaining at the mid-point between the 100-day EMA and the 200-day EMA.

- The 2-Yr bond future is down -0.02 at 102.34 pushing further below all major moving averages.

- The 10-Yr CGB is stronger today, down -1bp at 1.82%

JGBS: Market Reacts Positively To Min. Kiuchi Comments

Oct-22 03:23

At the Tokyo lunch break, JGB futures are flat compared to the settlement levels but well off session lows.

- Headlines have crossed from Japan's Growth Strategy Minister Minoru Kiuchi. Kiuchi stated that the focus now is compiling an economic stimulus package, albeit with one eye still on fiscal discipline (DJ) (and diverse funding sources). Various ministers are being consulted, with a focus on helping tariff impacted sectors. Kiuchi stated that no timeline is set for when the economic package will be compiled. Early focus for markets for the new Takaichi regime is fiscal stimulus, in terms of size and how it will be funded (particularly with parallels drawn with the Abenomics-like policy set ).

- Cash US tsys are slightly richer in today’s Asia-Pac session after yesterday’s modest bull-flattener.

- Cash JGBs are flat to 2bps richer across benchmarks, with the 7-year and 20-year outperforming.

- The benchmark 30-year yield is 0.4bp lower at 3.125% versus the session high of 3.148%. Notably, the current yield is more than 20bps below the cycle high of 3.351%, hit shortly after Takaichi was announced as the LDP leader.

- Swap rates are little changed.

Trending Top

Mar-27 20:13