EU COMMUNICATIONS: Deutsche Telekom: H125 Results

(DT ; Baa1pos/BBB+pos/BBB+)

Headline results broadly in line with consensus. CFO was lower YoY due to FX and WC phasing albeit is still higher on a YTD basis. German weakness is weighing on the equity with -1.3% org growth and soft KPIs including a second quarter of negative broadband net adds and just 185k branded mobile net adds (from 311k in Q224).

- Q2 Revs: €28.7bn (+1% YoY, in line). YTD: €58.4bn (+4% YoY).

- Q2 adj-EBITDAal: €11bn (+2% YoY, 1% beat). YTD: €22.3bn (+5% YoY).

- Q2 CFO: €9.8bn (-5% YoY, 4% miss). YTD: €20.9bn (+5% YoY).

- Q2 Cash CapEx: €3.9bn (+5% YoY, 1% miss). YTD: €8.2bn (-2% YoY).

- Q2 FCFal (ex divs, spectrum): €4.9bn (-7% YoY, 1% miss). YTD: €10.5bn (+18% YoY).

- Reported net debt 2.51x from 2.78x at FY24.

- FY guidance tweaked higher.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUD: AUDJPY Approaching March Highs Following RBA Surprise

- Despite Monday’s steady move lower for AUDUSD as renewed tariff concerns filtered through to higher beta FX, today’s RBA surprise and subsequent spike higher to 0.6558 fully reversed the week’s decline. The pair has since settled around the 0.6540 mark amid a more stable equity backdrop, and it is worth noting we have ~400mln of 0.6545 expiries rolling off at today’s NY cut.

- This AUDUSD bullish trend set-up is maintained, with the latest pullback considered technically corrective. Moving average studies remain in a bull-mode position, highlighting a dominant uptrend, and scope is still seen for a climb towards 0.6603 next, the Nov 11 high. Initial firm support to watch is 0.6472, the 50-day EMA.

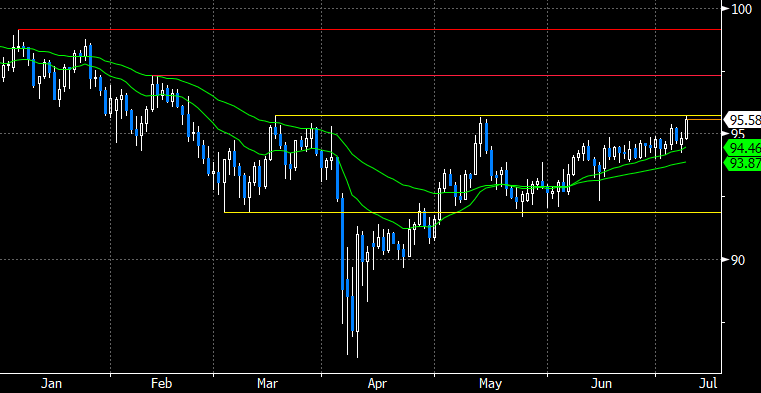

- Standing out on the chart is AUDJPY, which returns to an important area of resistance around 95.75 which aligns with the March and May highs from earlier in the year. Should major equity indices positively navigate the first major tariff deadline this week, the cross could see further upside targeting a move towards the February highs at 97.33. Uncertainty regarding a US/Japan trade deal and a market that remains long JPY could strengthen a short-term extension of the rally.

- Concerns over stubborn domestic inflation led the RBA board to keep the cash rate at 3.85%, in a 6-3 split decision that defied market pricing. Governor Bullock was unapologetic following the call, noting the Reserve had limited ability to influence market pricing ahead of the decision, largely due to the new board voting structure.

Source: Bloomberg Finance L.P. / MNI

GILTS: Bear Steepening Extends

Weakness in wider core global FI markets has pushed gilt futures through lows from last Wednesday & Thursday, leaving bears focused on nearby Fibonacci support (91.50), followed by the Feb 2 low (91.16).

- A relatively heavy session for global sovereign supply, the EU escaping higher U.S. tariffs (at least for now), a delay of the broader U.S. tariff deadline, further steepening on the JGB curve and a hawkish RBA outcome have all factored into this morning’s weakness.

- Yields 3-7bp higher, curve steeper.

- 10-Year yields registered a fresh July high (4.640%), with focus now on the June 9 high (4.673%).

- 2s10s though the month-to-date closing high, last 74.5bp, ~10bp off April’s intraday year-to-date high.

- 5s30s set for a fresh year-to-date closing high, last 14.06bp. Focus on the April intraday high at 147.2bp.

- There was no immediate reaction to the OBR’s Fiscal Risks and Sustainability Report, although the details won’t do much to alleviate long-term worry surrounding the UK’s fragile fiscal state and well-documented productivity headwinds.

- This morning’s GBP900mln sale of the 1.875% Sep-49 I/L gilt passed smoothly.

- BoE-dated OIS shows 52bp of cuts through year-end after failing to push meaningfully beyond 55bp in recent weeks. Over 80% odds of a 25bp cut are still priced through the August MPC, with such a step still fully discounted come the end of the September MPC.

BoE Meeting | SONIA BoE-Dated OIS (%) | Difference vs. Current Effective SONIA Rate (bp) |

Aug-25 | 4.003 | -21.4 |

Sep-25 | 3.948 | -26.9 |

Nov-25 | 3.781 | -43.7 |

Dec-25 | 3.696 | -52.2 |

Feb-26 | 3.566 | -65.1 |

Mar-26 | 3.535 | -68.2 |

BELGIUM T-BILL AUCTION RESULTS: Short/Long TCs

| Maturity | Oct 16, 2025 | Jul 9, 2026 |

| Amount | E1.2bln | E1.801bln |

| Target | E2.6-3.0bln | Shared |

| Previous | E1.153bln | E1.162bln |

| Avg yield | 1.898% | 1.910% |

| Previous | 1.911% | 1.907% |

| Bid-to-cover | 2x | 1.82x |

| Previous | 1.44x | 1.97x |

| Previous date | Jul 01, 2025 | Jul 01, 2025 |