US: Democrats Eying Another Special Election Overperformance In New Jersey

Apr-15 17:51

Analysts expect another strong Democratic performance in a House Special Election tomorrow in New Je...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: EGBs-GILTS CASH CLOSE: Yields Track Oil Prices Lower

Mar-16 17:50

European yields pulled back Monday, with curves bull flattening.

- Gains were largely steady throughout the session, crescendo-ing into a low in yields a little after 2pm London time.

- Once again, yields moved in lockstep with oil prices, including a simultaneous intraday bottom for both.

- Multiple oil/Mideast conflict headlines drove the decline, including signs of another vessel crossing through the Strait of Hormuz.

- Yields closed a little off the lows (10Y Germany 3bp off lows, UK closer to 5bp).

- Gilts outperformed Bunds across the curve. Periphery/semi-core EGB spreads tightened, led by higher-beta BTPs and GGBs.

- Tuesday's schedule includes German/Eurozone ZEW surveys for March.

- European focus for the week is on Thursday's ECB and BOE decisions.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 3.8bps at 2.404%, 5-Yr is down 3.9bps at 2.6%, 10-Yr is down 4.1bps at 2.942%, and 30-Yr is down 2bps at 3.513%.

- UK: The 2-Yr yield is down 4.3bps at 4.087%, 5-Yr is down 5.6bps at 4.283%, 10-Yr is down 6.1bps at 4.762%, and 30-Yr is down 6.3bps at 5.432%.

- Italian BTP spread down 2.9bps at 77.7bps / Greek down 3.1bps at 77bps

FOREX: USD Index Tracking Energy Prices Lower, AUD and NZD Recover Firmly

Mar-16 17:44

- Despite a gap higher at the open, crude futures have traded with a bearish tilt on Monday, erasing a solid portion of the late upswing on Friday. More favourable dynamics for risk overall have weighed on the US dollar, with the DXY currently half a percent lower as we approach the APAC crossover and back below the 100 mark.

- Both AUD and NZD are the notable outperformers, rising a punchy 1.15% and 1.35% respectively. For AUDUSD, this brings spot back into the mid-point of the most recent range as we approach Tuesday’s RBA decision, where surveyed estimates lean in favour of a 25bp hike to 4.1%. Short-term technical parameters appear well defined, with key support at 0.6963, the 50-day EMA, while the bull trigger stands at 0.7187, the March 11 high.

- Elsewhere in the majors, EURUSD has been steadily grinding higher and is now testing back above the 1.1500 handle, a key breakdown point last week. EURUSD price action should continue to be reflective of energy prices, however, short-term positioning could accentuate the price action as fresh shorts are squeezed further.

- USDJPY has seen more moderate downside on Monday as markets remain cautious on potential intervention. Japan's Finance Minister Katayama said authorities are ready to take bold steps on FX if necessary, reiterating rhetoric used in advance of rate checks this January.

- With spot closing above the 159.45 January highs last Friday, this means that risk/reward of long positions in the pair appear increasingly unattractive. Above the psychological 160.00 level stands the July 8 2024 low of 160.26, while to the downside, the 20-day EMA intersects at 157.22.

- Elsewhere, slightly softer Canadian CPI data did little to move the CAD needle, as USDCAD edged a little further below 1.37 and back into its short-term technical trading range.

- Aside from the RBA decision, the calendar is light with German ZEW, US weekly ADP and pending home sales the notable releases.

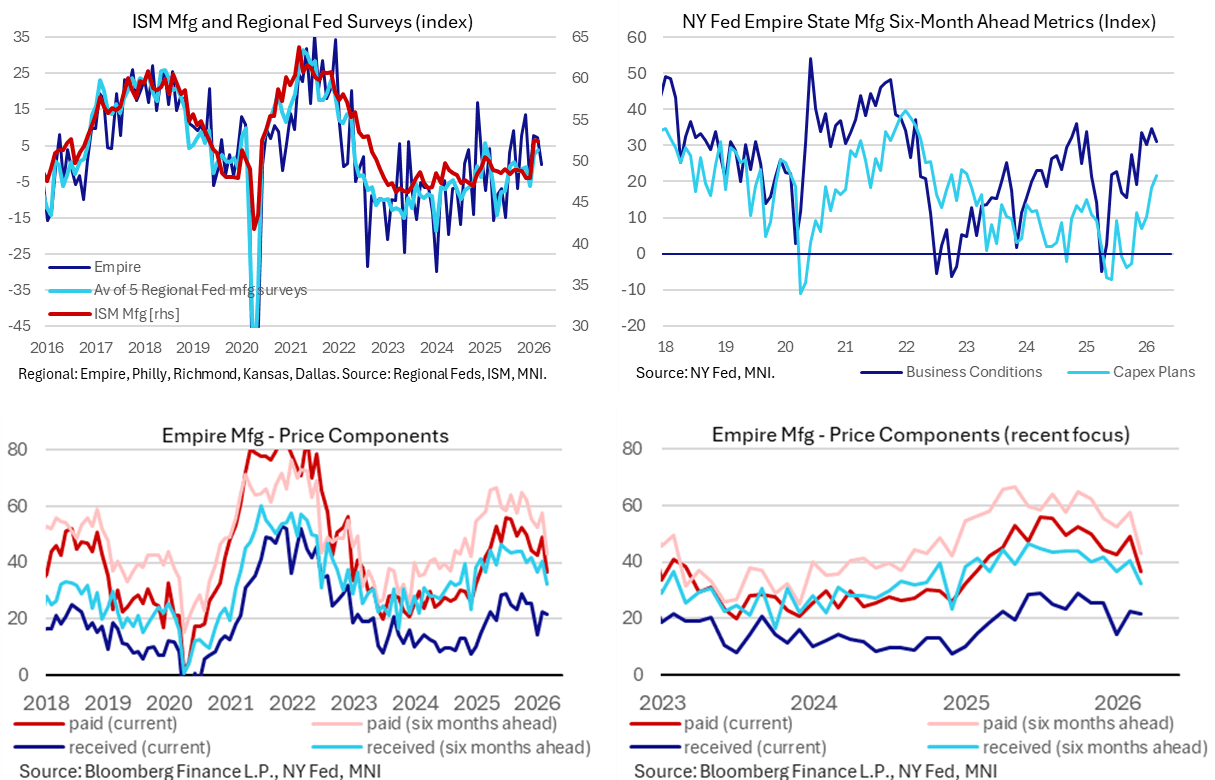

US DATA: First Regional Fed Mfg Survey For March Avoids Renewed Price Pressures

Mar-16 17:39

The Empire manufacturing survey offered a slightly softer than expected start to the March regional Fed surveys with a neutral reading after two modest expansionary readings. Capital expenditure plans were most encouraging, at their highest since early 2023, whilst price components saw a notable cooling with prices paid at its lowest since Jan 2025.

- The headline general business conditions index dipped to -0.2 (cons 3.9) in Mar from 7.1 in Feb and 7.7 in Jan. The 13.5 from Nov 2025 remains its most recent peak having previously hit 16.8 in Nov 2024 with the US presidential election.

- The breakdown was a little more encouraging as shipments declined (-6.9 after -1.0) but new orders at least improved a little (6.4 after 5.8) along with employment (5.8 after 4.0).

- The six-month ahead general business conditions index also softened slightly to 31.0 although that followed February’s 34.7 which had been its highest since Mar 2022.

- Probably the most encouraging aspect of the report was the capex plans diffusion index firming further to 21.6 from 18.2 for a fresh high since early 2023.

- Switching to price components, prices paid slipped from 49.1 to 36.6 for its lowest since Jan 2025 whilst six-month ahead prices paid also fell from 57.6 to 43.1 for the lowest since Dec 2024. The survey was collected Mar 2-9 but energy price shifts following the US-Israel-Iran war starting Feb 28 have mainly been in fuels rather than natural gas which appears to have limited its impact on industry judging by this anecdotal regional evidence.

- Prices received saw a smaller move, to 21.4 from 22.2, to keep within recent ranges but prices received also pushed to new recent lows with 32.4 after 40.3 in Feb.