OIL: Delayed Reaction To Headlines May Explain Oil Dip

Perhaps some delayed reaction to earlier headlines when it comes the move lower in oil: * Iran Inte...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

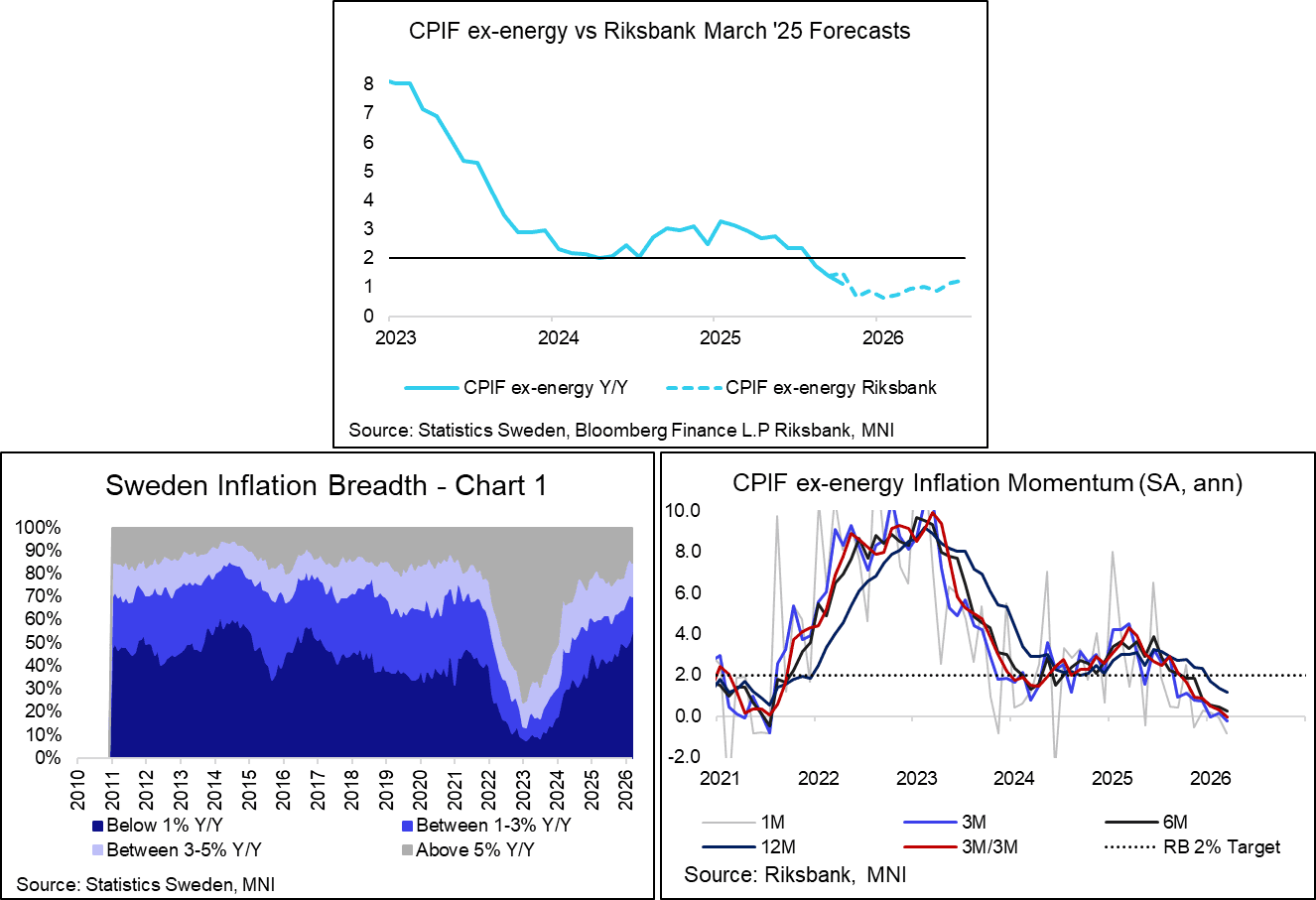

SWEDEN: Final March Report Confirms Lower Underlying Inflation Pressures

Swedish CPIF ex-energy inflation confirmed flash estimates in March, with the 1.13% Y/Y print well below the Riksbank’s 1.48% March MPR projection. We estimate seasonally adjusted underlying inflation at -0.07% M/M (vs 0.00% prior), which pulled 3m/3m momentum negative. The share of CPIF subcomponents with annual inflation rates below 1% also rose to 55% (vs 50% prior). The details confirm that underlying inflation pressures were low heading into the Iran war, which should mean any hawkish Riksbank reaction should be less aggressive than the ECB, for example. Headline inflation was 1.6% Y/Y vs 1.7% prior, with lower electricity prices offsetting higher fuel prices.

- As foreshadowed in the flash release, food inflation was soft at 0.48% Y/Y (vs 1.95% prior). A reminder that the temporary food VAT tax cut comes into effect from April, which is expected to pull this component down further.

- Services inflation was 1.94% Y/Y (vs 2.14% prior). We estimate seasonally adjusted services at 0.01% M/M (vs 0.15% prior), pulling 3m/3m momentum down to 0.24% (vs 0.71% prior), the lowest since August 2021.

- This was driven by recreational services (1.20% Y/Y vs 1.79% prior), accommodation services (-0.03% YY vs 2.59% prior) and insurance and financial services (3.36% Y/Y vs 3.48% prior). Other services, including volatiles such as package holidays and airfares, accelerated relative to February. Rent payments were broadly steady, with an uptick in actual rents offset by a decline in imputed rents.

- Goods ex-food inflation was -0.83% Y/Y (vs -1.26% prior). Seasonally adjusted goods were 0.05% M/M (vs -0.12% prior), with 3m/3m momentum still negative at -0.30% (vs -1.70% prior).

Clothing and footwear inflation was 1.61% Y/Y (vs -0.33% prior), while furnishings and household equipment was -3.55% Y/Y (vs -3.23% prior). Accelerations in vehicle inflation was seen alongside decelerations in recreational goods and personal care goods.

WTI TECHS: (K6) Monitoring Support

- RES 4: 126.49 - 1.618 proj of the Mar 10 - 23 high-low price swing

- RES 3: $123.68 - High Jun 14 ‘22 (cont) and a key resistance

- RES 2: $120.00 - Psychological round number

- RES 1: $117.63 - High Apr 7 and the bull trigger

- PRICE: $97.34 @ 07:23 BST Apr 14

- SUP 1: $91.05 - Low Apr 8

- SUP 2: $86.79 - 50-day EMA

- SUP 3: $75.64 - Low Mar 10

- SUP 4: $69.00 - Low Mar 2

Recent weakness in WTI futures is for now, considered corrective. The contract traded through the 20-day EMA, at $98.00. Attention for now is on support at the 50-day EMA, at $86.79. A clear break of the 50-day average is required to highlight a stronger short-term reversal. On the upside key resistance and the bull trigger has been defined at $117.63, the Apr 7 high. Clearance of this hurdle would confirm a resumption of the uptrend.

RIKSBANK: Bunge Does Not Rule Out Either March MPR Alternative Scenario

Riksbank Bunge speech summary here

- "How great the impact will be on inflation depends on how long the war lasts, how rapidly production in the region can be resumed and how companies and households react to the situation. All of this is very difficult to assess at this point in time, which made it reasonable to leave the rate unchanged at our last meeting"

- "If supply shocks are limited, they will not necessarily require a tighter monetary policy, as inflation disregarding the war is low to begin with. However, there is a risk of price increases spreading more widely in the economy, which is something we need to monitor closely."

- "“As I discussed at our most recent monetary policy meeting, this [the developing and volatile ceasefire situation] could lead to a need for either a higher or a lower policy rate than in our main scenario and I rule out neither alternative."