US: DefSec Hegseth Discusses Reconciliation 3.0 w/Senior House Republicans

Jun-11 15:30

Politico reports: https://x.com/meredithllee/status/2065080673648484506?s=20, "A group of senior Hou...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

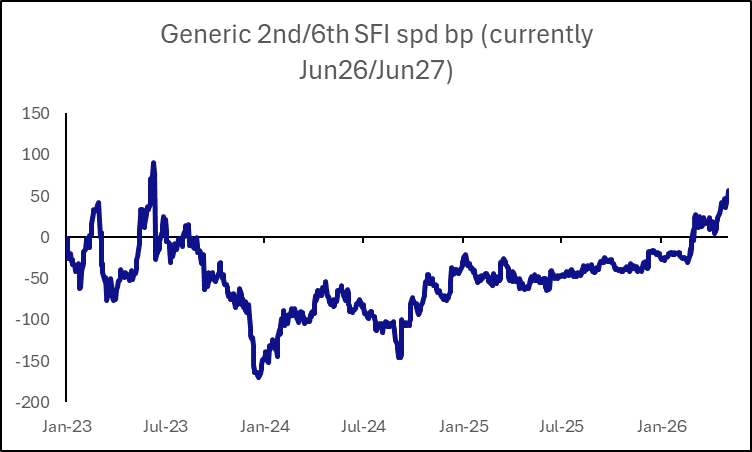

STIR: SFI Jun-26/Jun-27 hits cycle highs as political and energy risks mount

May-12 15:28

- The SFI Jun-26/Jun-27 spread has hit new highs over 55bps and could remain elevated as markets increasingly perceive persistent risks around UK energy-driven inflation and political instability, despite relatively fragile macro fundamentals.

- We had previously suggested that downside risks for the differential appeared more prevalent as the Bank of England seeks clarity on second-round dynamics, with rates already restrictive, labour market slack growing, and growth softening. However, the ongoing US/Iran impasse and the threat that a shift of power from PM Keir Starmer to a successor could play out slowly—amid fears the government may shift further to the left—may act as a brake on any near-term correction in the spread.

- Nevertheless, the differential is arguably now discounting a significant amount of negative news. Viewed on a generic basis, it has reached its highest levels since mid-2023, when UK interest rates rose for a 13th consecutive time to 5% amid peak anxiety about sticky wage and services inflation.

- Overall, we believe high commodity prices are a necessary, but not sufficient, condition for the BoE to hike in June. The MPC appears to be prioritising price-based rather than wage-based second-round impacts; consequently, the emphasis will be on forward-looking measures, such as the Decision Maker Panel (DMP) and Agents’ reports, rather than AWE data in the near term.

Markets will watch for continued increases in "own price" and 1-year ahead CPI expectations, while any rise in 3-year ahead CPI or wage growth expectations would likely be viewed as a more significant catalyst. Concurrently, any notable upside surprises in services or non-energy CPI categories relative to BoE forecasts would heighten the probability of a June hike.

Source: Bloomberg Finance LP, MNI

CAD: USDCAD Extending Winning Streak, Probes 50-Day EMA Resistance

May-12 15:25

- The Canadian dollar is performing relatively better than G10 counterparts on Tuesday, as the weaker risk/equity backdrop is potentially offset by the firmer oil price impulse. With that said, USDCAD’s 0.3% advance today looks set to extend a winning streak to five days, as the pair increases its recovery from the May lows to 1.2%.

- Despite this rally, the USDCAD trend condition remains bearish, and the latest recovery appears corrective. Resistance is being tested at 1.3711, the 50-day EMA, of which a clear break is required to signal a possible S/T reversal. Conversely, a resumption of weakness would pave the way for a move back towards 1.3526, the Mar 9 low and the next key support.

- CIBC stated they see scope for a retest of 1.3720 resistance as USD risk premia rebuilds modestly. That said, they have revised their USDCAD profile lower through year-end. CIBC pencil in a two-big-figure decline from Q3 to Q4 (1.36 to 1.34), reflecting a Fed cut not currently priced and a late-H2 Canadian recovery that could reopen the door to BoC hikes in 2027.

- Scotiabank believe CAD is holding up a little better than its core currency peers with the help of firmer commodity prices. Their fair value model reflects some minor weakening in factors driving the CAD, nudging spot’s equilibrium estimate marginally up to 1.3550 this morning. Scotia think USD gains may be capped in the low 1.37 zone absent a further deterioration in sentiment.

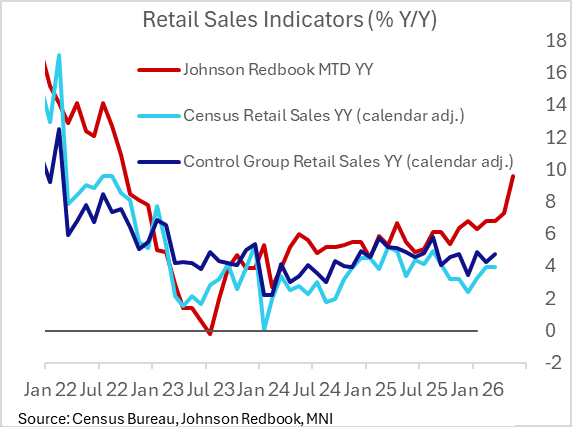

US DATA: Redbook Retail Sales Soaring, Boosted By Higher Prices

May-12 15:15

Retail sales started May on the front foot, with the Johnson Redbook index up 9.6% Y/Y through the week ending May 9. This would be up from the 7.3% recorded in April and easily the highest since September 2022.

- The acceleration in Redbook sales the last 2 months (was between 6-7% for 7 out of the 8 prior months) comes against the backdrop of accelerating inflation on the conflict in the Middle East, which is pushing up nominal series but not necessarily going to be reflected in volumes.

- Chicago Fed CARTS's ex-autos retail sales estimate for April is +1.1% M/M nominal but +0.3% real, after March's +1.9% M/M but -0.1% real; we get April's Census Bureau report Thursday (+0.7% ex-auto M/M expected, +0.4% Control Group).

- The Redbook anecdotes intriguingly eye potential positive impact for retailers from tariff refunds, following the Supreme Court's striking down of IEEPA levies: "As warmer temperatures spread across the country and graduation shopping season approached, stores reported increased sales of seasonal items, including apparel, footwear, and outdoor merchandise. Mother's Day drove notable buying activity in jewelry, cosmetics, flowers, cards, and small appliances. Despite the sales boost, annual growth rates remained unaffected because Mother's Day fell at the same time as the previous year, mirroring Memorial Day's pattern, which falls in the final week of May. The first wave of tariff refunds is expected to be sent out to businesses this week, and some companies might use these funds to restock inventories or lower prices, potentially impacting future sales trends."