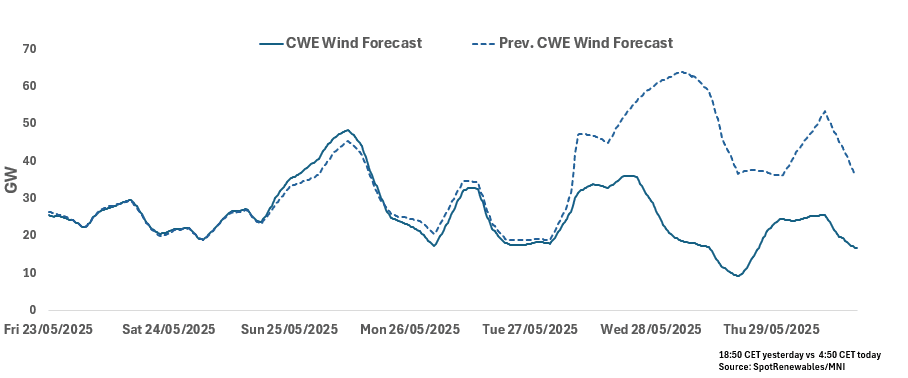

RENEWABLES: CWE Morning Wind Forecast

See the latest CWE Wind forecast for base-load hours from this morning for the next seven days. CWE wind forecast has been revised down over 26-28 May to be between 19-23% load factors.

CWE Wind for 23-29 May

- 23 May: 25.31GW

- 24 May: 23.79GW

- 25 May: 38.86GW

- 26 May: 23.98GW

- 27 May: 25.97GW

- 28 May: 20.77GW

29 May: 21.19GW

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BRENT TECHS: (M5) Corrective Cycle Still In Play

- RES 4: $77.75 - High Jan 20

- RES 3: $76.26 - High Feb 20

- RES 2: $69.95/75.47 - 50-day EMA / High Apr 2 and a bull trigger

- RES 1: $68.14 - High Apr 17

- PRICE: $66.67 @ 07:06 BST Apr 22

- SUP 1: $62.00/58.40 - Low Apr 10 / 9 and the bear trigger

- SUP 2: $58.85 - 2.000 proj of the Feb 20 - Mar 5 - Apr 2 price swing

- SUP 3: $56.89 - 2.236 proj of the Feb 20 - Mar 5 - Apr 2 price swing

- SUP 4: $55.00 - Round number support

Brent futures continue to trade above the Apr 9 low and maintain a firmer short-term tone. For now, the latest bounce is considered corrective and this is allowing a recent oversold condition to unwind. The primary trend direction remains down and a resumption of weakness would open $56.89, a Fibonacci projection. On the upside, initial firm resistance to watch is seen at $68.14, the Apr 17 high. Resistance at the 50-day EMA, is at $69.95.

SWEDEN: LFS Data Volatile, But Suggests Labour Market Should Strengthen Ahead

Overall, the LFS and PES (released last week) data suggests the Swedish labour market has passed its weakest point, and should start to strengthen alongside the broader economy through the rest of 2025 - assuming past (and potentially future) rate cuts and increased fiscal spending can offset some of the negative direct and indirect impact of US tariffs.

- The Swedish monthly LFS survey is a volatile release, meaning more emphasis should be placed on trends (e.g. 3mma’s) rather than single-month figures.

- In March, the seasonally adjusted unemployment rate fell 8 tenths to 8.1%, the largest one-month fall since July 2023. The three analyst estimates submitted to BBG were 8.5%, 8.7% and 9.2%. In Q1, the unemployment rate averaged 8.9%, below the Riksbank’s 9.1% March MPR forecast, and still heavily impacted by January’s lurch higher to 9.6%.

- The size of the labour force was essentially flat in March, meaning the fall in unemployment was mostly attributed to a rise in employed persons.

- 3m/3m employment growth was 0.4% (vs 0.3% in February), the highest rate since August 2024. The 3mma employment rate ended Q1 at 68.9%, above the Riksbank’s 68.7% projection.

GOLD TECHS: Bulls Remain In The Driver’s Seat

- RES 4: $3600.0 - Round number resistance

- RES 3: $3578.0 - 2.000 proj of the Dec 19 - Feb 24 - Feb 28 swing

- RES 2: $3547.9 - 1.764 proj of the Feb 28 - Apr 3 - Apr 7 price swing

- RES 1: $3499.0 - 1.618 proj of the Feb 28 - Apr 3 - Apr 7 price swing

- PRICE: $3495.0 @ 07:12 BST Apr 22

- SUP 1: $3331.5 - Low Apr 21

- SUP 2: $3163.5 - 20-day EMA

- SUP 3: $3167.8 - High Apr 3 and a recent breakout level

- SUP 4: $3033.3 - 50-day EMA

The trend needle in Gold continues to point north and this week’s fresh cycle highs confirm a resumption of the primary uptrend. The yellow metal has traded to another fresh all-time high. Note too that moving average studies are unchanged, they remain in a bull-mode position highlighting a dominant uptrend. The next objective is $3499.0, a Fibonacci projection. Initial firm support lies at 3163.5, the 20-day EMA.