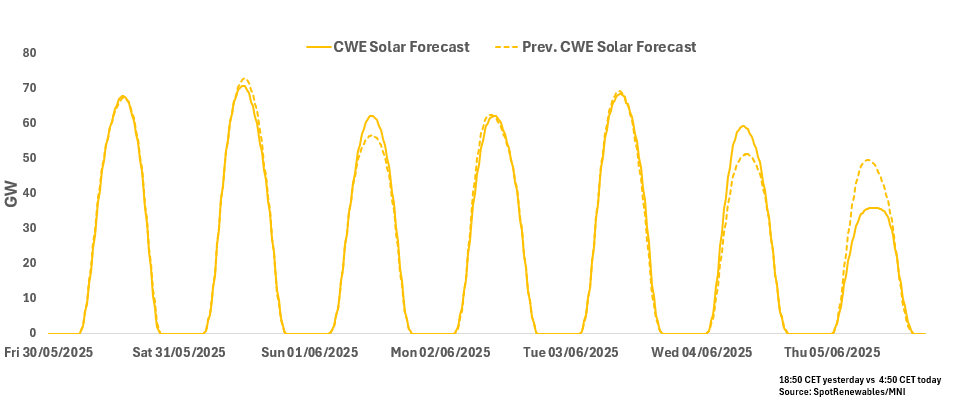

RENEWABLES: CWE Morning Solar Forecast

See the latest CWE Solar forecast for peak-load hours starting this morning for the next seven days. CWE peak solar is anticipated between 18-32% load factors, with the highest amount of PV on 31 May and the lowest on 5 June.

CWE Solar for 30 May – 5 June

- 30 May: 49.63GW

- 31 May: 51.34GW

- 1 June: 44.92GW

- 2 June: 45.92GW

- 3 June: 50.22GW

- 4 June: 42.85GW

5 June: 28.32GW

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BRENT TECHS: (N5) Resistance Remains Intact

- RES 4: $78.10 - High Jan 15

- RES 3: $75.81 - High Feb 20

- RES 2: $74.63 - High Apr 2 and a bull trigger

- RES 1: $68.67 - 50-day EMA

- PRICE: $64.10 @ 07:11 BST Apr 29

- SUP 1: $61.51/58.00 - Low Apr 10 / 9 and the bear trigger

- SUP 2: $56.29 - 2.236 proj of the Feb 20 - Mar 5 - Apr 2 price swing

- SUP 3: $55.10 - 2.382 proj of the Feb 20 - Mar 5 - Apr 2 price swing

- SUP 4: $54.00 - Round number support

Brent futures have pulled back from their recent highs. For now, the latest recovery is considered corrective and has allowed a recent oversold condition to unwind. The primary trend direction remains down and a resumption of the bear cycle would open $56.29 a Fibonacci projection. Initial support to watch lies at $61.51, the Apr 10 low. On the upside, the next important resistance to monitor is at the 50-day EMA, at $68.67.

BUNDS: Italian supply, US Earnings and Labour Data are in focus

- There's very little change for the German Bund, and also multi cross assets (Equities, FX), Bund and US Tnotes have seen some of their lowest traded Volumes for their Overnight sessions in quite some time, a busy Week ahead on the Data front, US earnings, and also Month end.

- The German GFK was better than expected, but not a known market mover, Bund is bid on Cash led flows, but all in very small.

- Small resistance moves down to 131.63, but the Main upside target is unchanged at 132.03, while support is unchanged at 130.75.

- Today sees, Spain prelim CPI/GDP. ECB Inflation Expectations, US Prelim Wholesales, and JOLTS.

- SUPPLY: Italy €3.5bn 2030 (equates to 19k BTP or 73k 2yr short BTS), Italy €4bn 2035 (equates to 38.7k BTP) that's heavy Italian supply, will weigh, UK 2054 Linker (won't impact Gilt).

- SYNDICATION: Finland, and France.

- SPEAKERS: ECB Cipollone, Villeroy, BoE Ramsden.

EUROPEAN INFLATION: Spain CPI/HICP Both Expected at 2.0% Y/Y [2/2]

Recap: Spanish March HICP inflation confirmed flash estimates at 2.22% Y/Y (vs 2.89% prior). As expected, energy (specifically electricity) inflation dragged on the headline reading, falling to 1.71% Y/Y (vs 8.58% prior).

- Excluding energy and unprocessed foods, HICP inflation was 2.00% Y/Y (vs 2.11% prior). Services inflation pulled back two tenths to 3.11% (vs 3.33% prior). Decelerations in medical, recreation/culture services and package holidays were somewhat offset by an uptick in transport services and accommodation.

- Non-energy industrial goods inflation remains subdued, but ticked up to 0.20% from 0.02% prior.

- The proportion of ECOICOP sub-components with annual inflation rates between 1-3% ticked up to 30% from 27% in February.

For reference, Spain represents 12% of the Eurozone-wide HICP basket in 2025.