COMMODITIES: Crude Rises Amid Mid-East Uncertainty, Gold Steady

Apr-16 18:50

* Oil prices have risen on Thursday, gaining further ground following a report that Gulf and EU of...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

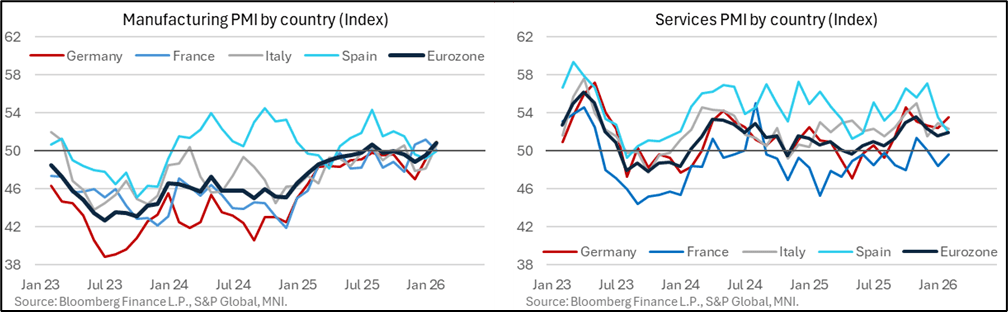

ECB: Macro Since Last ECB - Growth: ... But Manufacturing PMIs Hit 44-Month High

Mar-17 18:43

- As for softer indicators, the manufacturing PMI surprised higher in the preliminary February reading and then held onto this increase in the final update, whilst the services PMI saw a more modest increase.

- The manufacturing improvement to 50.8 (44-month high) is welcome after a recent stalling around the breakeven 50 level since mid-2025.

- The services PMI at 51.9 is only at a 2-month high as it consolidates a pullback off the recent high of 53.6 in November, a moderation driven by Spanish services activity cooling from some particularly elevated readings.

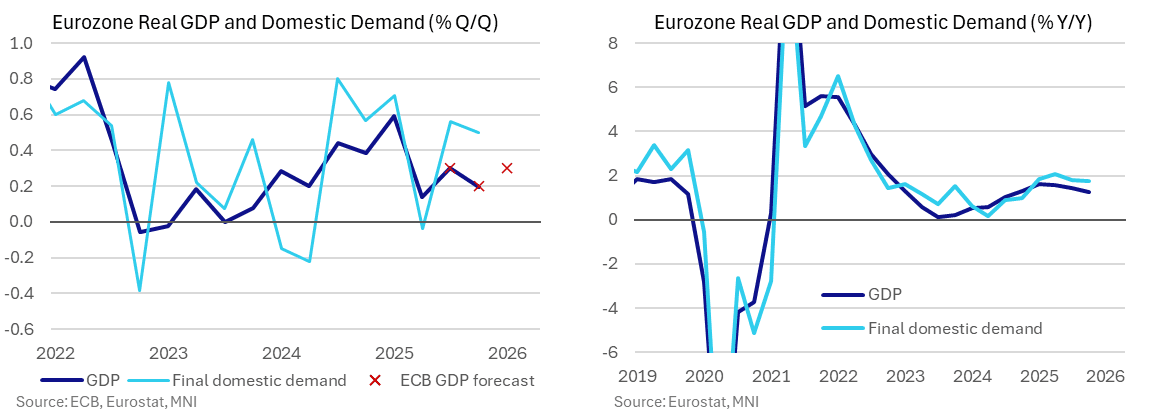

ECB: Macro Since Last ECB - Growth: Q4 GDP Revised Back Down To Forecast...

Mar-17 18:41

- Real GDP growth ended 2025 on a softer note than first thought, although the downward revision was driven by volatile Irish data. What was initially a stronger than expected 0.33% Q/Q non-annualised increase in the flash Q4 release ahead of the February meeting has since been revised down to 0.20% Q/Q in the third release.

- Still, that’s only back to in line with the 0.2% the ECB forecast for Q4 from the December projections, which then forecast then 0.3% in 1Q26 before three consecutive 0.4% quarters to end-2026.

- Within the Q4 details, final demand tells a stronger underlying story, with 0.5% Q/Q and 1.7% Y/Y vs 1.24% for GDP. Within that, consumption accelerated with 0.44% in Q4 after 0.25% in Q3 whilst gross fixed investment was still strong at 0.61% Q/Q (albeit disappointing consensus of 0.8%) after a particularly solid 1.25% in Q3 (revised up from 1.01%).

- There was an improvement in Eurozone labour intensity, with hours worked growth of 0.5% Q/Q outpacing employment growth of 0.2% Q/Q. Given GDP growth was 0.2%, this implied a negative sequential productivity per hour reading. The ongoing Middle East conflict is currently top of mind but progress is still needed in ensuring compensation and productivity developments are consistent with the 2% target in the medium term. This interplay is key for the services inflation outlook, which is largely dictated by domestic conditions.

BONDS: EGBs-GILTS CASH CLOSE: Rally Continues As Oil Stabilises

Mar-17 18:39

European yields pulled back for a 2nd consecutive session Tuesday.

- Intraday moves largely mirrored the trajectory of oil, with a sustainable rally taking hold after oil futures' overnight peak.

- Some desks attributed the stabilization in oil prices, and hence EGB / Gilt / equity rally, to reports that Iranian security chief Larijani had been killed, potentially auguring a nearer-term end to the conflict in the Middle East.

- The two-day rally means 10Y Gilt / Bund yields have now erased the rise seen in last week's Thursday-Friday sell-off (respectively now 13bp / 9bp down from the highs).

- In data, German ZEW saw the largest one-month fall since April 2025. Italy Feb HICP was revised down a tenth from the flash estimate.

- The German and UK curves bull flattened, with Gilts outperforming Bunds, while periphery/semi-core EGB spreads tightened for a second session.

- Wednesday brings final Eurozone February CPI data, while most attention will be on the US Federal Reserve decision.

- Focus for the week in Europe remains on Thursday's ECB (MNI preview here) and BOE decisions.

- Additionally, today MNI published a preview of Thursday's UK labour market release - here.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1bps at 2.392%, 5-Yr is down 2.3bps at 2.579%, 10-Yr is down 3.4bps at 2.918%, and 30-Yr is down 3.1bps at 3.486%.

- UK: The 2-Yr yield is down 4.7bps at 4.052%, 5-Yr is down 6bps at 4.234%, 10-Yr is down 6.3bps at 4.707%, and 30-Yr is down 5.7bps at 5.382%.

- Italian BTP spread down 0.9bps at 76.4bps / French OAT down 1.3bps at 65.7bps