OIL OPTIONS: Crude Put Skew Narrows from Most Bearish Since Sept.

The near term crude options call-put skew rebounds after yesterday turned the most bearish since late September. Global macroeconomic risks and hopes for Ukraine peace are weighed against supply risks from further sanctions on Iran.

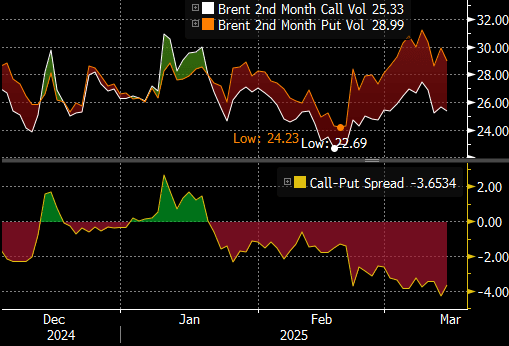

- The second month Brent call-put skew widened to nearly -4.3% yesterday although has regained some ground to around -3.6% today following a gain in front month futures.

- The WTI second month skew reached a low of -4.48% yesterday but is back to -3.4% today.

- The Dec25 call-put skews have also narrowed slightly today but holding rangebound through this week. Brent is around -4.15% and WTI at -4.75%. Monthly industry reports this week showed IEA revised its 2025 oil demand growth forecast lower, but OPEC maintained a more bullish view.

- Traded volumes for WTI and Brent put options are greater than calls volumes although WTI call aggregate open interest has increased this month.

- Brent MAY 25 up 0.8% at 70.41$/bbl

- WTI APR 25 up 0.8% at 67.11$/bbl

Source: Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SCANDIS: NOKSEK Tests Trendline Support As Oil/Gas Sell-off Weighs

NOKSEK has tested trendline support drawn from the August 5th low (0.9668 today). Clearance of this trendline would expose the December 20th low at 0.9625.

- NOK is underperforming the broader G10 basket with the exception of JPY, with crude oil and natural gas futures trading heavily. The FT reported overnight that the EC is weighing new powers to temporarily cap EU gas prices.

- EURNOK is up 0.7% on the session, narrowing the gap to the 20-day EMA at 11.6927.

- SEK is also weakening against the EUR and USD, which is allowing an oversold condition in EURSEK to unwind. Firm resistance is not seen until the 20-day EMA at 11.4005 though, with shallower rallies considered corrective.

- Riksbank Deputy Governor Bunge warned against placing too much weight on the higher-than-expected January CPI reading. She emphasised broader Riksbank guidance for a “tentative approach” to monetary policy going forward.

US TSY OPTIONS: TYH5 108.50 Puts Sold

TYH5 108.50 puts 4.7K given at 0-15, 11K trade all day, between 0-16 and 0-14.

EGBS: Supply Weighing Once Again

Bund futures are just off session lows, currently -19 ticks at 132.51 (lows of 132.48). The 20-day EMA at 132.63 has been pierced, with 132.34 the next downside target. Sovereign supply has once again weighed on EGBs, with a downtick in oil prices providing only temporary reprieve.

- German yields are 2-3bps higher, with the curve lightly bear flattening.

- The spread has been set for today’s 30-year OAT syndication, while conventional issuance has come from Greece, Germany and Portugal.

- Italian industrial production was much weaker than expected at -3.1% M/M (vs -0.2% cons, 0.3% prior), though it can be a volatile series month-to-month.

- 10-year EGB spreads to Bunds are up to 1.5bps tighter.

- Resident ECB hawk Holzmann unsurprisingly warned against 50bp cuts – but this probably already aligns with the median Governing Council view.

- Broader macro focus remains on the US CPI report at 1330GMT/1430CET.