COMMODITIES: Crude Falls Back, Gold, Copper Extend Gains

- WTI has lost ground today as it eases back from its highest level since July. Recent support comes from expectations of a tighter market.

- WTI Feb 25 is down by 2.1% at $78.4/bbl.

- The Russian sanctions may take some time to be fully in place, but buyers are already increasing interest in alternative non-sanctioned barrels.

- Middle East spot premiums for crude oil have risen to above a two-year high in some cases, as Chinese and Indian buyers seek alternatives to Russian flows.

- The recent strong impulsive rally in WTI futures has resulted in a breach of $76.41, the Oct 8 high, while $80.14, the Apr 12 ‘24 high has also been pierced, strengthening the bullish theme. Sights are on $81.69, a Fibonacci projection.

- Meanwhile, spot gold has risen by 0.7% to $2,716/oz today, bringing the yellow metal to its highest level since Dec 12.

- The recovery in gold opens $2,726.2, the Dec 12 high and an important resistance. Clearance of this level would be a bullish development, opening $2,730.4 next, the 76.4% retracement of the Oct 31 - Nov 14 bear leg.

- Copper has also extended its rally, with the red metal rising by another 1.0% today to $443/lb, taking total gains this month to 10%.

- Copper futures remain in a bull cycle. Recent gains have resulted in a move through key short-term resistance at $433.50, the Dec 12 high, opening $452.85, the Nov 5 ‘24 high and a key resistance.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

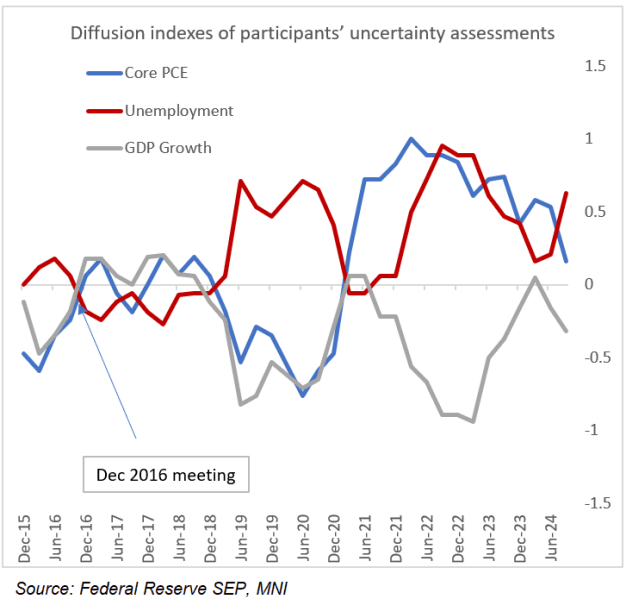

FED: Ex-FOMC Presidents Give MNI Varying Opinions On Trump Impact (3/3)

To be sure, opinions could vary. In interviews with MNI since the November meeting, three Dec 2016 participants had varied opinions on potential Trump policy impacts.

- Ex-St Louis Fed Pres Bullard told MNI: "If you think it’ll play out in a similar way this time [as 2016], inflation is the wrong narrative for this situation." Tariffs impact prices but also demand for those goods, and consumers switching to different products will dampen some of the inflation effects, he added. "Businesses faced with an uncertain situation over a two-year horizon might say, maybe I’ll postpone my investments. That’s the risk here more than an inflation risk."

- Ex-Richmond Fed Pres Lacker told MNI: “I would expect tariffs to provide an inflationary impulse."

- Ex-Dallas Fed Pres Kaplan told MNI: "This really is a puzzle. I'm going to avoid boring in too unduly on any one piece of the puzzle...tariffs are a piece of it, but they're just a piece of it, and so I've been reluctant to come to hard and fast conclusions yet, until I get a better sense of what that puzzle looks like."

FED: FOMC To Express Higher Uncertainty (2/3)

It's unclear how the current crop of FOMC members will interpret potential policy developments, but in the inter-meeting period, a few discussed shifts on trade/immigration under the incoming Trump administration, even if they stopped short of offering any conclusions.

- For example, St Louis Fed President Musalem – a hawk (who votes in 2025) - was asked at a public event if any of the scenarios on tariffs being produced by the St Louis Fed staff produced any "positive" outcomes for the economy. He replied that the “textbook” outcome is higher prices, potentially decrease demand and imports, and potentially increase domestic supply. He also said that we've seen the impact of the immigration surge over the past few years, and that "you can imagine if immigration policy were to change, you could imagine something going in the opposite direction".

- Richmond Fed President Barkin noted that whether tariffs cause inflation depends on the Fed's response. In other words, the Fed is responsible for maintaining price stability, and theoretically has control over the price level via settingmonetary policy.

- We interpret such comments as a sign that FOMC participants are concerned about the upside risks to inflation from government policy shifts.

- If nothing else, the FOMC will have to consider the shifts in markets since September’s 50bp cut, including a rise in long-term inflation breakevens (from close to 2% pre-cutting cycle, to over 2.3% now). A lot of that is the change in underlying economic conditions, but a good portion of it reflects anticipated policy changes (with pricing adjusting both in partial anticipation of, and following, the Republican election victory).

EURGBP TECHS: Resistance At The 50-Day EMA Remains Intact

- RES 4: 0.8448 High Oct 31 and reversal trigger

- RES 3: 0.8376 High Nov 19 and a bull trigger

- RES 2: 0.8356 High Nov 27

- RES 1: 0.8328 50-day EMA

- PRICE: 0.8263 @ 16:08 GMT Dec 17

- SUP 1: 0.8225 Low Dec 11

- SUP 2: 0.8203 Low Mar 7 2022 and a major support

- SUP 3: 0.8200 Round number support

- SUP 4: 0.8188 1.00 proj of the Oct 31 - Nov 11 - 19 price swing

EURGBP is holding on to the bulk of its most recent gains. Gains are considered corrective and attention is on 0.8328, the 50-day EMA. A clear break of this EMA would undermine the bear theme and signal scope for a stronger recovery. For bears, a reversal lower would refocus attention on 0.8225. Clearance of this level would expose the major support at 0.8203, the Mar 7 ‘22 low and the lowest point of a multi-year range.