EURGBP TECHS: Cracks Key Support

- RES 4: 0.8893 2.000 proj of the Sep 15 - 25 - Oct 8 price swing

- RES 3: 0.8875 High Apr 25

- RES 2: 0.8868 61.8% retracement of the 2022 - 2024 bear leg

- RES 1: 0.8818/65 High Nov 16 / 14

- PRICE: 0.8743 @ 16:40 GMT Dec 3

- SUP 1: 0.8755/46 50-day EMA / Low Nov 27

- SUP 2: 0.8726 Low Oct 28

- SUP 3: 0.8706 76.4% retracement of the Oct 8 - Nov 14 bull leg

- SUP 4: 0.8656 Low Oct 8 and a key support

The trend set-up in EURGBP is bullish and the current spell of weakness appears corrective - for now. MA studies are in a bull-mode position, highlighting a dominant uptrend. Price is trading below the 50-day EMA, currently at 0.8755 - a key S/T support. A close below this mark would signal scope for a deeper corrective pullback. Key resistance and the bull trigger is at 0.8865, the Nov 14 high.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURGBP TECHS: Bullish Trend Theme

- RES 4: 0.8865 1.764 proj of the Sep 15 - 25 - Oct 8 price swing

- RES 3: 0.8848 1.618 proj of the Sep 15 - 25 - Oct 8 price swing

- RES 2: 0.8835 High May 3 2023

- RES 1: 0.8818 High Oct 29

- PRICE: 0.8771 @ 16:26 GMT Nov 3

- SUP 1: 0.8751 High Sep 25

- SUP 2: 0.8729 20-day EMA

- SUP 3: 0.8699 50-day EMA

- SUP 4: 0.8656 Low Oct 8 and a key support

A bull cycle in EURGBP remains intact and last week’s strong gains strengthen current conditions. The break of resistance 0.8769, the Jul 28 high and a bull trigger, confirms a resumption of the uptrend and maintains the bullish price sequence of higher highs and higher lows. Sights are on 0.8835, the May 3 2023 high. Initial support lies at 0.8751, the Sep 25 high. Note that the trend is overbought, a pullback would be considered corrective.

BOC: Macklem: Policy Rates At Low End Of Neutral Range Providing Some Stimulus

BOC Gov Macklem is asked in an event Monday about why the Bank signaled last week that it wouldn't cut rates further (the actual Q from the host: "you said pretty clearly that this is it, you're done, unless things get way off course, you need to stop there. Why?") Macklem doesn't push back against the premise of the question, saying that there are limits to what monetary policy can do to mitigate the economic damage from the US-Canada trade conflict.

- Then asked why the BOC made in October what appeared to be explicit forward guidance on not cutting further, Macklem said: "We feel that with our interest rate at the low end of what we call our neutral range, it's providing some stimulus that's helping with this adjustment. But yeah, I mean, based on - and I would underline the conditionality of the statement - based on our current outlook with the current tariffs that are in place. Yes, we think monetary policy is in about the right place to provide some support while keeping inflation well controlled. We've also said, look, if the situation changes, you know, we're certainly prepared to adjust. We recognize there's still a lot of uncertainty."

- Implied BOC rates are little changed through the event, with a December cut just 12% priced and no full cuts seen through the rest of the cycle (about 1/2 a 25bp cut cumulative through next summer).

- On inflation, Macklem notes that upward momentum has "dissipated" but he's wary about how inflation may develop amid the ongoing "structural adjustment" in the economy: "Our assessment overall is still underlying inflation is about two and a half [percent].... that is a bit of a concern. And what you worry about is that headline inflation is going to adjust up to those rather than those adjusting down to 2%... the more reassuring sign earlier in the year, we did see some upward momentum in those. By which I mean, if you look at the three month, six month measures, they were running at 3.5%, they've now come down a little under 3. So some of that upward momentum we saw has come out. It takes a little while for that to show up in the year over year numbers. So we think that... upward momentum is dissipated. We think there's going to be some more easing. But look, this is a structural adjustment. We don't go through these very often. So yes there is a normal amount of uncertainty about how this is going to play out. And we're watching that closely. Our priority is to make sure that a tariff problem doesn't become an inflation problem."

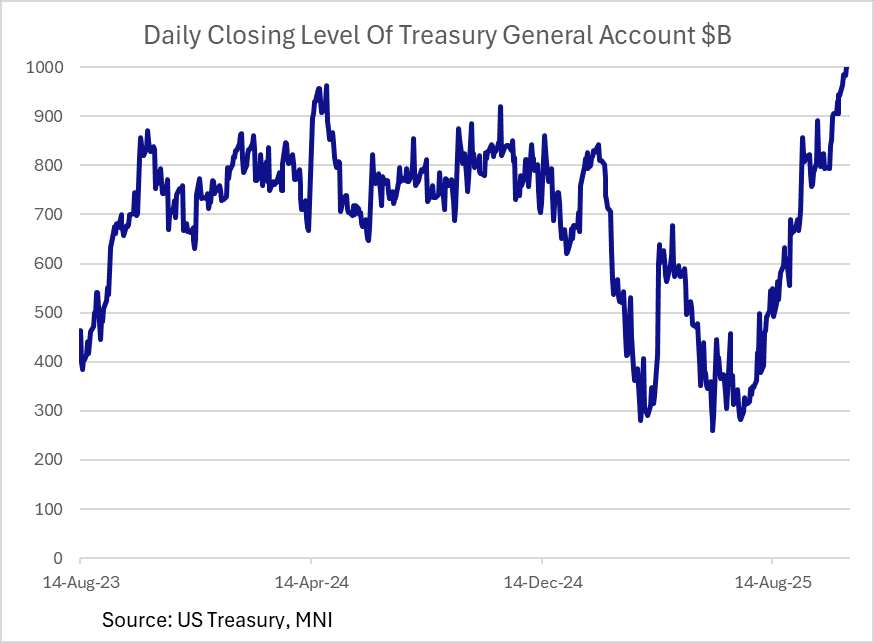

US TSYS/SUPPLY: Borrowing Requirements Hinge Partly On Treasury Cash Views (2/2)

We think we are slightly on the low side for Oct-Dec borrowing estimates vs consensus though expectations are extremely wide as usual and some of the outliers are predicated on increases in the TGA target.

- Our expectation of Treasury estimating $650B marketable borrowing requirements the Jan-Mar quarter is roughly at the median.

- Expectations for marketable borrowing:

- Oct-Dec: $525B (Jefferies), $570B (Deutsche), $600B (NatWest), $697B (Wells Fargo), $680B (Citi), $700B (Wrightson ICAP), $810B (TD)

- Jan-Mar: $387B (TD), $500B (Citi), $625B (Jefferies), $650B (Wrightson ICAP), $665B (Deutsche), $795B (Wells Fargo)

- TGA end-quarter targets: all $850B except: $900B (Jefferies and Wrightson ICAP), $950B (TD).