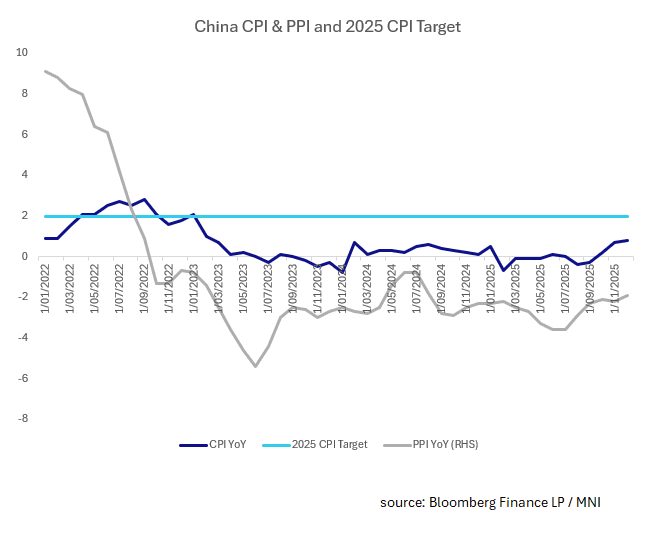

CHINA: CPI Highest Since Feb 2023

- December CPI in China rose 0.8% in line with estimates. China has not released the 2026 CPI forecasts yet but based on the 2025 forecast of 2.0%, CPI remains below target. The rise to 0.8% represents the highest CPI print since February 2023.

- Core CPI was steady at 1.2% where it has printed for the last 3-months.

- PPI was modestly better, a decline of -1.9% against estimates of -2.0% and prior month of -2.2%. For the PPI it is more of the same as a major structural driver the "involution" —intensive price wars among manufacturers continues. Excessive investment in sectors like electric vehicles, solar panels, and batteries has created a supply-demand imbalance, forcing companies to slash prices to clear inventory and maintain market share. Chinese authorities this week were meeting with battery manufacturers in a bid to further regulate and protect the industry whilst ultimately seeking to stabilize price declines.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

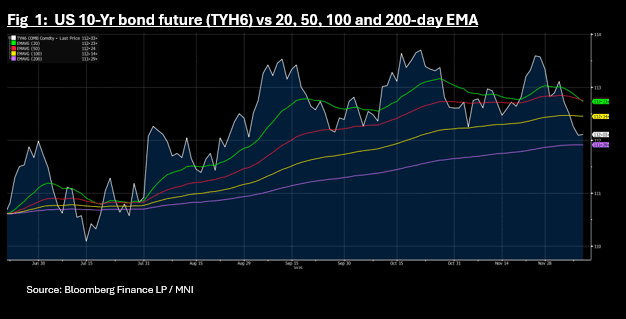

US TSYS: TYH6 Steadies Near Key Tech, Yields Grind Lower

Most US bond futures are flat to trending modestly higher during the morning session in Asia. The US 10-Yr is at 112-03+, just above the key resistance of the 200-day EMA at 111-29+.

Cash is better in the morning session with yields grinding lower. Across the curve yields are between 0.3 - 1.0bps lower as the 10-Yr backs away from its recent upper range of 4.20%

- The 2-Yr is at 3.611% : -0.8bps

- The 5-Yr is at 3.78% : -1bps

- The 10-Yr is at 4.182%: -0.8bps

- The 30-Yr is at 4.806%: -0.3bps

Tonight's auction will be a US$69 Bln 17-Week Bills

Ahead of the FED we look at the Macro since last FOMC. Real GDP growth has likely been the main area where the FOMC has been surprised to the upside, especially since the last economic forecasts with the September SEP but also since the late October decision. The Atlanta Fed’s GDPNow extended estimate eyes real GDP growth of 3.5% annualized in Q3, a useful tracker having now missed two official releases for Q3 originally scheduled for Oct 30 and Nov 26. Instead, the BEA is going to combine these two reports with an “initial” release that will include the alternate Gross Domestic Income series on Dec 23.

Assuming the Atlanta Fed estimate is accurate – and it has tended to outperform analysts in recent quarters – it paints a only a slightly softer picture than the 3.84% in Q2, with a similar story for private domestic final purchases estimated at ~2.6% annualized after 2.86% in Q2.

MNI: CHINA NOV CPI +0.7% Y/Y VS MEDIAN +0.7%; OCT +0.2%: NBS

- CHINA NOV CPI +0.7% Y/Y VS MEDIAN +0.7%; OCT +0.2%: NBS

- CHINA NOV CPI -0.1% M/M VS +0.2% M/M OCT

- CHINA NOV FOOD PRICES +0.2% Y/Y VS -2.9% Y/Y OCT

- CHINA NOV NON-FOOD PRICES +0.8% Y/Y VS +0.9% Y/Y OCT

- CHINA NOV PPI -2.2% Y/Y VS MEDIAN -2.0%; OCT -2.1%: NBS

- CHINA NOV PPI +0.1% M/M VS +0.1% M/M OCT

MNI EXCLUSIVE: China-German Trade

A German business leader in Beijing provides insight into China-German trade.

On MNI Policy MainWire now, for more details please contact sales@marketnews.com