EM LATAM CREDIT: Costa Rica: Fitch Affirmed ‘BB’ and Outlook

(COSTAR; Ba2/BB/BBpos)

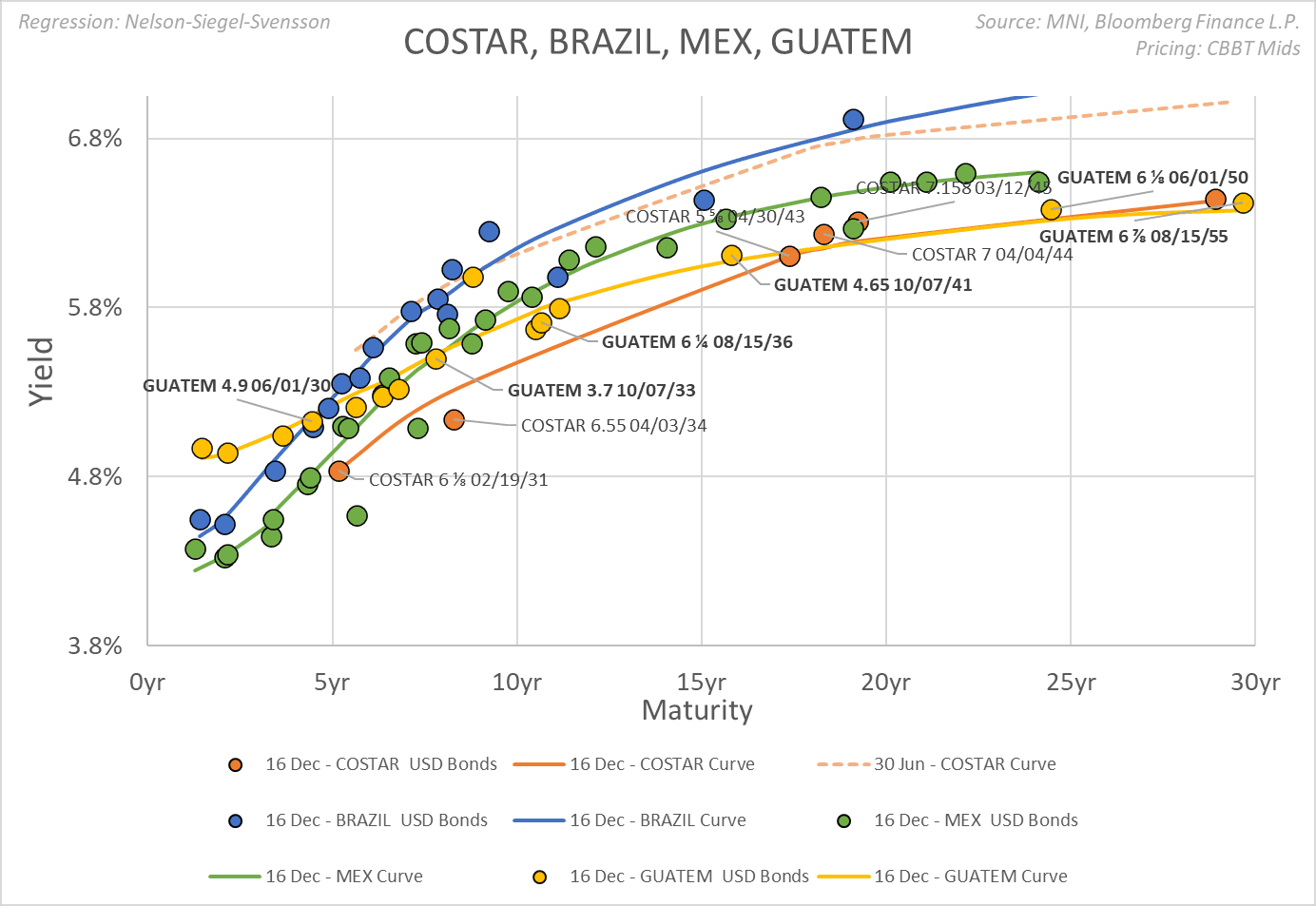

• Outlook positive assigned February 2025 and now affirmed again today. USD bond yields were already quoted about equal to higher rated Guatemala (GUATEM; Ba1/BB+/BB+), 70bp through similar rated Brazil (BRAZIL; Ba1/BB/BB) and flat yield to much higher, investment grade rated Mexico (MEX; Baa2neg/BBB/BBB-). We attribute some of Costa Rica’s low relative USD bond yields for the rating to technical factors as the country has not issued in USD for over two years and instead has chosen to fund itself in Euros and local currency denominated debt.

• Fitch affirmed the ‘BB’ rating, noting a solid fiscal policy structure and governance as well as an improved external position offset by high interest costs which kept the overall fiscal deficit elevated at 3.8% in 2024. The rating agency noted an impressive reserves accumulation of USD16bn as of November 2025, more than double the USD6.9bn in 2021 thanks to robust foreign domestic investment (FDI) and strong export performance that led to lower current account deficits.

• Higher ratings would be triggered by maintenance of a primary budget surplus and continued strong economic growth that would keep debt/GDP on its current stable to declining trajectory. Fitch cited a debt/GDP of 59.4% for 2025. The IMF shows a gross debt/GDP of 59.7% for 2025, down from a peak of 67.6% in 2021. All things being equal, we would look for a Fitch ratings upgrade sometime in the next three months as the time frame for outlooks is typically 12 months and the latest report suggests a justification for it.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: US TSY 26W BILL AUCTION: HIGH 3.710%(ALLOT 62.59%)

- US TSY 26W BILL AUCTION: HIGH 3.710%(ALLOT 62.59%)

- US TSY 26W BILL AUCTION: DEALERS TAKE 30.21% OF COMPETITIVES

- US TSY 26W BILL AUCTION: DIRECTS TAKE 9.06% OF COMPETITIVES

- US TSY 26W BILL AUCTION: INDIRECTS TAKE 60.73% OF COMPETITIVES

- US TSY 26W BILL AUCTION: BID/CVR 2.80

FED: US TSY 13W BILL AUCTION: HIGH 3.795%(ALLOT 56.39%)

- US TSY 13W BILL AUCTION: HIGH 3.795%(ALLOT 56.39%)

- US TSY 13W BILL AUCTION: DEALERS TAKE 38.44% OF COMPETITIVES

- US TSY 13W BILL AUCTION: DIRECTS TAKE 7.51% OF COMPETITIVES

- US TSY 13W BILL AUCTION: INDIRECTS TAKE 54.05% OF COMPETITIVES

- US TSY 13W BILL AUCTION: BID/CVR 2.79

US TSY OPTIONS: Large Dec'25 2Y Put

- 16,800 TUZ5 104 puts, 2.5 ref 104-03, open interest 40,986 coming into the session.

- Reminder - November options expire Friday