FRANCE DATA: Consumer Sentiment Weakens as Inflation Expectations Edge Up

Feb-24 07:50

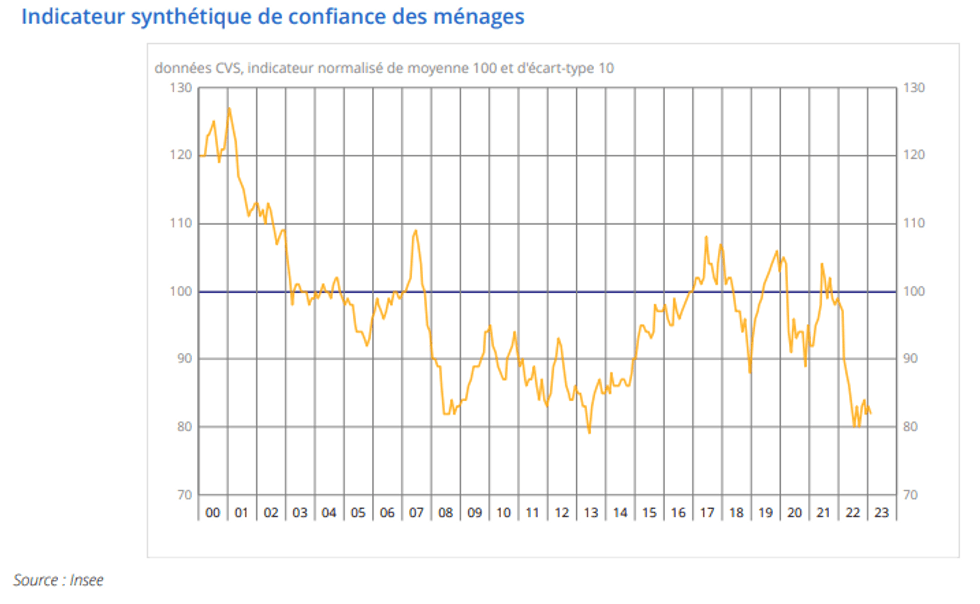

FRANCE FEB CONSUMER CONFIDENCE 82, JAN 83

- French consumer confidence edged down by one point to 82 in February, following the upwardly revised Jan data (due to a calculation error).

- The indicator remains only a few points above the September low and in deeply negative territory.

- Personal finance outlooks weakened and propensity to make major purchases was stable, dragging further on household consumption in the near-term.

- 12-month inflation expectations edged up in February. This follows the January HICP print, which edged up 0.3pp to +7.0% y/y, only 0.1pp below the October/November high.

- This uptick was largely due to the winding back of government energy support measures, which saw fuel and regulated gas prices jump recently.

- A continued decline in French inflation will be necessary if consumer sentiment is to improve over the coming months.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

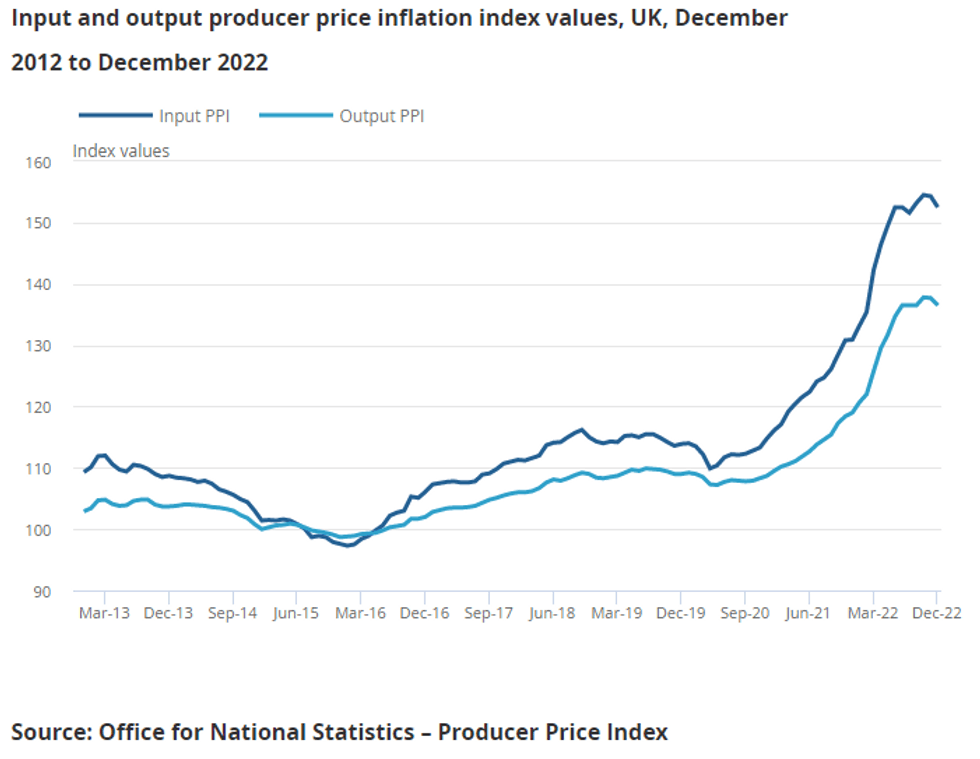

UK DATA: Initial Core PPI Easing Evident

Jan-25 07:46

UK PPI OUTPUT DEC -0.8% M/M (FCST +0.1%), +14.7% Y/Y; NOV +16.2% Y/Y

UK PPI INPUT DEC -1.1% M/M (FCST -0.8%); +16.5% Y/Y; NOV +18.0% Y/Y

- Annualised input PPI slowed for a fifth (sixth) consecutive month in December to +16.5% y/y (output +16.5% y/y), 8.1pp below the June record high. The UK December PPI data release also included revisions, whereby rates were largely upgraded by +0.1 to +0.2pp in H2 due to reweighting corrections.

- PPI contracted by -0.8% m/m (output) and -1.1% m/m (input), the largest m/m falls since April 2020 -- the first full month post lockdowns).

- Downwards pressure came largely from crude oil, and to a lesser extent from other parts/equipment and metals. Easing supply bottlenecks alongside weakening demand is supporting slowing factory-gate inflation.

- Despite core output PPI up by +0.1% m/m, core input PPI fell by -0.4% m/m. This was the first contraction in m/m input PPI since the lockdown of April 2020. The focus will be on whether this translates into falling output PPI, which should feed into easing core CPI which had proven to be very sticky between +6.3% to +6.5% y/y since August.

- Around 45bp remain priced in for next Thursday's BOE meet.

EURIBOR OPTIONS: Outright put buyer

Jan-25 07:35

ERG3 97.00p, bought for 2.25 in 7.1k (ref 97.04)

CROSS ASSET: Estoxx future edging higher

Jan-25 07:31

- Estoxx futures ticks higher, looking to close the small opening gap up to 4163.00.

- Further upside continuation, could keep the lid on the USD.VGH3 small resistance comes at 4176.00, but better is seen at 4206.00.

- The Dollar holds onto small gains against the NZD and the Yen, trades flat against the CHF and the Pound.

- Best performer is the Aussie, after the overnight inflation beat for the country, as market participants pencil a hike for the next rate meeting on the 7th February.