EU CONSUMER CYCLICALS: CONSUMER CYCLICALS: Consumer & Transport; Week in Review

Oct-25 16:02

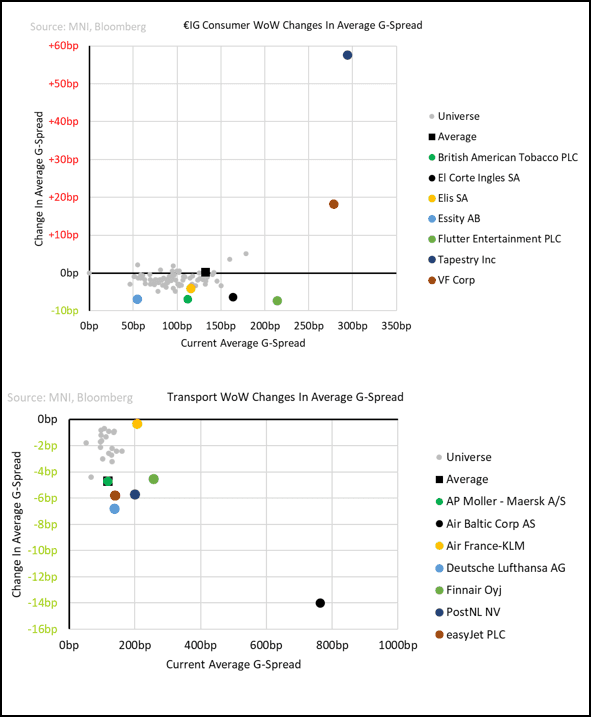

McDonald’s causing a E. Coli outbreak, Kering with an outsized earnings miss and a US Judge surprising markets with a ruling against Tapestry has given us an eventful week. It won’t slow down next week with VF earnings on Monday and local Airlines kicking off. DSV’s 5-part supply will come alongside all that. (links in the weekly pdf)

Fundamentals linked news

- Kering gives FY EBIT guidance that implies an over halving in year-on-year 2H profits. We expect S&P downgrade. The co struggling to turn around larger Gucci in this macro environment and it does not bode well for Burberry.

- Edenred numbers were firm but upcoming Italian regulation looks to be having an outsized earnings impact has frightened markets to read-through on other regions. Bonds are coming out of tights, but Pluxee levels remain interesting ahead of its earnings

- Electrolux continues to give weak numbers ex. LATAM. We expect a S&P downgrade

- Carrefour YTD trends continued in the sales update. The read through to Auchan is negative on a still competitive French hypermarket pricing environment

- Phillip Morris reports firm earnings continuing its streak. Investments it made - while peers prioritised equity payouts - is benefiting it now

Event Driven Movers

- Tapestry; Judge rules in favour of FTC catching the market by surprise - pricing was moving towards 60% in equities and 70% in local bonds. A 101 forced call is the likely outcome now across the ~$6.1b in bonds

- McDonald’s causes a E-Coli outbreak across several US states. 49 cases, 10 hospitalisations and 1 tragic death are still contained vs. Chipotle issues and leaves it more in-line with past outbreaks that had smaller impact to companies. Earnings next week is likely to paint a bleak picture on trading conditions this week

- VF Corp equities face a broker cut. It seems to echo what we are seeing in US card data - a lack of a turnaround. Bonds are repeating last quarter moves, selling off aggressively into the print

- Auchan; French paper carries headlines it has found a domestic seller of the Russian business. S&P sees it at ~10% of earnings but unclear in the restricted market what multiple it will get. Bonds rallied on the news

- Air Portugal; Air France the latest of companies rumoured to be lining up for a stake. The mover for credit will be if the government offloads a majority stake – and if so to who. Earnings ahead.

- Alimentation Couche-Tard comments late last week turned less conservative on the debt/equity funding mix – yet it continues to commit to “high” IG rating. The target (7-11) remains defensive attempting to appease investors in its ‘IR Day’ this week.

- JDE Peets stock bounces as it names a new CEO and reaffirms FY guidance. It is the local F&B reject in credit – somewhat unfounded vs. fundamentals.

- IDS does a bolt-on taking a 20% stake in Greece’s largest parcel carrier. We revisit levels ahead of earnings

Primary (fundamentals linked, levels below)

- Priced; Nestle (6 & 12yr), Fressnapf (7NC3), Picard (4.7NC0.7 floater tap)

- Mandates: DSV (2,4,6,8,10yr; M&A supply), Boparan (£5NC2), Takko Fashion (5.5NC2)

Rating Actions

- Victoria (Secured; B3 Neg/B Neg/BB); Moody’s downgrades to B3 and stays on negative outlook after rough earnings

- Adidas (A3 Neg/ A- Stable); An overdue stabilisation in ratings from S&P

- Agrifarma (B1/B CW Pos): S&P moves to CW positive. It expects it to remain a separate subsidiary to Fressnapf but is accessing level of support latter may provide in the absence of cross-default and guarantees.

- Picard (B2/B neg/BB-); S&P moves to neg outlook as the co does a €200m tap of the floater to buyout current majority owner (Lion Capital). It sees the change of owner as positive to BS governance.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: Greenback Hits Highs Through London Close

Sep-25 15:57

Greenback edges to new daily highs alongside the London close, helping GBP/USD fade through earlier lows and open an 80 pip gap with the overnight highs.

- No specific headline or news trigger behind the greenback move, but persistent gains for US yields and the steepening of the curve are helping the case - Treasuries have extended losses following the modestly higher than expected New Home Sales data, with Treasury supply still to come later today ($28B 2Y FRN Note, $62B 17W bills and $70B 5Y notes).

- Influx of potentially large corporate issuance from Oracle and Saudi Aramco also being absorbed, with the ripple effects leading through to dollar strength in recent trade.

US TSYS: US TSY 1Y-10M FRN AUCTION: HIGH MARGIN 0.261%; ALLOTMENT 16.37%

Sep-25 15:32

- US TSY 1Y-10M FRN AUCTION: HIGH MARGIN 0.261%; ALLOTMENT 16.37%

- US TSY 1Y-10M FRN AUCTION: DEALERS TAKE 42.57% OF COMPETITIVES

- US TSY 1Y-10M FRN AUCTION: DIRECTS TAKE 0.89% OF COMPETITIVES

- US TSY 1Y-10M FRN AUCTION: INDIRECTS TAKE 56.54% OF COMPETITIVES

- US TSY 1Y-10M FRN AUCTION: BID/CVR 2.86

US TSYS: US TSY 17W BILL AUCTION: HIGH 4.430%(ALLOT 38.21%)

Sep-25 15:32

- US TSY 17W BILL AUCTION: HIGH 4.430%(ALLOT 38.21%)

- US TSY 17W BILL AUCTION: DEALERS TAKE 36.12% OF COMPETITIVES

- US TSY 17W BILL AUCTION: DIRECTS TAKE 5.03% OF COMPETITIVES

- US TSY 17W BILL AUCTION: INDIRECTS TAKE 58.85% OF COMPETITIVES

- US TSY 17W BILL AUCTION: BID/CVR 2.80