EU: Commission Outlines Multi-Trillion Euro Defence Readiness Roadmap

At a presser following a meeting of the College of Commissioners, European High Representative for Foreign Affairs and Security Policy Kaja Kallas speaks on the EU's 'Defence Readiness Roadmap'. Says that "Over the next few years, there must be a major build-up of European defence capabilities," warning that "Russia has no capacity to launch an attack on the EU today, but it could prepare itself in the years to come." Kallas: "The danger will not disappear even when the war in Ukraine ends. It is clear that we need to toughen our defences against Russia." Says the goal is to have a drone defence system for the EU ready by 2028.

- Speaking alongside Kallas, European Defence Commissioner Andrius Kubilius says the roadmap implies investment of EUR6.8 trillion in defence by 2035.

- Bloomberg News reported on 15 Oct on a draft roadmap it had seen that was presented to the College today, and will go before EU leaders at next week's European Council summit.

- The article claims the roadmap demands, "EU countries must coordinate their defense spending, it argues, and swiftly create coalitions to jointly erect new defense programs."

- The coordination of defence spending across national borders, combined with aims of a multi-trillion euro outlay, is likely to either see such an ambitious project fail to get off the ground, or it ends up significantly diluted amid national fiscal constraints.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

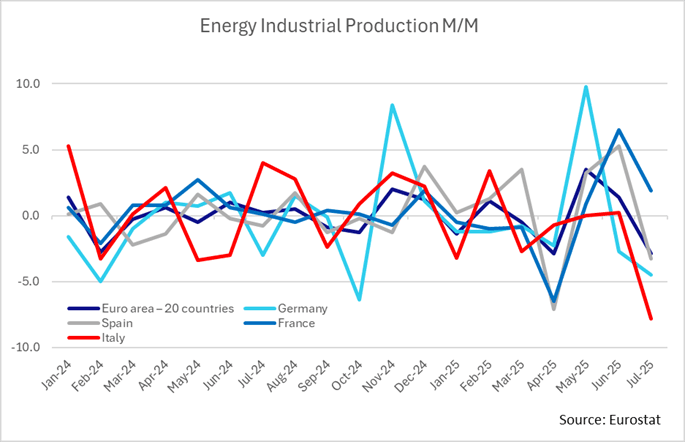

EUROZONE DATA: July IP Broadly In Line, Energy Volatility Mutes Strength

Euro area industrial production increased in July despite a return of a heavy drag from energy, with M/M readings on balance surprising positively but the Y/Y as expected. IP growth of 1.8% Y/Y is within some wide recent ranges owing in part to energy volatility.

- Euro area IP modestly undershot expectations in July with 0.3% M/M (cons 0.4) but that was easily more than offset by a large upward revision to -0.6% M/M in June (initially -1.3%).

- That was a ‘genuine’ upward revision with the Y/Y also lifted from 0.2% to 0.7%. Interestingly though, despite this upward revision the Y/Y in July was as expected at 1.8% (although note 27 replies for the M/M vs 12 for Y/Y in the Bloomberg survey).

- This 1.8% Y/Y is the only the highest since March, with the series oscillating between rates a little above 0% and below 4% in recent months.

- Broadly speaking, Germany and Italy’s growth (+1.5% and +0.4% M/M respectively) were partly offset by declines in France and Spain (-1.2% and -0.7% M/M respectively).

- Ireland’s usual volatility, which had driven previous M/M moves, calmed this month (+0.6% M/M vs -11.9% prior).

- Swings in energy IP have also had an increasingly large contribution to the headline number in recent months, with euro area energy IP contracting -2.9% M/M (vs +1.4% June). One ex-energy measure increased 0.8% M/M in July after -1.0% in June.

- Highlighting this volatility, Italy’s energy IP fell -7.8% M/M (vs +0.2% prior), Germany’s -4.5% M/M (vs -3.3% prior), and Spain’s -3.3% M/M (vs +5.3% prior). France saw an increase of +1.9% M/M (vs +6.5% prior).

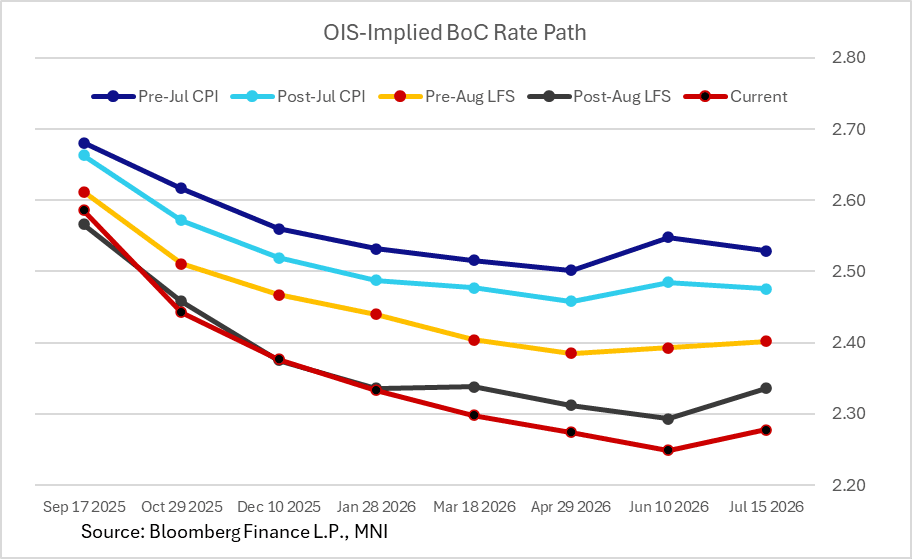

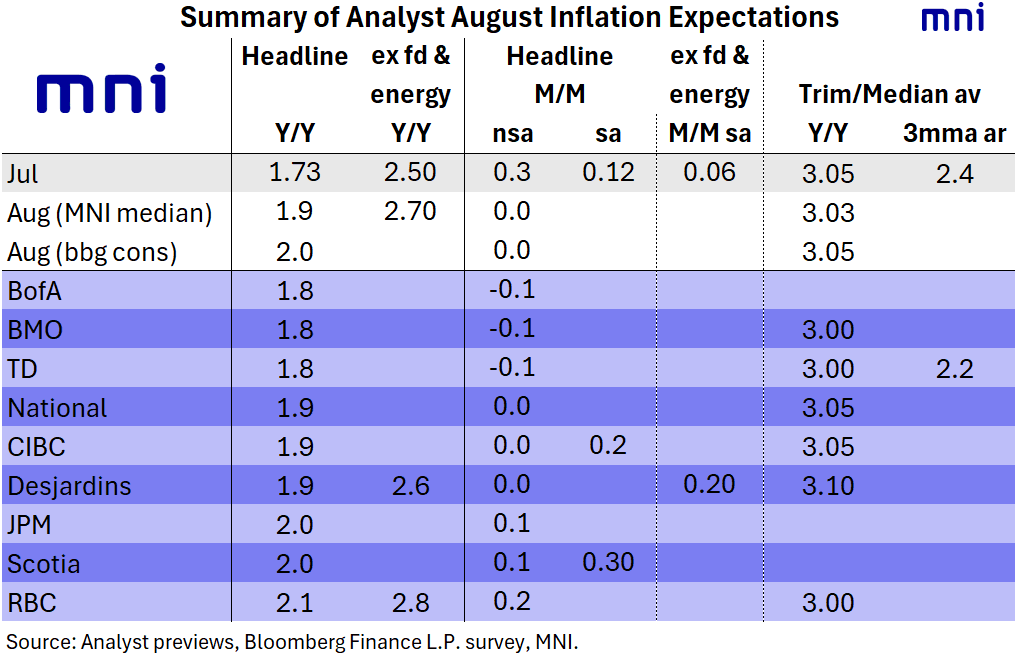

CANADA: High Bar For CPI To Dissuade BOC From Cutting Tomorrow

Today's (0830ET) inflation report is expected to show a slight pickup in headline CPI in August vs July when measured on a Y/Y basis, but flat on a sequential non-seasonally-adjusted basis. More importantly the Bank of Canada's preferred measures of core inflation are seen remaining steady, with risks perceived to be slightly to the downside.

- MNI's compilation of analyst forecasts shows a median headline expectation of 1.9% Y/Y headline CPI (1.73% prior), with NSA M/M of 0.0% (0.3% prior) and the average trim/median Y/Y at 3.03% (implying some downside risks to the average remaining steady at 3.05%).

- The range of headline estimates is 1.8%, to 2.1%, with the pickup on a Y/Y basis due to base effects and not sequential pressures which are seen to be limited.

- While headline CPI is seen picking up, it would mark the 5th consecutive month below 2.0%.

- As such it's unlikely that anything but a huge surprise will dissuade the Bank of Canada from cutting rates by 25bp Wednesday. The pickup in core measures this summer had been seen as a potential obstacle to further cuts - so a continuation of July's softer momentum could help shape the message that the BOC retains its easing bias.

- Analysts aren't convinced that the report will have much bearing on the Wednesday decision, due in large part to the fact that the rate deliberations will have all but concluded by now, though a few meeting previews noted that there may be an impact if there is a significant upside surprise.

- Coming into the data, 6 of 7 Canadian institutions see a 25bp cut (RBC the exception, seeing a hold.)

- Current BOC meeting-dated OIS cumulative cuts implied: Sep 22bp (almost 90% prob of a cut), Oct 36bp, Dec 43bp, Jan 47bp, Mar 51bp.

OUTLOOK: Price Signal Summary - Bunds Remain Above Support

- In the FI space, Bund futures have pulled back from their latest highs. Recent gains have resulted in a break of resistance at 128.87, the Aug 28 high and a short-term bull trigger. The climb undermines a recent bearish theme and highlights a stronger reversal. Scope is seen for an extension towards 129.50, the Aug 5 high. Key support and the bear trigger has been defined at 127.61, the Sep 3 low. The latest pullback is - for now - considered corrective. First support lies at 128.25, the Sep 4 low.

- A bull cycle in Gilt futures remains in play - a recent rally highlights a stronger corrective cycle and the contract is holding on to its gains. Note that the move higher is allowing an oversold trend condition to unwind. Price has breached initial firm resistance at 90.84, the Aug 28 and 29 high. A continuation higher would signal scope for a climb towards 92.06, the Aug 14 high. On the downside, initial support lies at 90.65, the Sep 5 low.