ASIA: Coming Up in Asia Today

--------------------------------------------------------------------- 0100BST 0900HKT 1100AEST ...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: Cheaper With US Tsys Amid Mideast De-Escalation Questions

NZGBs are 2bps cheaper after US tsys finished showing a bear-steepener, with yields 5-8bps higher amid uncertainty on Mideast de-escalation.

- After a constructive start following through from Monday's comments by President Trump that the Iran conflict could soon be over, cash yields leaned higher throughout the day.

- Early afternoon reports of oil tankers moving through the Strait of Hormuz (including one by the US Energy Secretary on X.com saying the US Navy had escorted one such tanker) helped oil take another leg lower. However, these reports were quickly refuted (Energy Sec Wright deleted his post), with a CBS report on Iran potentially mining the Strait then seeing oil rebound sharply.

- There was also some pressure at the short-end after the 3Y Note auction was one of the weakest in the last year, tailing 1.1bp (after having traded-through for the 6 consecutive auctions prior).

- Swap rates are 1-2bps higher.

- RBNZ-dated OIS pricing is little changed across meetings. No tightening is priced for April, while December 2026 assigns 44bps.

- The local calendar will be empty until Thursday's release of Q4 Mfg Activity data.

- On Thursday, the NZ Treasury plans to sell NZ$250mn of the 1.50% May-31 bond, NZ$150mn of the 4.25% May-34 bond and NZ$50mn of the 1.75% May-41 bond.

Bloomberg Finance LP

CNH: Scope For Continued Outperformance Amidst Strong Exports/Trump Visit

USD/CNH extended its pullback post Tuesday's Asia close, before finding support around 6.8600 in US trade. We track near 6.8790 in early Wednesday dealings, after posting a 0.12% gain for Tuesday's session. We are back under the 20-day EMA, but firmer resistance has been evident around the 50-day EMA (6.9310). On the downside, outside of Tuesday lows, late Feb lows were at 6.8267. The DXY and BBDXY indices lost ground in Tuesday trade, but recovered from lows in US trade as oil rebounded amid conflicting Strait of Hormuz reports. This filtered through to USD/CNH which is still following broader USD trends.

- Spot USD/CNY ended at 6.8685 on Tuesday, while the CNY CFETS basket tracker was at 99.46, off recent highs of 99.90, in line with lower risk aversion and softer USD index levels. Still, crosses like CNH/JPY remain in firm uptrends, with the pair close to an upside test of 23.00 (last 22.976).

- Yesterday's strong export data/healthy trade balance, should reinforce a firmer yuan backdrop, particularly ahead of US President Trump's planned visit to China in a few weeks.

- CNH seasonality is typically weaker in March and April, but such trends may not appear, at least until post Trump's visit (he is due to arrive on March 31).

- On the data front, we await Feb new loans/aggregate finance figures (due between now and Mar 14).

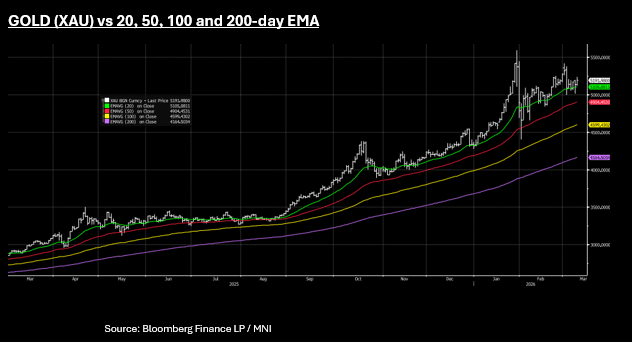

GOLD: Gold to Look Through FEB CPI Towards Medium Term Inflation

- A moderating USD Tuesday gave gold a boost posting 1% gains and nearing $5,200 again.

- Finishing at USD$5,191 gold had tested $5,200 - reaching $5,238 briefly before moderating back as the USD regained some of its earlier lost ground, whilst continuing to track the 20-day EMA.

- The 14-day Relative Strength Index remains broadly neutral though the MACD still shows a bearish cross - suggesting that a short term downward trend still exists.

- The release of February's U.S. CPI data on March 11. Economists expect inflation to remain relatively steady compared to January's cooler-than-anticipated figures with headline CPI YoY forecast at +2.4% (prior +2.4%); CPI MoM expected to rise 0.3% (+0.2% prior) and Core CPI YoY forecast to hold steady at +2.5%.

- With the rise in oil prices in recent weeks, inflation expectations have repriced bond markets with the June FED meeting now only pricing in 29% probability of a cut and July 27%. July at its peak had a 71% probability of a cut.

- Whilst a very weak CPI print may bring forward rate cut expectations (and boost gold), in the current environment the February CPI is likely to be viewed as stale given expectations for sharp rise in inflation going forward on the back of oil's ascent.

- Look for gold to tread water in the near term, dictated by USD moves. Medium term however will depend on whether we face a stagflation environment, which is typically good for gold.