CHINA: CNH Move Sticks, Fix Behaviour in Focus

Jan-22 12:57

CNH weakness is sticking at the NY crossover, with pre-Lunar New Year fix behaviour now coming into focus.

- We note that directionally the reaction to today's headlines makes sense: 'PBOC to prevent CNY overshooting', 'to use RRR cuts and interest rate cut tools'. While these are not new sentiments (both have been said explicitly already this year), it seems to have been sufficient to keep USDCNH bid.

- As such, fix behaviour should become a greater focus: China's Lunar New Year is not set to start until February 17th, but the PBoC and authorities commonly manage liquidity and market rates well ahead of the extended break - with CNY fix management a key tool to manage conditions into the long market holiday.

- Today's fix again came in higher than expected (7.0019 vs. Exp. 6.9681), extending the streak of the fixing coming in above forecast (averaging a ~350 pip spread this year) in a further sign that authorities are looking to slow the downward trend in USDCNY. This may be providing assymmetric risks to USDCNY spot ahead, allowing corrective rallies to run further.

- Similarly, we noted late last year that the specific intervention tools used by state-run banks were further evidence of concern for USDCNY's trajectory after several instances of state-owned banks buying USD, but not recycling the purchased USD via swaps - the net result being tighter local dollar liquidity - and more acute negative carry for USD/CNY shorts. This is particularly notable for exporters - as it disincentivises the sector from accumulating CNY as a hedge to lock in margins.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA: Tools Available to Slow USDCNY Decline; But L-T Trend Still Looks Down

Dec-23 12:48

- USDCNH and USDCNY both today his their lowest levels since September 2024 and are raising the risk of a test of levels below 7.00 as the USD depreciates more broadly and as onshore Chinese equities look to lock-in returns of 20% for 2025.

- The rally in CNH and CNY bolsters and may embolden the Chinese authorities calls for proactive monetary policy in 2026 (as evidenced in a report in today's Shanghai Securities News arguing in favour of easier interest rates and reserve requirement ratios in Q1), but other more direct tools remain available to smooth untoward CNY strength.

- In early December, there was strong evidence of intervention through buying USD - but with a new approach. Instead of recycling the bought USD in the FX swaps market, the state-backed lenders conducting the intervention held the USD for a longer period, thereby tightening onshore USD liquidity and pressuring markets to a more acute negative carry for USD/CNY shorts.

- This method not only helps support the spot price, but it also squeezes speculation and provides a strong disincentive for exporters to accumulate CNY as a hedge to lock in profit margins. This method, if used in sufficient size, should help slow any undesired USDCNY losses through the end of the month and headed into the particularly sensitive Lunar New Year period in mid-February.

- While these tools can slow any pace of appreciation in the short-term - the recognition of the need for natural currency strength (largely to address strong external balances) is clear, hence the recent CEWC statement that argued for "stable" exchange rates, rather than calling out currency strength in particular. This makes USDCNY losses beyond 7.00 far more likely longer-term, even as the depth of the Fed easing cycle continues to be unwound.

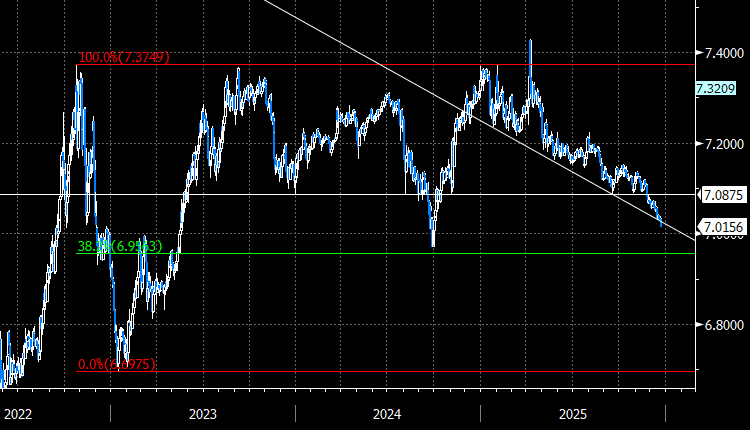

Figure 1: USDCNH through key support; downtrend accelerates

Source: MNI / Bloomberg Finance L.P.

OUTLOOK: Price Signal Summary - Bounce in Bunds Appears Corrective

Dec-23 12:18

- In the FI space, Bund futures remain in a clear downtrend and Monday’s fresh cycle low reinforces this condition. The move lower confirms a resumption of the downtrend Short-term gains for now appear corrective. Initial firm resistance is seen at 127.91, the 20-day EMA. A break of this average would signal the start of a stronger correction. For bears, a resumption of the downtrend would open 126.53, the Mar 11 low (cont.).

- Recent price action in Gilt futures highlights 90.50, the Dec 16 low, and 91.93, the Nov 27 high, as two important short-term directional triggers. A clear breach of support at 90.50 would signal scope for a deeper retracement towards 89.86, the Nov 19 low and a bear trigger. For bulls, a stronger resumption of gains and a breach of 91.93, would instead signal scope for a climb towards resistance at 92.55, the Nov 11 high.

SPAIN: Bank Of Spain Updates Inflation, GDP Projections

Dec-23 12:18

- Bank of Spain has published its quarterly report on the Spanish economy including updated macro projections here.

- The CPI view of 2.7% in 2025, 2.1% in 2026 and 1.9% in 2027 represent revisions of +0.2pp, +0.4pp, and -0.5pp, respectively. 2025/26 Revisions come "due to the incorporation into the central scenario of recent inflationary dynamics (higher than expected in September), the evolution of collective bargaining and the new macroeconomic scenario", while the lower view on 2027 comes on the back of the EU ETS2 delay.

- GDP is meanwhile seen at 2.9% in 2025, 2.2% in 2026 and 1.9% in 2027, upward revisions of 0.3pp, 0.4pp and 0.2pp, respectively. Despite the upward revisions, this means BoS sees the Spanish economy to narrow down on its current firm positive output gap.

- On risks: "Taking into account the different approaches used to assess the uncertainty surrounding the central scenario, the risks to activity appear to be balanced in the short term and slightly on the downside in the medium term, while the risks to inflation are tilted to the upside over the entire projection horizon. In particular, the uncertainty surrounding the evolution of wages and corporate margins could materialise in an alternative scenario characterised by higher inflation and lower GDP growth"