CZECHIA: CNB Holds Financial Stability Meeting, Pavel Refuses To Appoint Turek

- The Czech National Bank (CNB) holds a 'major' financial stability meeting today. The decision on the countercyclical buffer (CCyB) rate and a wider range of macroprudential parameters will be announced at 14:30GMT/15:30CET, during a press conference with Bank Board's Jakub Seidler and Financial Stability and Resolution Department's Libor Holub. The decision will be informed by the Financial Stability Report - Autumn 2025. The minutes of the meeting will be published two weeks later, alongside the full Financial Stability Report.

- President Petr Pavel will start interviewing ministerial candidates tomorrow, but already refused to appoint Filip Turek, honorary chairman of the Motorists party, to any cabinet position. Pavel remained defiant even as the ANO-SPD-Motorists coalition agreed not to propose Turek for the position of Foreign Minister and offer him the environment portfolio instead. ANO leader Andrej Babiš said that he respects the President's decision and will take it back to the Motorists for further consultations.

- The lower house returned the 2026 budget draft to the government after the ANO-led coalition signalled that the fiscal plan lacks around CZK96bn in necessary spending. The outgoing government has 20 days to propose amendments.

- The Chamber of Deputies holds an extraordinary session requested by the opposition to discuss ANO leader Andrej Babiš's conflict of interest amid his bid to become the next Prime Minister.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CROSS ASSET: Soft Bank Stocks Helping Support EGBs and Gilts in Early Trade

- Early risk-off trade is helping feed through to a bid in core EGBs, as Bunds, Gilts and US Treasuries all edge to new respective daily highs. Some of the risk-off stemming from early pressure in the banking sector, with BNP Paribas dropping another 3% after disclosing their exposure to a "specific" credit issue as part of their earnings release.

- BNP Paribas are one of the most highly weighted firms in the EuroStoxx Banking Index, which shifts focus to yesterday's opening gap in the price down at 225.28.

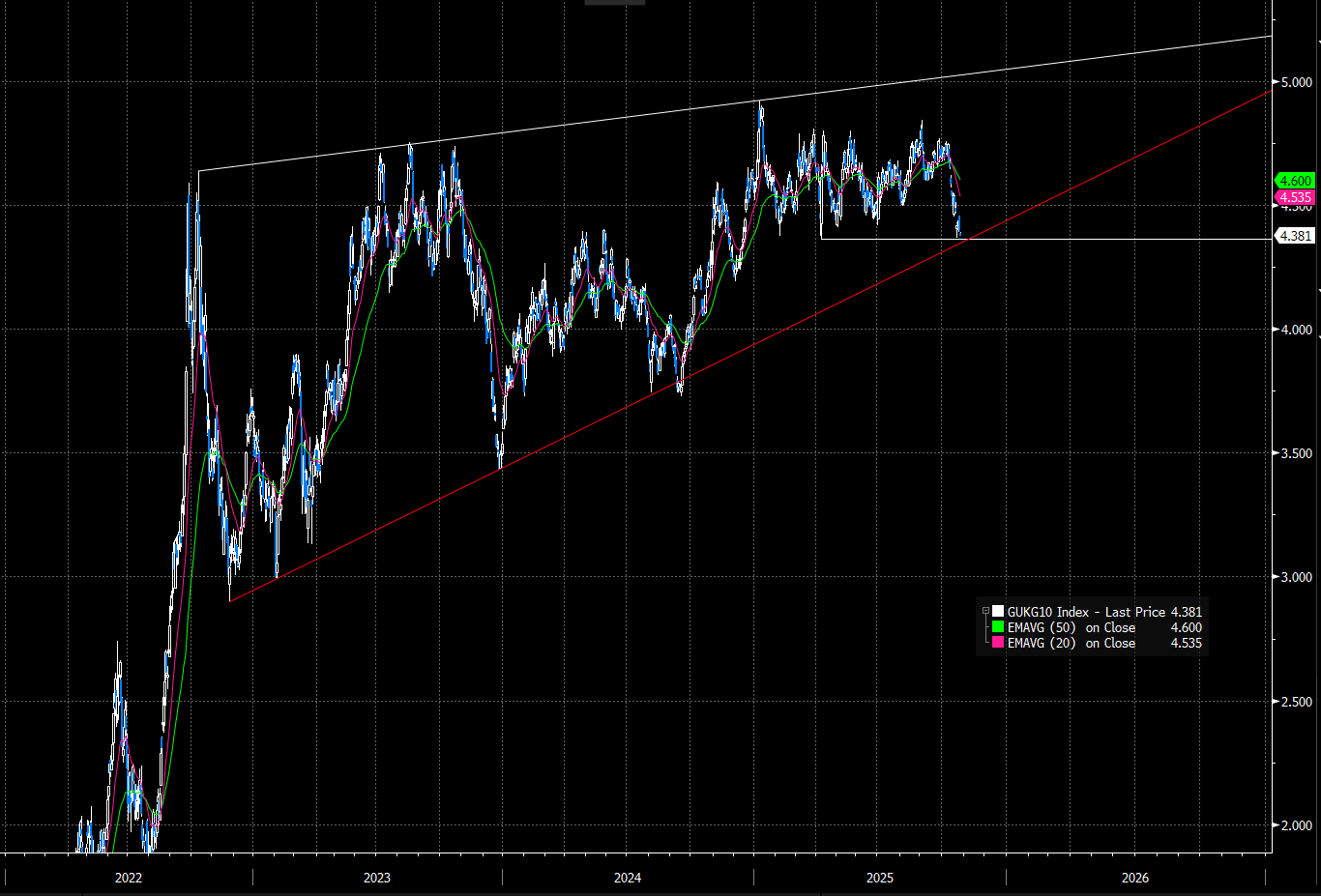

GILTS: Outperforming Bunds Across The Curve With More Fiscal Tightening Likely

Gilts outperform German peers across the curve, with the 10-year Gilt/Bund spread testing the March closing low of 177.5bps, down 1bp on the session. There are increasing signs that UK Chancellor Reeves will have to raise income tax at the November 26 budget to fill a widening fiscal hole, and potentially increase headroom above the ~GBP10bln seen at previous fiscal events.

- The FT reported yesterday evening that the OBR is expected to cut its trend productivity forecast by 0.3pp, larger than the 0.1-0.2pp that had been expected by most analysts/independent forecasters. The IFS’ Green Budget estimated that each 0.1pp downgrade to productivity would increase 2029-2030 PSNB by GBP7bln, so this downgrade implies a GBP21bln hit to public finances. A reminder that the YTD tracking error with existing OBR projections is also GBP7.23bln.

- 10-year Gilt yields are down 2bps to 4.38%, narrowing the gap to clustered support around 4.35% (April 7 low and trendline drawn from the November 2022 low). 30-year yields are down 1.5bps at typing, while 2- and 5-year yields have fallen almost 3bps.

- Gilt futures are +24 ticks at 93.89, just off opening highs of 93.91. A bull cycle remains intact, with moving average studies also highlighting a dominant uptrend. Initial resistance is the Oct 22 high at 93.93.

- The DMO will sell GBP1.5bln of the 1.125% Sep-35 linker at 1000GMT today.

- The BRC-NIQ Shop Price Monitor, released overnight, showed the first slowdown in the Y/Y pace of growth of the year, with overall shop price inflation falling to 1.0%Y/Y in October, from 1.4%Y/Y in September. And it helps to validate some of the food price falls seen in the official ONS CPI release - particularly on the ambient side. This seems to support that food price inflation may already have peaked, and may therefore give more confidence to MPC members ahead of the November policy decision.

- In GBP STIR markets, SONIA futures are +0.5 to +4.0 ticks through the blues. BOE-dated OIS price ~7bps of easing through November, and ~17bps of easing through year-end (the latter 1.5bps more dovish than yesterday's close)

Figure 1: 10-year Gilt Yields (Source: Bloomberg Finance L.P)

SWEDEN: Riksbank Q3 Business Survey: Initial Summary Screens Dovish

Riksbank Q3 Business Survey is here. Initial headlines/summary screens dovish on net, but we still think the bar to another rate cut is high (and economic weakness suggesting another cut was needed would have to be confirmed by hard data)

Title: “We’re waiting for the upturn”

- "Sweden’s major companies describe the economic situation as a long and protracted slump that has not improved since the spring. Industrial activity has weakened, while the trade sector is reasonably satisfied with the situation. "

- "Sweden’s major companies describe the economic situation as a long and protracted slump that has not improved since the spring. Industrial activity has weakened, while the trade sector is reasonably satisfied with the situation.

- "Households are still perceived to be cautious and keeping a tight grip on their wallets. Businesses are hopeful that a lower level of interest rates and upcoming fiscal policy stimulation measures will boost demand and investment, but they expect it to take time."