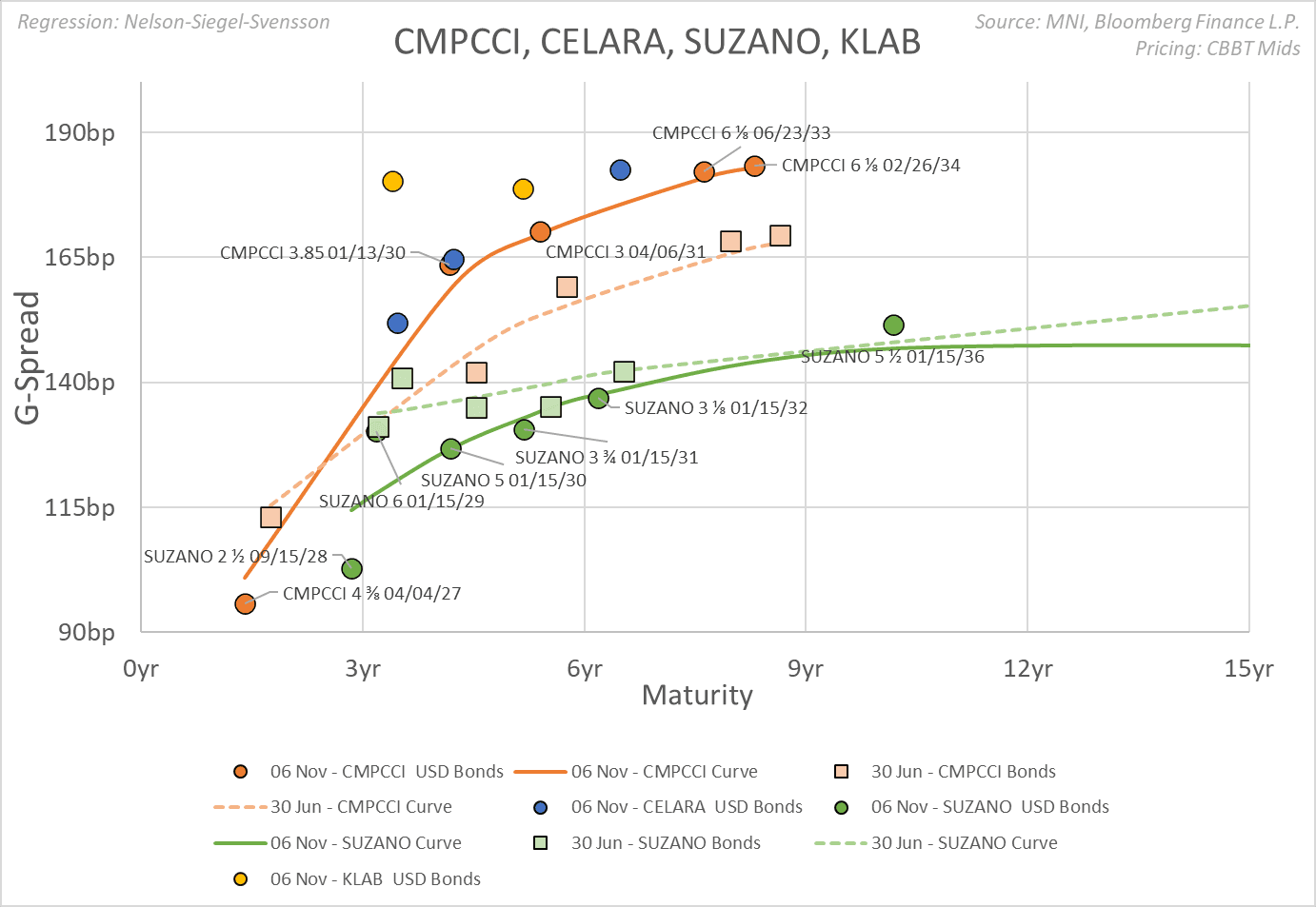

EM LATAM CREDIT: CMPC: Q3 2025 Earnings – Negative

(CMPCCI: NR/BBBneg/BBBneg)

• The drop in pulp prices which negatively impacted Brazil based Suzano (Baa3pos/BBB-pos/BBB-pos) earnings also hurt CMPC EBITDA which dropped 40% YoY from a large decline in EBITDA margin of 7.8pp. As a result, net debt/adjusted EBITDA rose to 3.79x vs 3.65x the previous quarter and 3.3x a year ago but market impact should be limited as CMPC’s negative credit trend has already been factored into spreads.

• CMPCCI 34s were last quoted T+166bp, 14bp wider since June 30th and 26bp wider YTD. When comparing the CMPC bond yield with lower rated Suzano in the 2031 maturity we observe a 36bp wider spread to account for the negative credit profile trajectory which widened out from flat five months ago and was 30bp through Suzano seven months ago. CMPCCI 31 yield is quoted flat to much lower rated Brazil based paper company Klabin (KLAB; Ba1/BB+/BB+).

• Comparing the CMPC subordinated hybrid bonds with another cyclical name in the market with a similar structure lower rated but more stable credit profile, Mexico based global cement producer CEMEX (CEMEX; Baa3/BBB-/BBB-), we see a 40bp wider spread than lower rated CEMEX so to some extent a lower rating for CMPC appears to be expected.

• Fitch moved their ‘BBB’ rating to negative outlook July 2025 reflecting weak pulp prices and increased leverage, so the company likely has at least until Summer 2026 to improve operations before ratings are affected. We see a shorter-term negative rating scenario at S&P that expressed disappointment February 2025 when they moved their outlook to negative on the ‘BBB’ rating, saying it was the third year in a row that leverage was above their 3x comfort level. We anticipate a one notch downgrade by S&P to BBB- within the next six months.

• EBITDA for the pulp segment fell 49% YoY despite flat pulp production because of a drop in pulp prices.

• Tissue sales rose 3% YoY but Tissue EBITDA declined 13% from a depreciation in local currencies in Latin America and a highly competitive environment which pressured prices as well as increased production capacity, especially in Brazil.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS/SUPPLY: WI 10Y Re-Open

WI 10Y stable at 4.117% ahead of the $39B 10Y note auction re-open (91282CNT4) cut-off at 1300ET, compares to last month's stop: drawing 4.033% high yield vs. 4.047% WI.

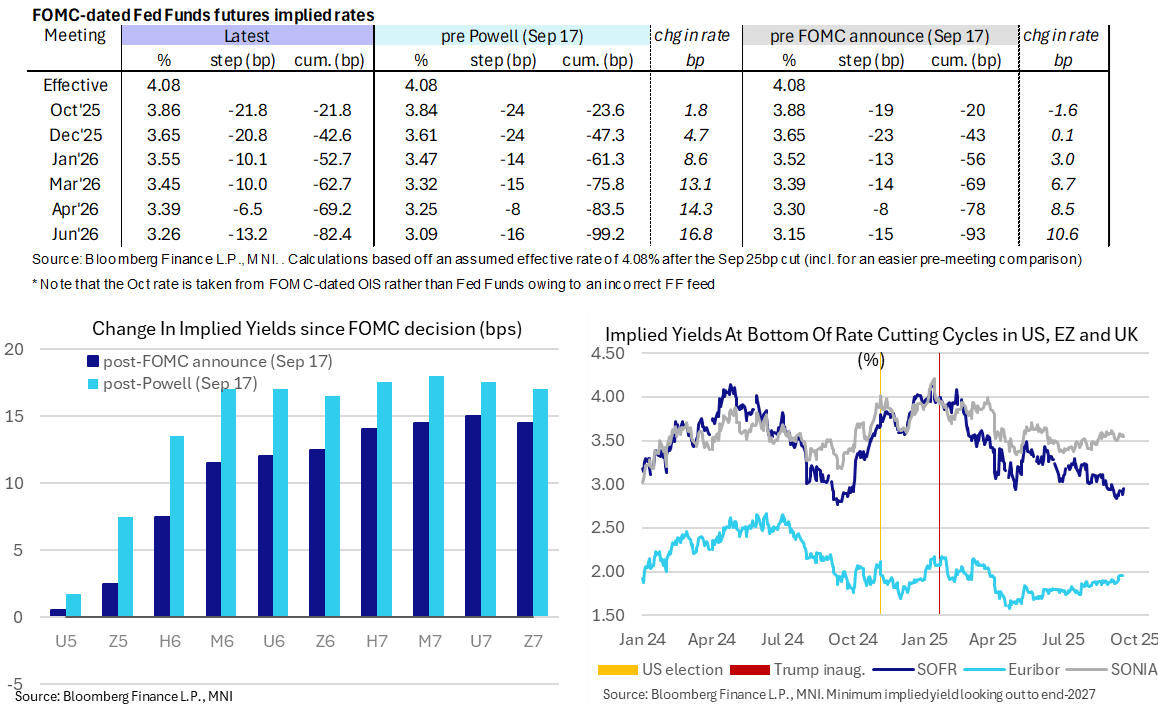

STIR: Near-Term Rate Path Back Close To Pre-ADP Levels, FOMC Minutes To Come

- Fed Funds implied rates are towards their most hawkish of the day, with the Dec implied rate for example back close to levels prior to last week’s soft ADP release.

- Further gains for crude oil futures (WTI 1st +1.3%) and S&P 500 e-minis back at record highs are likely in the driving seat.

- Moves are still relatively modest on the day, with 1.5bp increases for Dec and Jan meetings and 2.5bp higher through Mar-Jun meetings.

- Cumulative cuts from 4.08% effective: 22bp Oct, 42.5bp Dec, 52.5bp Jan, 62.5bp Mar, 69bp Apr and 82.5bp June.

- SOFR futures also see modest losses, sitting 2 ticks lower through H6-H7 contracts.

- The SOFR implied terminal yield of 3.07% is back in the SFRH7 after technically tilting into the Z6 on Monday for the first time since mid-July. It roughly points to 100bp of cuts ahead.

- Fedspeak has indeed been a non-event today although we are still to get the FOMC minutes at 1400ET - see the above posts starting 1121ET for a more detailed take on what to look for. That's barring any spillover to front rates at the upcoming 10Y auction at 1300ET.

FED: US TSY 9Y-10M AUCTION: NON-COMP BIDS $78 MLN FROM $39.000 BLN TOTAL

- US TSY 9Y-10M AUCTION: NON-COMP BIDS $78 MLN FROM $39.000 BLN TOTAL