FED: Citi and Morgan Stanley Delay Rate Cut Calls After Payrolls

Jan-09 16:46

Morgan Stanley now look for 25bp cuts from the Fed in June & September vs cuts in January & April. They maintain their terminal call with a target range at 3-3.25%.

- “Given the improved economic momentum and the decline in the unemployment rate, we see less need for near-term cuts to stabilize the labor market.”

- Specifically: "Third quarter GDP surprised to the upside, with unexpected strength in consumer spending on services, among other items. Incoming data for the fourth quarter also point to relative strength, despite the federal government shutdown. In addition, the unemployment rate in December fell to 4.4% (4.375% to three decimals) and the November unemployment rate was revised lower to 4.5%."

- “Instead, we now think the Fed will cut rates as it becomes clear tariff pass-through is complete and inflation is decelerating toward the 2.0% target.”

- “We expect disinflation to begin in 2Q 26 with y/y rates of inflation slowing around mid-year. If so, the Fed can then further normalize its stance.”

Reuters earlier reported that Citi now expect the Fed to cut 25bps in March, July and September vs January, March and September previously seen.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OPTIONS: Larger FX Option Pipeline

Dec-10 16:44

- EUR/USD: Dec12 $1.1550(E1.3bln); Dec15 $1.1600(E2.3bln), $1.1650(E1.2bln), $1.1680(E1.1bln)

- USD/JPY: Dec12 Y155.00($1.2bln); Dec15 Y156.50($1.1bln)

- GBP/USD: Dec12 $1.3240-55(Gbp1.1bln); Dec16 $1.3500(Gbp3.5bln)

- USD/CAD: Dec12 C$1.3780-00($1.6bln)

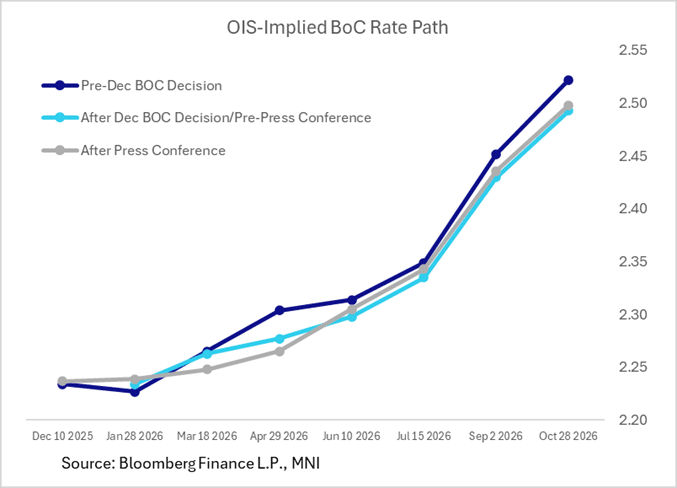

BOC: MNI BoC Review-Dec 2025: Data Seen Solid, But Not Yet Material

Dec-10 16:37

We've just published our review of the December BOC meeting - Download Full Report Here

- As largely expected the BOC produced a fairly neutral appraisal of the economy and rate outlook alongside the unanimously-expected overnight rate hold at 2.25%.

- The market reaction to the decision release was slightly dovish (about 2-3bp of implied hiking taken out of the path over the next 7 meetings), reflecting the Statement's downplaying of recent upside surprises in macro data developments.

- The post-meeting press conference saw little further shift in rate expectations, with Gov Macklem acknowledging the resilience in the Canadian economy evident in the latest data, but highlighting that it “hasn’t fundamentally changed our view”.

- Coming out of the meeting, markets price in 25bp of cumulative hikes through the October 2026 meeting, vs 27bp prior, with the path through H1 2026 almost completely flat.

- Attention turns to two key data releases to round out the year: November CPI (December 15) and October GDP (December 23), with the December labour report (January 9) and CPI (January 19) the key releases ahead of the Bank of Canada’s next decision on January 28 (1bp of cuts priced).

- See PDF report for:

- MNI View

- MNI Instant Answers

- Press Conference Transcript

- BOC Meeting Links

- Policy Statement Changes

FED: US TSY 17W BILL AUCTION: HIGH 3.610%(ALLOT 97.45%)

Dec-10 16:32

- US TSY 17W BILL AUCTION: HIGH 3.610%(ALLOT 97.45%)

- US TSY 17W BILL AUCTION: DEALERS TAKE 29.56% OF COMPETITIVES

- US TSY 17W BILL AUCTION: DIRECTS TAKE 5.11% OF COMPETITIVES

- US TSY 17W BILL AUCTION: INDIRECTS TAKE 65.33% OF COMPETITIVES

- US TSY 17W BILL AUCTION: BID/CVR 3.04

Trending Top

May-28 10:51

May-28 04:59