CHINA PRESS: CIPS Daily Trading Volume Exceeds CNY1 Trillion

The Cross-border Interbank Payment System (CIPS) processed CNY1.22 trillion in transactions in a sin...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA: Markets Wait for NPC Output, RRR Cuts Remain Favoured

- China's bonds are trying to post a modest recovery Tuesday after the largest drop of the year Monday. The 10-Yr is up +.025 to 108.335, having fallen -0.235 yesterday.

- The 2-Yr is up +.016 to 102.47 having fallen -0.052 yesterday.

- Cash is also marginally better with the 10-Yr CGB back at 1.80 having closed at 1.814% yesterday.

- Markets await any policy response from the NPC. The government has lowered its 2026 GDP growth target to 4.5%–5%, down from "around 5%" in previous years, signalling a shift toward "high-quality" growth over raw speed. Finance Minister Lan Fo'an indicated that fiscal expenditure and new government bond issuance will reach record highs this year. The headline budget deficit target is set at 4% of GDP, consistent with 2025 levels, to provide stable macroeconomic support.

- The PBoC is expected to implement incremental rate cuts and reductions in the Reserve Requirement Ratio (RRR) to maintain ample liquidity for a "strong start" to the new Five-Year Plan.

- Forecasts are for a 50bps cut which would add CNY1tn of liquidity to the interbank system and help support bond yields.

US TSYS: Yields Resume Climb, 10-Yr Back Above 4.10% - Risk of 4.20% Growing

UST yields resumed their ascent in Asia Tuesday with cash up 2-2.5bps across the curve. The 10-Yr has re-taken its position north of 4.10% and we see risks rising (in the short term) for the 10-yr to reach 4.20%.

- The 2-Yr is up +1.9bps at 3.561%

- The 5-YR is up +1.8bps at 3.705%

- The 10-yr is up +1.2bps at 4.111%

- The 30-Yr is up +0.9bps at 4.725%

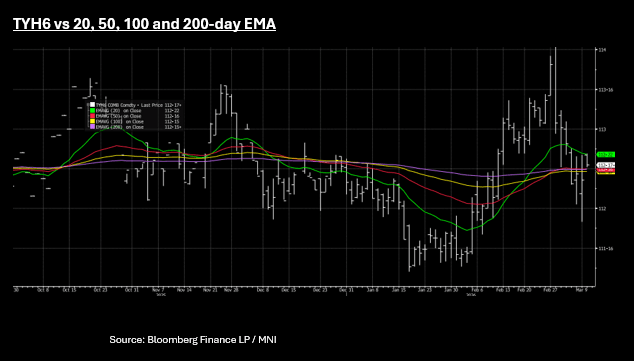

Futures are however higher on relatively light volumes Tuesday with the 10-Yr up +06 to 112-17+. TYH6 is wedged between the coverged 50-day / 200-day EMA at 112-15+ as lower resistance and the upper resistance via the 20-day EMA at 112-22+. A convergence of the 50-day and 200-day Exponential Moving Averages (EMAs) suggests a period of indecision and a lack of definitive market momentum.

Key out this week is CPI for February. Forecasts expect the annual inflation rate to hold steady at 2.4%, matching the January reading. This February report covers the period before recent energy price spikes caused by geopolitical conflicts meaning it may appear tamer than current real-time costs suggest.

There is a US$90bn 6-week auction anda US$58bn 3-Yr scheduled. Auctions Monday saw bid to cover's lower than prior.

BOJ: Rinban Purchase Offer

The BoJ offers to buy a total of Y700bn of JGBs from the market:

- Y270bn worth of JGBs with 1-3 Years until maturity

- Y260bn worth of JGBs with 5-10 Years until maturity

- Y95bn worth of JGBs with 10-25 Years until maturity

- Y75bn worth of JGBs with 25+ Years until maturity