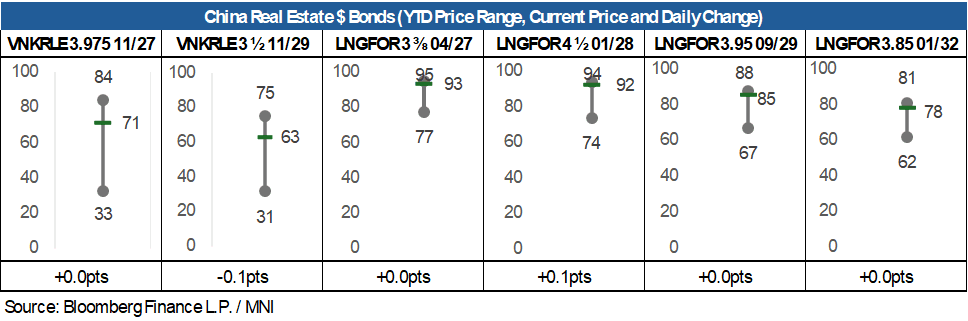

EM ASIA CREDIT: China Vanke: Results poor, liquidity risks rising

(VNKRLE, Caa3neg/B-neg/CCC-)

Results very weak, liquidity remains poor, shareholder support required

China Vanke reported its 9M25 results overnight, revealing operating losses of CNY11.2bn compared to a loss of CNY1.9bn in the same period last year. The cash ratio remained low at 0.4x at the end of the quarter, unchanged since H1, with a substantial shortfall of CNY91bn.

Access to liquidity remains the crucial factor driving the credit story. Financial support from its largest shareholder, Shenzhen Metro, continues, with shareholder loans reaching CNY29.13bn by the end of Q3. Nonetheless, the company acknowledged that 'The tight liquidity situation is intensifying, and the Company faces pressure in debt repayment.'

From a valuation perspective, the USD bonds maturing in 2027 and 2029 have declined by about 10 points since reports surfaced in September of strategic delays in interest payments aimed at securing better terms from lenders, alongside the resignation of its chairman.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Cash Bond Bear-Steepener, Tankan Broadly In Line

In Tokyo morning trade, JGB futures are little changed, +2 compared to settlement levels.

- The Q3 Tankan survey printed in line with expectations and Q2 but FY25 capex intentions increased 1pp to 12.5%. Large company business conditions have been moving sideways at a solid level since the start of last year, especially for the non-manufacturing sector.

- The large manufacturers’ index rose 1 point to 14 in Q3 while the outlook for Q4 is forecast to deteriorate 2 points. The series has not been affected by new US tariffs and the 2025 average is slightly higher than 2024’s.

- Non-manufacturers’ conditions were steady at 34, well above the series average of +7.3, with the outlook at 28.

- Small non-manufacturers are also outperforming manufacturers with the index at 14 (down 1 point) compared to +1 (stable). The outlook for both sectors improved 1 point.

- The September BoJ summary of opinions showed a bias towards a resumption of tightening.

- Cash US tsys are slightly cheaper in today’s Asia-Pac session after yesterday’s modest twist-steepener.

- Cash JGBs are little changed across benchmarks out to the 10-year, and 1-2bps cheaper beyond.

- Swap rates are flat to 2bps higher, with a steepening bias. Swap spreads are mixed.

AUSSIE BONDS: ACGB Dec-34 Auction Result

The AOFM sells A$1200mn of the 3.50% 21 December 2034 bond, issue #TB168:

- Average Yield (%): 4.2868 (prev. 4.0895)

- High Yield (%): 4.2875 (prev. 4.0925)

- Bid/Cover: 2.1033x (prev. 3.1708x)

- Allotted at Highest Accepted Yld as % of Bid at that Yld (%): 92.1 (prev. 12.2)

- Bidders: 30 (prev. 35), 11 (prev. 18) successful, 3 (prev. 11) allocated in full

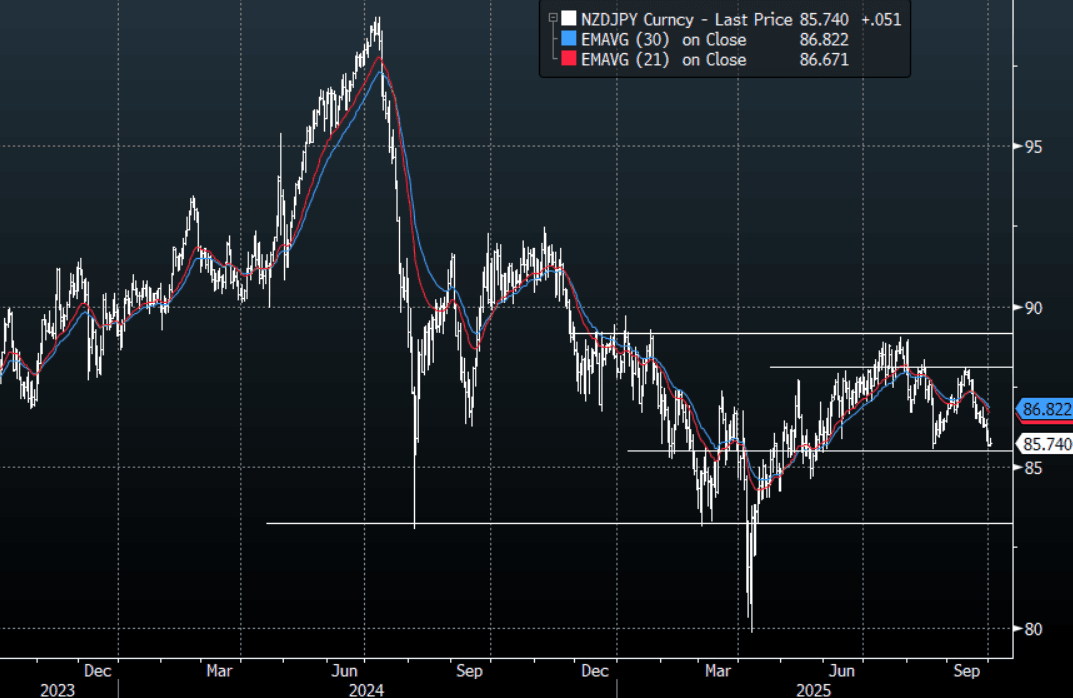

FOREX: JPY Crosses - The JPY Underperformance Starts To Retrace In The Crosses

US equities continued to grind back towards its all-time highs brushing off concerns of an imminent US shutdown overnight. This morning US futures have opened lower on our open as the shutdown begins to be executed, E-minis(S&P) -0.35%, NQZ5 -0.45%. The JPY outperformed across the board in the crosses, NZD remains the standout to be long JPY against.

- EUR/JPY - Overnight range 173.39 - 174.05, Asia is trading around 173.80. The pair topped out around 175.00 and has pulled back as upward momentum stalled. First support back toward the 173.00/173.50 area saw demand return overnight but the move is starting to look stretched.

- GBP/JPY - Overnight 198.59 - 199.31, Asia trades around 199.05. This pair has failed again to move above the 200.00 area. Buyers need to reassert the momentum higher again soon or the probability of a deeper pullback increases. In the middle of its recent 198.00-201.00 range, first support is seen back towards the 198.00 area.

- NZD/JPY - Overnight range 85.66 - 85.97, Asia is currently dealing 85.75. The pair continues to grind lower but is approaching some support. I continue to have a bias lower and would look for bounces to fade. A sustained break back below 85.00/85.50 is needed to see the move begin to grow momentum.

- CNH/JPY - Overnight range 20.7008 - 20.7906, Asia is currently trading around 20.7500. The pair topped out toward the upper boundary of its recent 20.40-21.00 range, a sustained break back above the pivotal 21.00 area is needed to signal the start of the next leg higher targeting the 21.50 area.

Fig 1 : NZD/JPY Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P