EM ASIA CREDIT: China Resources Land: New USD FV estimate

(CRHZCH, Baa1/BBB+/BBB+)

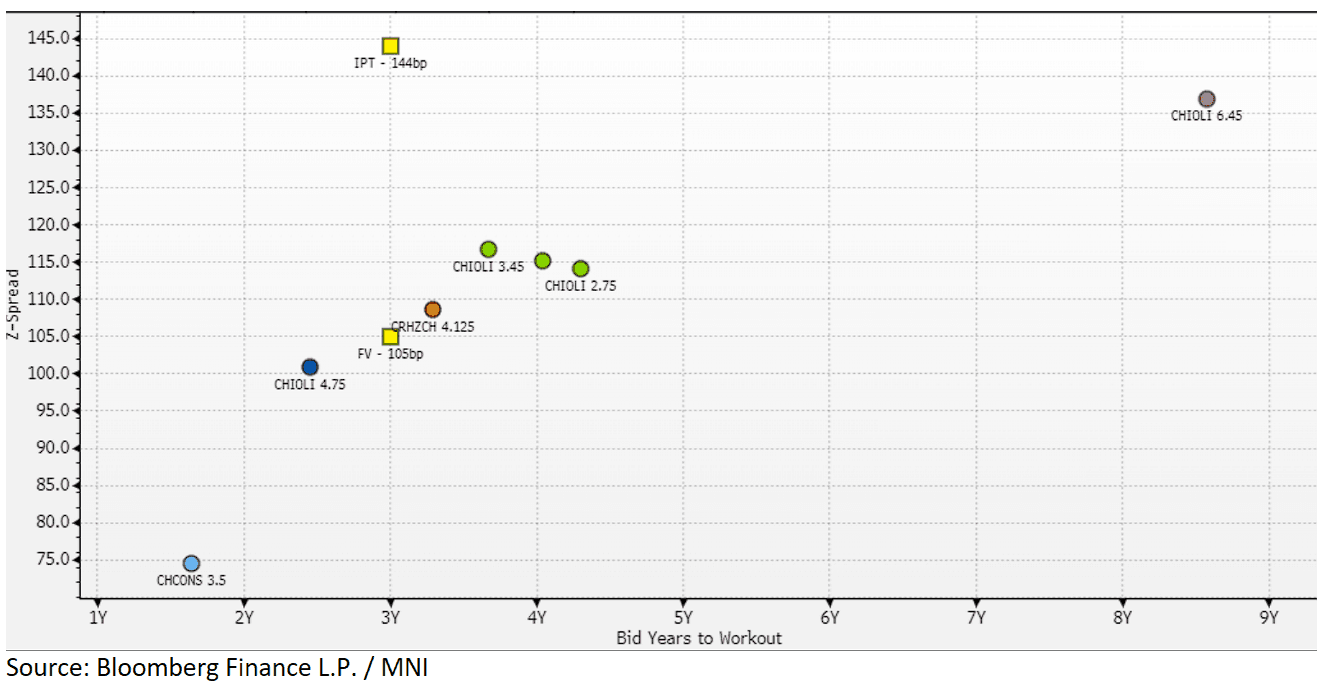

"*IPT: CHINA RESOURCES LAND $BMRK 3Y REGS GREEN NOTES +120 BPS A" - BBG

New Issue: 3Y USD benchmark

IPT: T+120bp (z+144bp)

FV: T+81bp area (z+105bp)

Real estate business, China Resources Land, is 60% owned by China Resources (Holdings), which in turn is owned by the China State-owned Assets Supervision and Administration Commission (SASAC). We expect state support if needed.

In terms of credit quality, Moody’s forecasts that earnings from both the property development business and the increasing share of recurring, higher-margin rental income will support EBITDA at around RMB 65-70 billion over the next 12-18 months. Leverage is expected to range between 4.0x and 4.5x in 2026.

In terms of fair value, we include the existing CRHZCH 2/29s, which acts an anchor for our assessment, as well as bonds from China real estate company, China Overseas Land (CHIOLI, NR/A-/A-). We believe fair value will be close to the CHIOLI curve at around z+105bp area.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA SETS YUAN CENTRAL PARITY AT 7.1021 TUES VS 7.1007

- CHINA SETS YUAN CENTRAL PARITY AT 7.1021 TUES VS 7.1007

RBA: Minutes Reflect More Caution Than Downside Concerns, Nov Hold Plausible

The RBA minutes clearly reflected the Board’s caution at the 30 September decision to keep rates unchanged. Its “decisions”, ie. not just last month’s, “remain cautious and data dependent”. Thus the outcomes of releases between now and 4 November are very important and the tone of the minutes was clear that a rate cut at that meeting is not a given. Today’s September NAB business survey was consistent with an ongoing recovery in activity.

- There were a number of observations that suggest the Board may hold again. It noted that “early indicators” for Q3 showed private demand could be recovering a bit faster than expected, so not just the backward-looking Q2 GDP data, and that it may have underestimated consumption growth in August. Also on growth, the US is “steady” and the risk from “higher tariffs” has “diminished”, while fiscal policy should support a weaker China.

- Not only do the July/August CPI outcomes suggest Q3 inflation may be higher than the RBA expected in August but that combined with “broadly stable labour market conditions” may imply that it underestimated the extent of capacity pressures. As Governor Bullock noted, elevated services in other countries may have “potential lessons for Australia” too.

- Monetary policy is deemed “restrictive” but the RBA doesn’t know by how much. It is seeing the impact of previous easing on housing and credit growth and it knows that it hasn’t fully fed through. It seems to be slightly uncomfortable with the current effect of easier financial conditions.

- There was little discussion of downside risks with the only consideration in the minutes that staff projections “were not taking sufficient signal” from “persistent weakness in consumer sentiment”, softer employment and “timely indicators of wages”.

- Key data coming up include 29 October Q3 CPI, 16 October September jobs, 31 October September private credit and 3 November September household spending.

US TSYS: Treasury Yields Edge Higher in Morning Session

- As treasuries begin trading in the Asia trading day, yields across the curve have opened 1-3bps higher.

- The US 2-Yr is +1bp at 3.515%, having traded near to 3.50% but was unable to break below.

- The US 5-Yr is up +2bps to 3.649% having closed prior to Columbus day at 3.626%.

- The US 10-Yr is up +3bps to 4.067% having failed to test 4.00% and looks likely to remain in the 4.00% - 4.20% range for now, seeking a fresh catalyst to break out.

- The US 30-Yr is up +3bps at 4.65%

- Futures are edging lower too as TYZ5 is down -02 at 113-02