US-CHINA: China Asks Banks To Pause New Loans To US-Sanctioned Oil Firms - BBG

Headlines have crossed from BBG that China has asked banks to pause new loans to US-sanctioned oil r...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

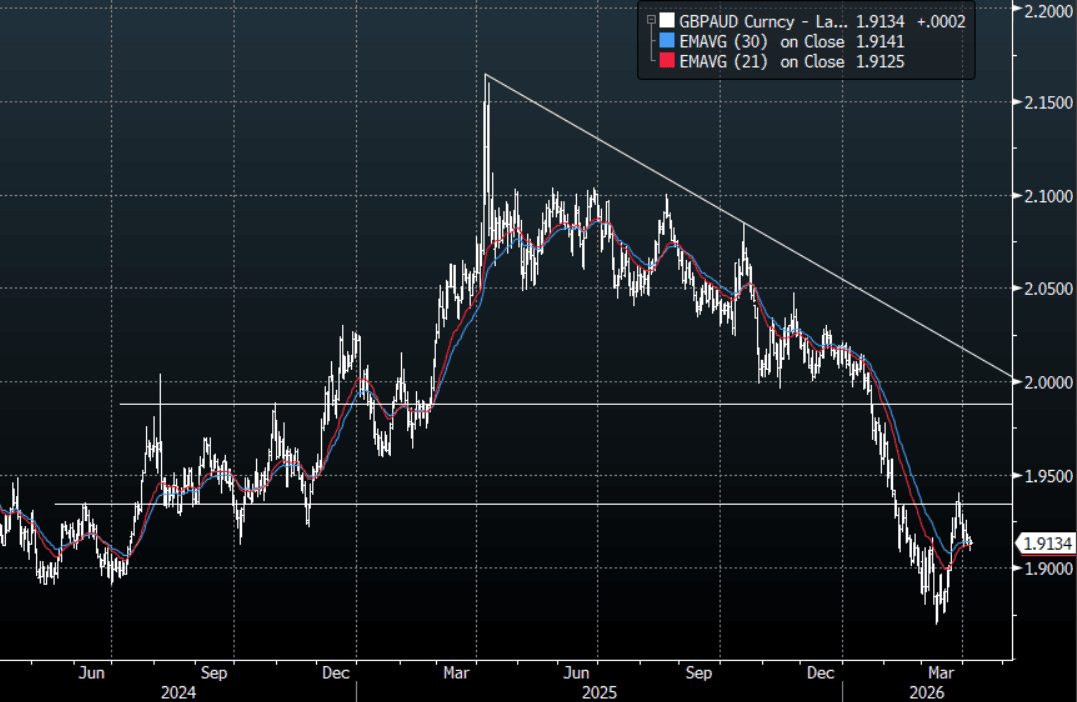

AUD: GBP/AUD - Finds Support Initially Back Toward 1.9100

The GBP/AUD range overnight was 1.9104-1.9152, Asia is trading around 1.9130. The pair continues to find short-term support back toward the 1.9100 area as the Trump deadline looms. I am personally skeptical of this relief rally and am not sure how global growth will look should the deadline expire and we see US troops on the ground. The first support on the day is pretty close between 1.9070-1.9100 and then the 1.9000 area. There is a good chance we chop around in a whippy 1.90-1.94 range while the market looks for clarity on how this conflict is set to unfold, the longer it drags on the worse it is for risk and then by proxy potentially the AUD.

- The GBP/AUD Average True Range(ATR) for the last 10 Trading days: 100 Points

Fig 1: GBP/AUD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

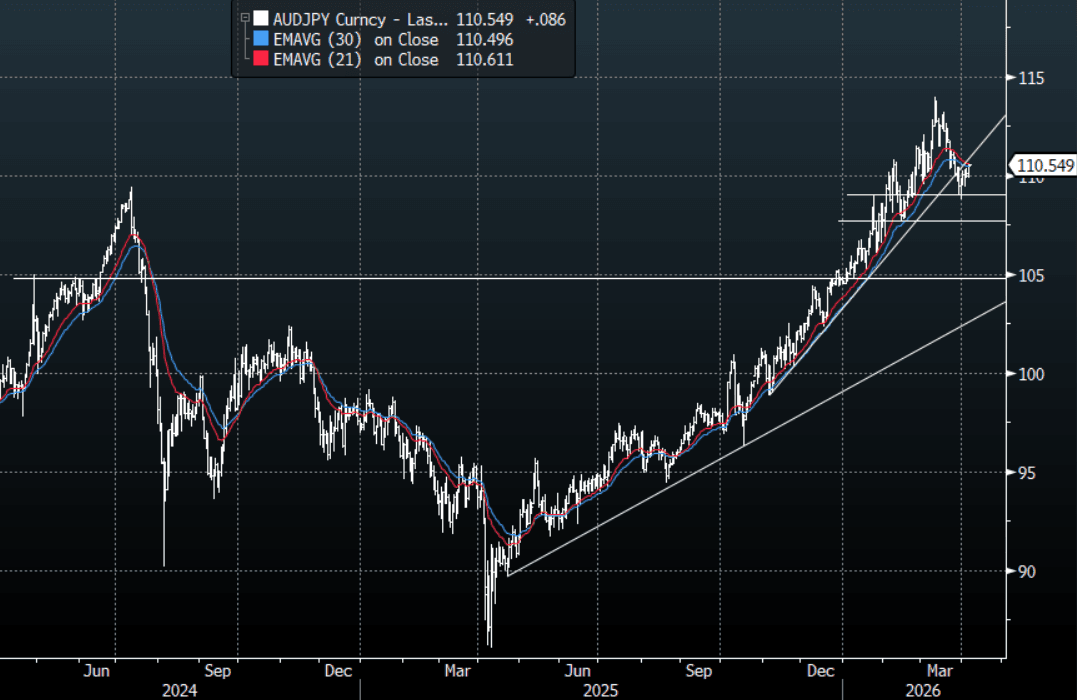

AUD: AUD/JPY - Looks Toward Trump Deadline For Clearer Direction

The AUD/JPY range overnight was 110.21-110.59, Asia is currently trading around 110.55. The pair has drifted higher as US equities hold onto hopes of a solution being found before the deadline or just simply believe he will “TACO”. Technically the trend remains up, and the pair has traded very well considering the negative risk sentiment from geopolitics. The inability for the Yen to bounce meaningfully in the crosses during this period of upheaval has been telling. On the day, all eyes on the approaching deadline, I remain very skeptical and err on the side of a potential escalation. AUD/JPY could test the 111.00-111.50 area, but there remains lots of scope for disappointment as well which would see another test of the support around 109.00. Looks like we could chop around in a 108.50-111.50 range as risk looks for some clear direction.

- The AUD/JPY Average True Range(ATR) for the last 10 Trading days: 74Points

Fig 1: AUD/JPY spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

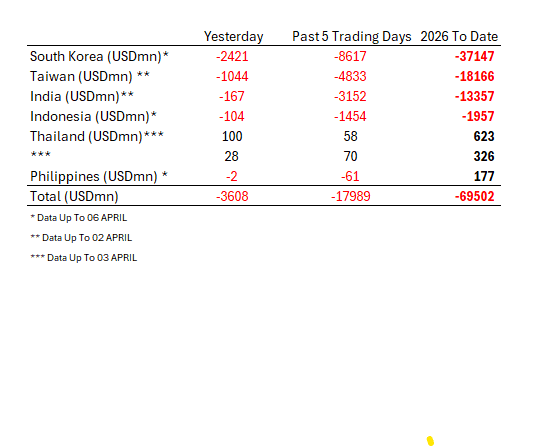

ASIA STOCKS: Huge Outflows Continue for Korea as YTD Totals Near $70bn

Whilst the various holidays over the recent weekend mean that the release of data is varied from country to country, there is no doubt of the key theme across key equity markets in Asia - Outflows.

Being one of the markets open yesterday, Korea saw yet again another day of significant outflows, over $2bn left, taking their year to date outflows to just North of $37bn. This coincides with a period of further instability for the KOSPI, now down over 10% from the late February highs as investors lock in profits from the huge moves in tech/AI names.

Indonesia reported flows as of the 6th also and continues to see consistent, modest outflows, now nearing $2bn year to date. MSCI's upcoming key deadline for Indonesian stocks is the May 2026 Index Review, which will determine if the country remains an Emerging Market or is downgraded to Frontier Market status.

Taiwan's flows as of the 3rd continued to be negative with over $1bn outflow recorded as year to date hit $18bn. The TAIEX is down just over 8% from the February highs, with flagship AI stock TSMC down -4.2% over the last month.

India's outflows as of the 2nd were modest but has had over $3bn out in the last five trading days.

In total, year to date the key markets have now seen almost $70bn of outflows.