US DATA: Chicago Business Barometer™ - Slipped To 44.6 in April

The Chicago Business Barometer™, produced with MNI slipped 3.0 points to 44.6 in April. This more than reverses March’s 2.1 point rise, but still leaves the index above January’s 39.5 reading. The index has been in contraction for seventeen consecutive months.

- The decrease was driven by a pullback in new orders and production, and to a lesser extent supplier deliveries. Order backlogs and employment rose relative to March.

- Production dropped 7.6 points to 47.9, almost fully unwinding March’s rise.

- New orders fell 7.0 points, the lowest since December 2024.

- Employment inched up 0.4 points to 37.6. This index has been below 40 for eight of the last twelve months.

- Order backlogs progressed 2.3 points.

- Supplier deliveries pared 1.4 points. The index has been above 50 for ten of the last twelve months.

- Inventories increased 17.0 points, potentially reflecting tariff front-loading. This was the highest level since November 2023, with 31% of respondents reporting larger inventories, up from 12% in March.

- Prices paid consolidated 1.3 points to 78.0, the highest level since August 2022.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

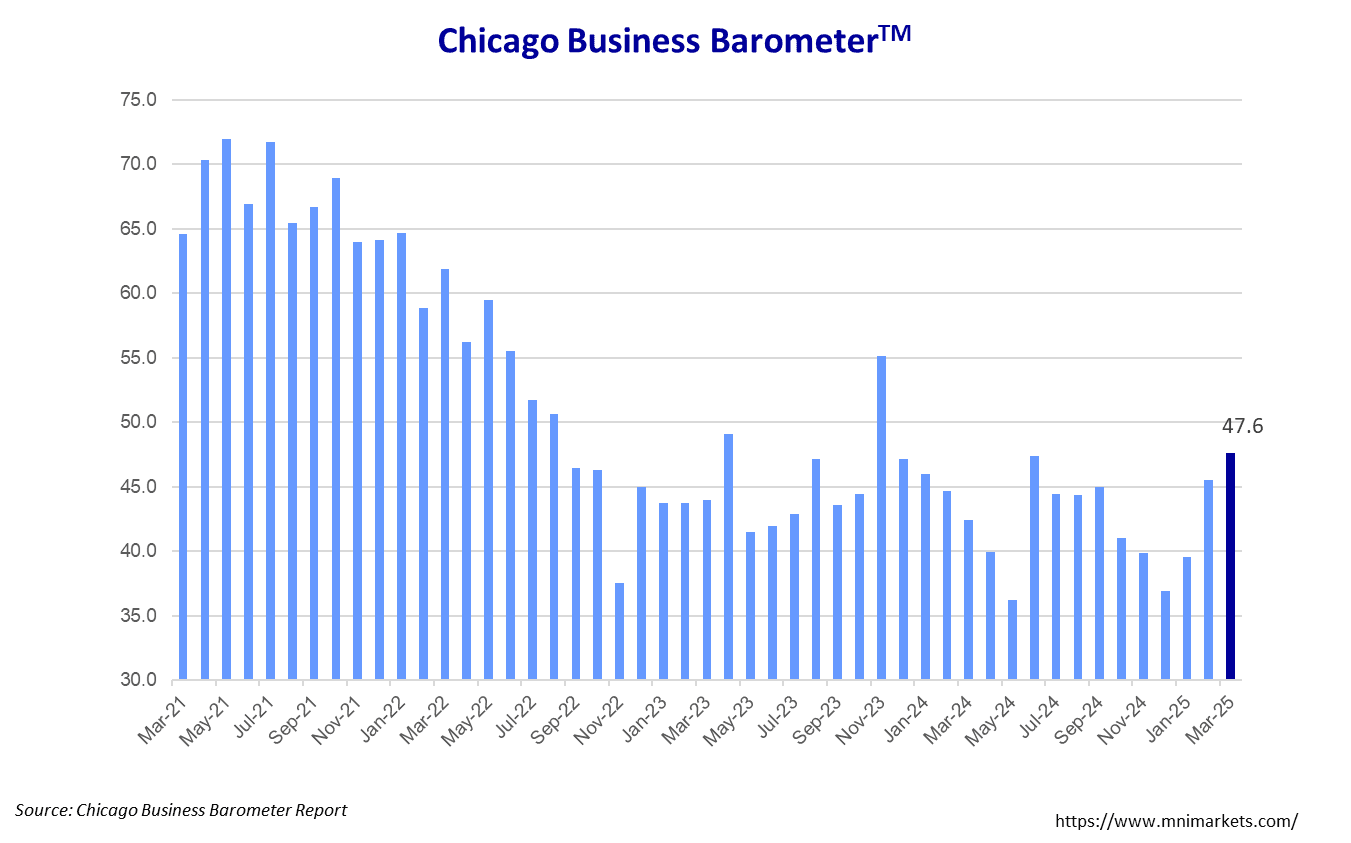

US DATA: Chicago Business Barometer™ - Advances to 47.6 in March

The Chicago Business Barometer™, produced with MNI advanced 2.1 points to 47.6 in March. This is the third consecutive monthly gain, taking the index to its highest level since November 2023, though it remains in contractionary territory for the sixteenth successive month.

- The increase was largely driven by a rise in Production, with smaller increases in Employment, Order Backlogs and New Orders also contributing whilst Supplier Deliveries declined.

- Production increased 8.8 points to 55.5, to the highest since December 2023, taking it into expansionary territory for the first time since June 2024.

- New Orders saw a minor 0.4 point rise, with the subindex last higher than this in November 2023.

- Employment lifted 0.9 points to 37.2, only a marginal improvement from January 2025 which had recorded the lowest level since June 2020.

- Order Backlogs progressed by 0.7 points, remaining the highest since September 2024.

- Supplier Deliveries dipped 2.0 points.

- Inventories fell 6.5 points to the lowest level since March 2020.

- Prices Paid edged down a marginal 0.4 points to 76.7, keeping the reading the second highest print since August 2022. No respondents reported lower prices for the second consecutive month.

GILTS: Back Towards Highs As U.S. Equities Weaken

Little to really shape gilt trade since the early risk-off rally driven by tariff risks, with the pullback in Bunds detailed elsewhere helping gilts trade away from highs through the European morning.

- Futures back towards session highs as U.S. equities come under fresh pressure after the cash open.

- Initial Fibonacci resistance (92.17) protects trendline resistance drawn off the March 4 high (92.55).

- Yields 3.5-4.5bp lower, 10s outperform.

- A reminder that the DMO will hold its consultations regarding FQ1 (April to June) issuance at 15:30BST (investors) and 17:00BST (GEMMs) today.

- The DMO auction calendar for the remainder of the quarter is due to be released on Friday at 7:30BST.

- We set out our expectations for gilt issuance across FY25/26 in our UK Issuance Deep Dive publication.

- SONIA futures flat to +7.0.

- BoE-dated OIS showing 19bp of cuts through May, 23bp through June, 35bp through August and 53bp through December. We still look for the next cut to come in May.

STIR FUTURES: BLOCK: SOFR Red Packs

- 2,000 SOFR Red packs (SFRH6-SFRZ6) +0.030 at 0931:32ET, appears to be swap-tied buying with spreads running mildly tighter in the vicinty