US ENERGY SECTOR: Chevron (CVX): 1Q26 Results

Credit neutral. Beat on bottom line, although top-line results came in slightly below consensus. Ear...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

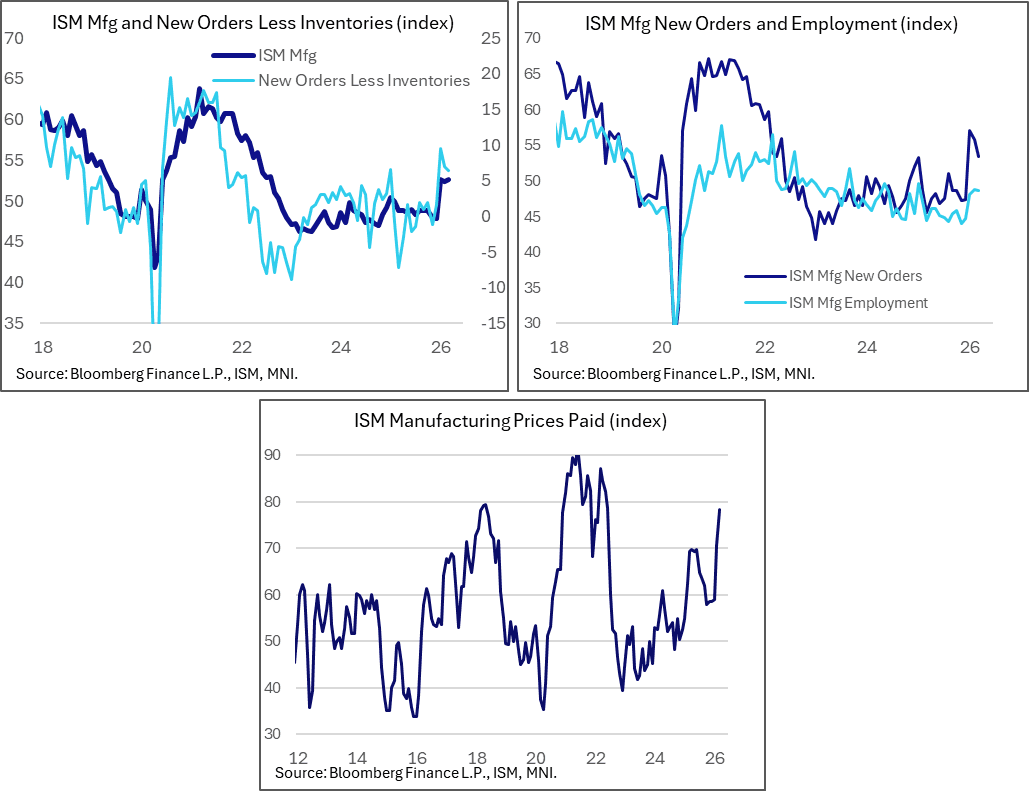

US DATA: ISM Manufacturing Price Jump Stands Out As War Impact Starts To Be Felt

March's ISM Manufacturing Report posted another solid set of activity readings, but came with another indication of soaring inflation. The data and anecdotal commentary provide some evidence that the conflict in the Middle East is already hampering supply chains and pushing up input costs.

- The headline PMI ticked up to 52.7 from 52.4 prior, besting the 52.3 expected, with the composite receiving contributions from New Orders (53.5 after 55.8, a 3rd consecutive expansion after 4 consecutive contractions though below the 54.5 expected), Production (55.1 after 53.5), and Supplier Deliveries (58.9 after 55.1). This was the highest (and therefore slowest) Supplier Deliveries reading since May 2022, indicative of supply chain pressures building.

- However, Employment fell 0.1pp to 48.7, the 38th month in the last 39 of contraction. "Of the six big manufacturing industries, two (Transportation Equipment; and Machinery) reported higher levels of employment in March. For every comment on hiring, there was 1.2 on reducing head counts."

- The key surprise was in Prices Paid: they soared to 78.3 (74.0 expected) from 70.5 and have now risen 19+ points in 2 months to another fresh post-June 2022 high.

- Manufacturers are evidently feeling the pipeline pressures of tariffs as well as the latest spike in energy prices: “The Prices Index reading continues to be driven by (1) increases in steel and aluminum prices that impact the entire value chain, (2) tariffs applied to many imported goods and now (3) increases in petroleum-based products as a result of the recent Middle East conflict."

- Business export orders slipped back below 50 (-0.4 points to 49.9) with a bigger pullback seen in Imports (-2.3 points to 52.6) but overall remained within recent ranges. Inventories dipped 1.7 points to 47.1, a 3-month low. New Orders less inventories remained relatively elevated, suggestive of sustained future output.

- Several respondents cited "geopolitical instability/tensions" and "Iran/Middle East war", in terms of increasing manufacturing supply costs, raising uncertainty, and weighing on sentiment. Per the report: "This month also marks the first report with panelists citing the Iran war as a new impact to their business, along with ongoing uncertainty with U.S. economic policy, despite the recent Supreme Court ruling striking down International Emergency Economic Powers Act (IEEPA) tariffs. In March, 64 percent of comments overall were negative. Among the negative comments, about 20 percent cited tariffs and about 40 percent the war in the Middle East."

EQUITY OPTIONS: Estoxx Put Spread

SX5E (19th June) 4800/4725ps, bought for 6 in 10k.

STIR: Firm ISM Prices Paid Provides Modest Hawkish Reaction

A firm prices paid component within the ISM manufacturing survey promotes another round of contained, knee-jerk hawkish repricing in US$ STIRs after the early NY data releases (ADP & retail sales) & President Trump’s latest threats against Iran provided some hawkish inputs ahead of the ISM data.

- SFRZ6 back from fresh session lows after a 2.0 move lower on the ISM data, contract back to flat on the day, 8.0 off highs. December FOMC-dated OIS prices ~6bp of cuts through year-end vs. ~12bp as NY participants started to filter in earlier today.