EMERGING MARKETS: CEEMEA FX Price Signal Summary: USDTRY Clears The Bull Trigger

Jul-19 11:09

- EURHUF has continued to pull away from recent highs. The trend outlook remains bullish however the break of the 20-day EMA and today’s extension lower, has exposed support at the 50-day EMA, at 395.88. A clear break of this EMA would highlight potential for a deeper retracement. The broader uptrend remains intact and a reversal higher would once again refocus attention on key resistance and bull trigger at 416.89, the ul 6 high.

- EURPLN has pulled back from last week’s high of 4.8515, Jul 12 high. A bullish theme still dominates following recent gains. 4.7446, the Jun 16 high, has been cleared and this signals scope for an extension towards 4.8976, the 76.4% retracement of the Mar 7 - May 30 bear leg. The 20-day EMA, at 4.7511, has been tested. A clear break would signal scope for a deeper retracement towards the 50-day EMA, at 4.7022.

- USDZAR remains below its most recent highs. Short-term pullbacks are considered corrective and the current uptrend remains intact. This follows recent gains that resulted in the breach of major resistance at 16.3668, the Nov 26 2021 high. Moving average studies are in a bull mode condition too. The break confirmed a resumption of a broader uptrend that started in June 2021. This sets the scene for an extension higher towards the 17.50 handle next. Initial firm support is at 16.6215, the 20-day EMA.

- USDTRY trend conditions remain bullish and the pair has cleared key resistance and the bull trigger at 17.4446, the Jun 22 high. A clear breach of this hurdle confirms a resumption of the primary uptrend and sights are on the 18.00 handle. Key support is unchanged at 16.0956, the Jun 27 low. The 20-day EMA, at 17.1530, marks initial support.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Falling Breakevens Help Cap Yield Gains

Jun-17 18:52

Treasuries traded weaker Friday, with a renewed rise in short-end yields bear flattening the curve.

- In a week dominated by big swings in Treasury yields and big equity declines, oil stole the show Friday, with WTI dropping 6.8% on the session.

- This helped 5Y and 10Y TIPS-implied breakevens fall to the lowest levels since February. In turn, that helped cap yield gains in an otherwise risk-on session, with the Nasdaq rallying in the afternoon.

- The 2-Yr yield is up 5.8bps at 3.1512%, 5-Yr is up 4.2bps at 3.326%, 10-Yr is up 2.9bps at 3.2237%, and 30-Yr is up 3.4bps at 3.2812%.

- Fed communications (George, Bullard, Kashkari) generally leaned hawkish where they leaned at all (nothing new from Chair Powell), helping pull short-end yields off session lows.

- Data (industrial production, leading index) added to the recent string of concerning reports but didn't draw any market reaction.

- With a market holiday Monday, attention will swiftly turn to Powell's congressional testimony next Weds and Thurs.

SNB: UBS: First rate hike since 2007

Jun-17 18:21

- We had expected a 50bp hike to happen only at the September meeting. The monetary policy statement

notes that "It cannot be ruled out that further increases in the SNB policy rate will be necessary in the foreseeable future to stabilise inflation in the range consistent with price stability over the medium term." - The SNB also dropped the sentence that the Swiss franc is "highly valued" in its policy statement as we had thought likely. The SNB has over recent months prepared the ground for a changed exchange rate assessment by arguing that the nominal appreciation does not entail an appreciation in real terms, given the inflation differential between Switzerland and abroad.

- They also retained the willingness "to be active in the foreign exchange market as necessary" to ensure appropriate monetary conditions, Chairman Jordan in his remarks specified that the SNB would consider selling foreign currency if the Swiss franc were to weaken. This is the most explicit reference so far that the balance sheet will also play a role in SNB policy normalisation.

- SNB announced that the tiering multiplier would be lowered from 30 to 28 from 1 July, as we had thought likely. This was done to ensure that a sufficient amount of sight deposits is subject to negative rates and to prevent upward pressure on money market rates. It can also be seen as sign that the banking system should prepare for the end of negative rates.

- Previously, we had expected the SNB to hike rates by 50bp in September, followed by four more 25bp hikes at the following meetings to bring the policy rate to +0.75% by September 2023. With the 50bp hike brought forward to June, we maintain our expectation for a 50bp hike in September (to +0.25%), followed by rate hikes at each forthcoming meeting by 25bp until March 2023, by which time the policy rate would stand at +0.75%. The SNB announced that from now it will hold press conferences after every meeting which will help to explain further rate hikes.

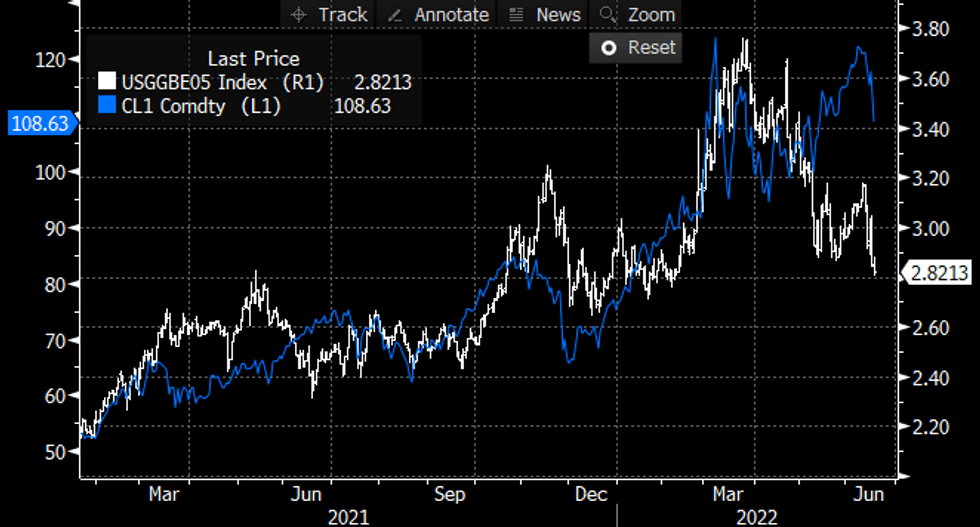

US: Inflation Breakevens Starting To Fall Alongside Oil

Jun-17 18:13

US 5Y and 10Y TIPS-implied inflation breakevens have quietly falling to multimonth lows today as Oil continues to correct, hitting a fresh post-February low. Here's 5Y which has fallen nearly 100bp since the late-March peak - has inflation peaked?

Source: BBG

Source: BBG