EM ASIA CREDIT: Cathay Pacific: Possible large Boeing order.

(CATHAY, NR)

"*CATHAY PACIFIC POISED TO MAKE FIRST BOEING ORDER IN 12 YEARS" - BBG

According to Bloomberg the order of new 777x aircraft will be made at the same time as the H1 earnings release today. No details yet on how many aircraft.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

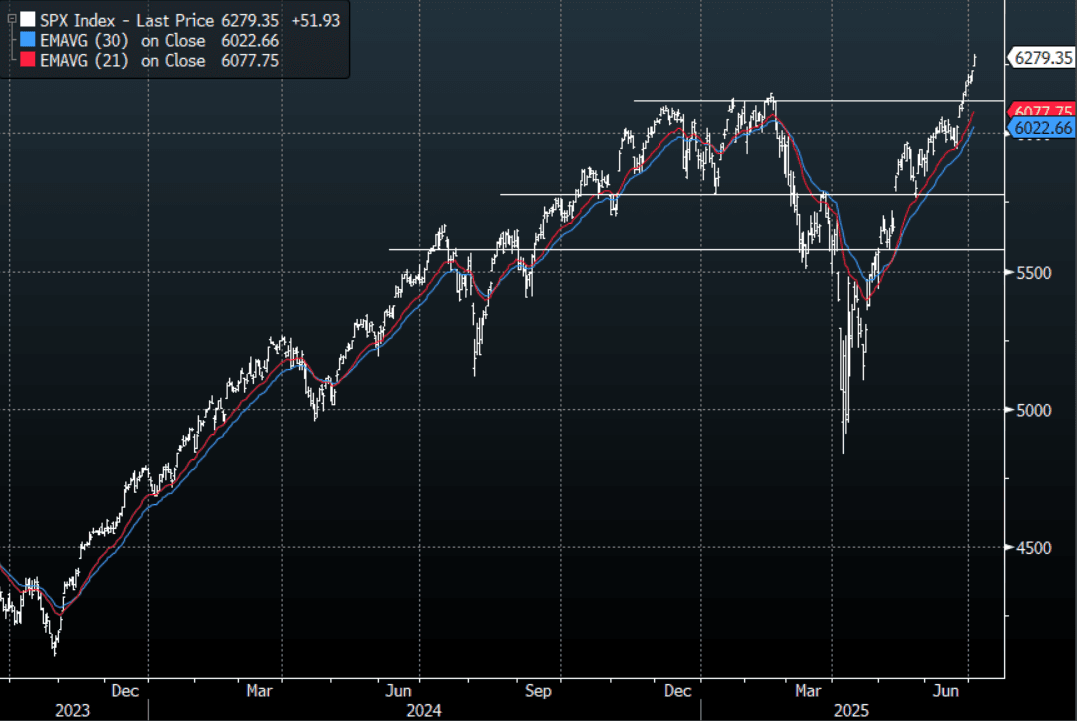

US STOCKS: Upward Momentum Stalling As Market Eyes The Tariff Deadline

The ESU5 Friday night range was 6276.50 - 6308.75, Asia is currently trading around 6300. US Equity futures drifted lower on Friday as the market began eyeing the tariff deadline this week. This morning has seen US futures open a little higher but still off the highs from last week, ESU5 -0.35%, NQU5 -0.40%. This week the tariff deadline will be closely watched by a market that looks to have a lot of positives already baked in the price.

- Wei Li Chief Strategist at Blackrock on Linkedin - “Big Beautiful Bill” could boost equity sentiment and push up term premium - still low to historical comparables - through worsening deficit. The Congressional Budget Office puts it at an additional, front-loaded, $3.25T in borrowing over 2025-34. I continue to favour US equities over long Treasuries.”

- Charlie Bilello on X: “ Over the last 17 years, US stocks have gained 592% vs. 140% for International stocks and 93% for Emerging Markets.”

- Mohamed A. El-Erian replied on X: ”This is a stunning out-performance. That’s the obvious remark, of course. Less obvious is where do we go from here as illustrated by those who feel that:

- (i) America’s valuation gap has grown to excessive levels and will be subject to some mean reversion which, as illustrated earlier this year, would translate into meaningful gains for the rest of the world: and

- (ii) Continued US outperformance is ahead given the deeply (structurally) embedded nature of the economy’s corporate innovation and competitive drive.”

- The market has been caught underweight and with momentum type funds(CTA’s) together with Retail adding through all-time highs these reluctant PM’s are being forced to return to the market.

- Short-term this does look a little overdone but dips are just non-existent at the moment as risk surges higher. Could the risks this week around the tariff deadline give the market some pause ? First support is back towards the 6000/6100 area.

Fig 1: SPX Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

US TSYS: Cash Open

TYU5 is trading 111-12, up 0-05 from its close.

- The US 2-year yield opens around 3.85%, down 0.03 from its close.

- The US 10-year yield opens around 4.322%, down 0.2 from its close.

- (Bloomberg) - US Treasuries are likely to be knocked off their podium as the best performing bonds in developed markets this year. Slower disinflation, swelling fiscal deficits, and a broader investor push toward diversification will hurt US debt relative to peers.

- (Bloomberg) - The Treasury’s willingness to fund more at the short-end of the yield curve will further compromise the Federal Reserve’s independence and increasingly leave monetary policy de facto in fiscal hands. The dollar will be a casualty, and the yield curve will steepen.

- “The world economy is about to get more clarity on trade deals as the US president's deadline for trade deals arrives on Wednesday, ending the 90-day reprieve from Trump's "reciprocal" levies.”(BBG)

- The 10-year yield has seen a strong bounce in reaction to the better NFP print. This 4.35/40% area offers those who would like to express a long the opportunity to fade. A sustained close back above 4.40/4.45% area though would not be great for the bulls and would see more of the longs prepared back.

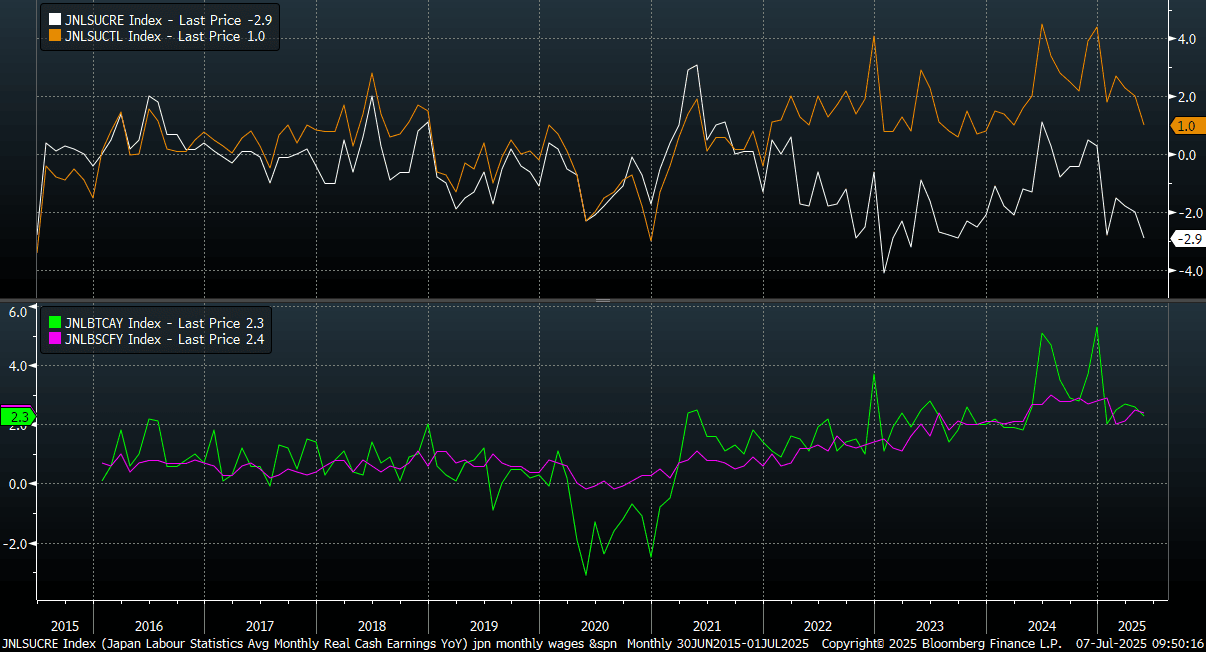

JAPAN DATA: Wages Weaker Than Forecast, Weighed By Bonus Payment Slump

Japan May labor cash earnings were weaker than forecast. Headline nominal cash earnings rose 1.0%y/y, versus a 2.4% forecast. The prior April outcome was also revised down to a 2.0% rise (initially reported as a 2.3 % gain). In real terms, earnings were down -2.9%y/y, against a -1.7% forecast and prior -2.0% outcome. For nominal earnings this is weakest outcome since Mar 2024, while in real terms it is back to Sep 2023 lows. See the top panel of the chart below. It also widens the trend with last Friday's stronger real household spending outcome.

- A slump in bonus payments, down -18.7%y/y, weighed on the headline results. Contracted and scheduled pay in y/y terms were little changed versus April levels. Bonus payments tend to be quite volatile (we were at +74.1%y/y in Feb), so there is scope for this to be less of a headwind in months ahead.

- On a same sample base, cash earnings were +2.3%y/y, below the 2.8% forecast and 2.6% prior outcome. Scheduled full time pay (on a same base) rose 2.4%y/y, also below market expectations (2.6% was the forecast and 2.5% printed in April). See the bottom panel of the chart below. These trends are more positive compared to the headline earning outcomes, but sit off 2024 highs.

- In this segment, special payments also fell 3.6%y/y, versus a +2% gain in April. Again, there is scope for this to be less of a headwind going forward.

- All in all, given the contribution of bonus payments to the headline fall it softens the negative message from today's print. The BoJ still have time on its hands to assess wages trends, with the near term bias likely to see rates left on hold.

Fig 1: Japan Labor Earnings Slowed In May, As Bonus Payments Fell

Source: Bloomberg Finance L.P/MNI