SONIA: Call fly buyer

Aug-22 10:58

SFIU4 95.20/95.25/95.30c fly, bought for half in 1.5k.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA: Risk-off Moves Across China Work Against Local Markets

Jul-23 10:51

A particular focus on Chinese markets overnight, where risk-off moves worked against both headline equity indices as well as relevant industrial commodities:

- CHINA (BBG): Chinese Stocks Slump Amid Signs National Team Is Pulling Back

Chinese stocks suffered their biggest decline in six months as a lack of major policy support following the Third Plenum reinforced bearish sentiment. The onshore benchmark CSI 300 Index closed 2.1% lower, following a 0.7% drop in the previous session. - CHINA (Yicai): PBOC Could Phase Out MLF

The PBOC could eventually phase out its medium term lending facility and use the DR series of overnight rates as the main policy tool, according to Wen Bin, chief economist at China Minsheng Bank. - CHINA (BBG): China’s Deadly Rains to Intensify as Tropical Storms Arrive

Heavy rains lashing China have left at least 26 people dead in the past week, flooding city streets and threatening farming and industrial activity, as two more tropical storms barrel toward the nation. - COMMODITIES (BBG): Iron Ore Buckles Below $100 as China’s Plenum Fails to Inspire

Iron ore crumbled below $100 a ton as a policy meeting in China failed to deliver major stimulus, while supplies stayed strong. The outcome of the Third Plenum, a twice-a-decade conclave of Communist Party officials held last week, underwhelmed investors, with few steps to boost metals demand or fix the property crisis. - COMMODITIES (BBG): Copper Falls to Lowest Since Early April on China Pessimism

Copper fell to lowest level in almost four months on concern that Chinese demand for industrial metals is weakening. A twice-a-decade conclave of China’s top leadership held last week has so far failed to deliver any meaningful stimulus.

US TSYS: Support From Softer Industrial Prices - 2Y Supply, Earnings and Home Sales Ahead

Jul-23 10:48

- MNI (London) - Treasuries have seen some support overnight from a softer global growth outlook with industrial commodity prices including iron ore and copper falling further after what’s perceived by some as a lack of major new stimulus from the China Communist Party’s Third Plenum (for example, here).

- Moves are relatively limited though and leave benchmark tenors across the curve firmly within yesterday’s range after a flow-driven sell-off on a lighter session for headlines.

- Cash yields are 1.5-2.5bp lower with the front end lagging, but with curves also within ranges including 2s10s at -27.3bps (-0.3bps).

- TYU4 at 110-28+ (+ 05+) is close to session highs on somewhat subdued cumulative volumes of 260k.

- Yesterday’s low of 110-18+ cleared support at 110-21+ (20-day EMA) to open 110-07+ (50-day EMA). The latest pullback tests a bullish backdrop which includes resistance at 111-13+ (Jul 16 high).

- Today sees data focus on existing home sales before 2Y supply is possibly of more note. Last month’s 2Y auction came in almost in-line but with the bid-to-cover of 2.75x the highest since Aug 2023.

- A heavy docket for earnings is also in focus, with some large names including Alphabet, Tesla and Visa.

- Data: Philly Fed non-mfg Jul (0830ET), Existing home sales Jun (1000ET), Richmond Fed mfg Jul (1000ET)

- Note/bond issuance: US Tsy $69B 2Y Note auction -91282CLB5 (1300ET)

- Bill issuance: US Tsy $70B 42D CMB Auction (1130ET)

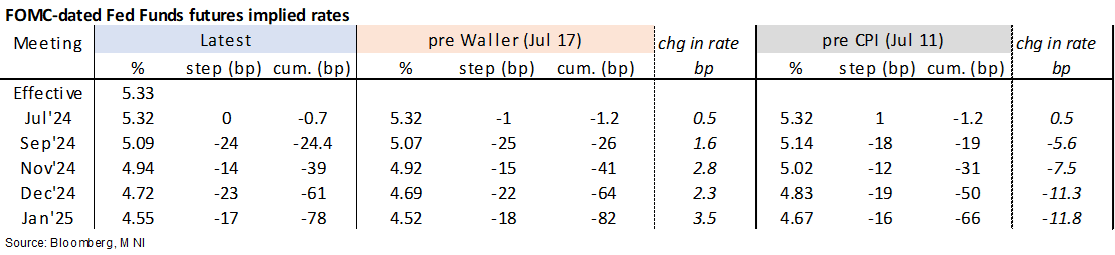

STIR: Fed Rates Hold Yesterday’s Climb, Awaiting Stronger Trigger Late In The Week

Jul-23 10:29

- Fed Funds implied rates hold yesterday’s second half climb that came about with little new drivers, showing little impact from further declines in industrial commodity prices overnight.

- It leaves implied rates close to highs seen since surprisingly soft US CPI on Jul 11, although still fully prices three cuts with the January meeting.

- Cumulative cuts from 5.33% effective: 0.5bp Jul, 24.5bp Sep, 39bp Nov, 61bp Dec and 78bp Jan.

- A reminder that the FOMC is in media blackout for the Jul 31 decision whilst today sees a pick-up in data with existing home sales and some regional Fed manufacturing surveys but with greater data focus on GDP and PCE data on Thu/Fri.