SOFR OPTIONS: Call Fly buyer

SFRV6 96.06/96.18/96.31c fly, bought for 1.25 in 3k....

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BOC: Instant Answers For Today's BOC Decision

Following are the expected Instant Answers for the Bank of Canada decision due at 945am EST:

- Overnight Rate Target (level in x.xx%):

- Does the Bank signal it is prepared to lower rates in the future?

- Does the Bank signal it is prepared to raise interest rates in the future?

- Does the Bank say it will not allow higher energy prices to become persistent inflation?

- Does the Bank say it will look though some of the short-term inflation from the Iran war?

JPY: USD/JPY Threatens Break Above 160.00

USD demand and the latest uptick in U.S. yields takes USD/JPY to 160.00, with immediate resistance located at the April 7 high (160.03), followed by the March 30 top & bull trigger (160.46).

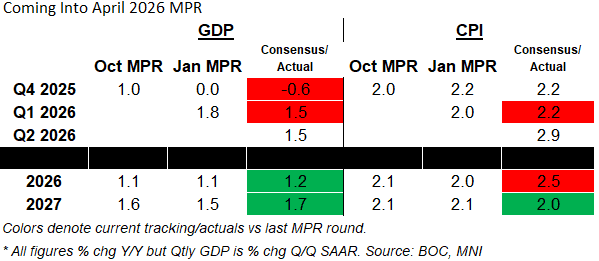

BOC: Monetary Policy Report: Definitely Higher CPI; Neutral Rates Eyed Too

While the BOC is likely to caution today that it’s still too early to assess the impact of the Iran war on the Canadian economy, updates to the quarterly Monetary Policy Report are set to show higher headline CPI forecasts for 2026 compared with the April edition. That’s largely going to be due to a jump in energy prices on the back of the Iran war; consensus shows an expected 2.5% annual CPI reading including a strong pickup to 2.9% by Q2 2026 for this year, though currently consensus is for that to be only “transitory” with a pullback to below BOC forecasts in 2027 (2.0%) and we should note that core measures look to be more tame. See accompanying table.

- On the growth side, it’s more ambiguous. Q4 came in well below January MPR estimates (-0.6% vs 0.0%) and Q1 GDP looks to undershoot 1.8%, but consensus for annual GDP for 2026 and 2027 look a little higher than the last MPR’s projections. This may be attributed to a possible upside impulse to the energy sector boosting growth, and/or the latest Business Outlook Survey suggesting firms expect stronger sales and increased capital spending (apparently shrugging off recent geopolitical uncertainty) but either way analysts are somewhat mixed on whether GDP estimates will be boosted or lowered in this round.

- We will also get the BOC’s updated estimates of potential GDP growth and neutral policy rates. On the latter, it’s widely expected that the estimate of neutral will stay at around 2.25–3.25%. There are structural headwinds to growth that are becoming increasingly apparent, including weaker population/labour force growth and trade frictions, but it may be premature to make a major reassessment.

- Lowering the neutral rate estimate would imply that current rates are less accommodative all else being equal, though we do not expect this to change this year. But if anything, slowing population growth and weak investment given trade shifts could mean lower potential growth and neutral rates. This could have dovish implications as rates at 2.25% would presumably be less on the accommodative side of neutral than previously thought. By the same token, if the BOC produces higher near-term growth estimates alongside the same/lower potential growth, it could suggest less slack and thus more reason to tighten.