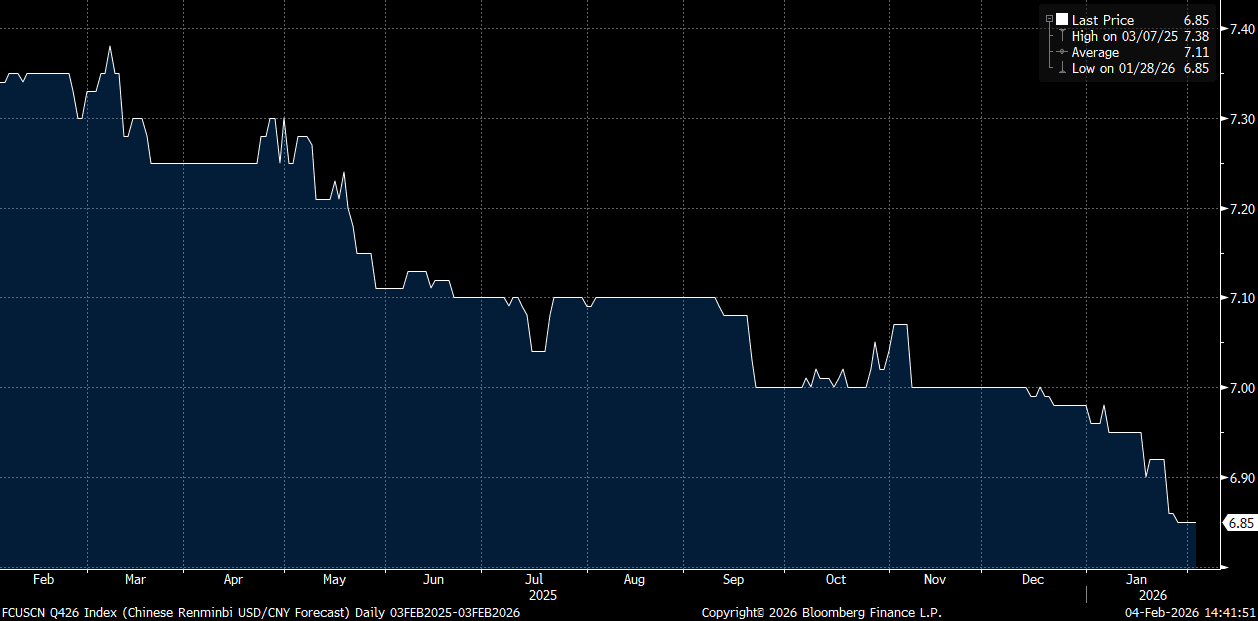

CNY: Bullish Consensus On Yuan Outlook Continues To Rise

USD/CNH couldn't build on fresh downside after the earlier test under 6.9300. We sit back near 6.9350 in latest dealings, little changed for the session. USD indices are little changed, but USD/JPY is pushing high, last near 156.30. CNH/JPY is now close to 22.54, continuing to rebound from the late Jan plunge (highs on Jan 23 of 22.8737). Broader sell-side momentum for the yuan outlook remains positive. The chart below plots the BBG consensus for USD/CNY by end 2026. The bias has been skewed lower, particularly since the start of the year (now at 6.8500).

- Via BBG: "Bank of America Corp. boosted its forecast for the yuan, with the onshore yuan likely to end the third quarter at 6.7 per dollar." Adding: "“Recent yuan appreciation momentum — backed by robust exports and firmer policy signals — leads us to revise the forecasts,” Piron wrote. “The yuan’s strength is spilling into broader emerging-market FX gains.”

- 6.70 by end Q4 is the low end of the BBG range, with 7.10 the high point. The USD/CNH 9 month forward outright sits near 6.8300 in latest dealings, while the 12 month is just under 6.8000. Hence forwards are pricing in this outlook to some degree. Still, the extent of the downside move in consensus forecasts since the start of the year, from near 7.00 to 6.85, is likely to leaving the market looking for further spot USD/CNH downside.

- A fresh break under 6.9300 should see the 6.9000 region targeted. Focus post the Lunar new year break (mid Feb) will be on policy comfort around a stronger yuan, along with export growth and conversion trends.

Fig 1: Trend For Consensus 2026 Year End USD/CNY Forecast

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

PRECIOUS METALS: Venezuela Drives Safe Haven Flows Into Gold & Silver

The US ousting of Venezuelan dictator Maduro on the weekend has added to geopolitical uncertainty as it is unclear if the US will intervene in other countries, especially in South America, and what the outcome of current unrest in Iran could be. This appears to have driven an increase in safe haven flows in Monday’s APAC trading boosting precious metal prices. They have stabilised though in line with a stronger US dollar (BBDXY +0.3%).

- Gold is up 1.7% to $4405.7/oz after an intraday high of $4420.99. Silver is 3.6% higher at $75.44 after reaching $76.344.

- Currently Venezuela is being run by Rodriguez, a Maduro ally, and she has said that the country is ready to cooperate with the US. President Trump warned her against being obstructive and said that the US needs full access to Venezuela’s oil. Secretary of State Rubio said that it will take time to hold elections and that the US doesn’t have troops on the ground.

- Risks at this stage don’t appear to stem from Venezuela itself but what type of precedent the US action has set.

- Equities are generally stronger with the S&P e-mini up 0.1% and CSI 300 +1.6% but Hang Seng down 0.1%. Oil prices are lower with WTI -0.4% to $57.08/bbl. Copper is 2.9% higher.

- Later US December manufacturing ISM and UK November lending data are released.

AUSSIE BONDS: Modestly Richer On A Relatively Subdued Data-Light Session

ACGBs (YM +4.0 & XM +2.5) are modestly stronger after a relatively subdued data-light session.

- The focus of this week will be Wednesday’s November CPI, which is the new complete monthly series. The new trimmed mean CPI appears less volatile than the incomplete series but printed 0.7pp higher at 2.8% y/y in June 2025, which was the recent trough. Q2 was at 2.7% y/y overall.

- Bloomberg consensus is forecasting trimmed mean to be stable at 3.3% in November, which would be at or above the top of the RBA’s 2-3% band for the fifth consecutive month. Headline is expected to moderate 0.2pp to 3.6% but this series continues to be distorted by previous government electricity rebates.

- Cash US tsys are slightly richer in today's Asia-Pac session after Friday's modest bear-steepener.

- Cash ACGBs are 2-4bps richer, with a steeper curve and the AU-US 10-year yield differential at +64bps.

- The bills strip is stronger, with pricing +2 to +4 across contracts.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 35% for February to 98% by June and 171% by December 2026.

- Tomorrow, the local calendar will see S&P Global PMIs: Composite & Services.

Bloomberg Finance LP

OIL: Venezuelan Oil Unlikely To Have Material Impact On Global Market

Venezuela is not a major player in the oil market despite having the largest known reserves, as years of sanctions and dictatorship have resulted in its crude production trending lower. The industry has been neglected and significant private investment will be needed to increase output as well as the lifting of sanctions. Low oil prices could discourage the needed capex. President Trump has said that the US needs full access to Venezuelan oil to rebuild the country.

- In the 1990s, Venezuela produced over 3mbd and OPEC reported that recently it was 1mbd which is above its 2020 trough. According to the IEA it was the 17th largest oil exporter globally and second in South America in 2023 as sanctions and a related-lack of investment in the sector drove output down 73% since 2000.

- Venezuela sells at a discount to benchmarks and most of its oil exports go to China.

- Even if it can return to producing 3mbd, Venezuela would still only be the 10th largest oil exporter and 15th largest producer, assuming other countries are unchanged.