USDCAD TECHS: Bull Cycle Hindered

- RES 4: 1.4111 High Apr 10

- RES 3: 1.4019 38.2% retracement of the Feb 3 - Jun 16 bear leg

- RES 2: 1.3968 High May 20

- RES 1: 1.3925 High Aug 22

- PRICE: 1.3840 @ 16:55 BST Aug 22

- SUP 1: 1.3794 20-day EMA

- SUP 2: 1.3769/22 50-day EMA / Low Aug 22

- SUP 3: 1.3576 Low Jul 23

- SUP 4: 1.3557/40 Low Jul 3 / Low Jun 16 and the bear trigger

Gains this week in USDCAD and the breach of resistance at 1.3879, the Aug 1 high, marked a positive development, however the slippage into the Friday close undermines this sentiment - for now. Moving average studies have crossed and are in a bull-mode position, reinforcing current conditions. An extension higher would signal scope for a climb towards 1.4019, a Fibonacci retracement. On the downside, support to watch lies at 1.3769, the 50-day EMA - a level not yet challenged by the correction lower.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: Inter-Meeting FedSpeak: Uncertainty Equals Patience For Most (2/2)

While a majority of participants appear open-minded to the argument that tariff inflation will prove transitory and that the labor market is “on the edge” (in Waller’s words), almost all participants require more certainty in the data and broader developments before supporting a cut.

- “Uncertainty” was cited by many as a key reason to maintain a patient stance. For example, SF’s Daly is concerned that the Fed could fall behind the easing curve but still only eyes two cuts this year, and not before the fall.

- The most hawkish Board member – Gov Kugler (who is very likely to be replaced in January at the end of her term) – saw the June inflation reports pointing to tariff pressures beginning to show up in prices. Another 2025 voter, St Louis’s Musalem, saw the possibility it could be several months if not quarters before tariffs’ full impact would be felt.

- We haven't heard any other FOMC participants say they were seriously considering supporting a cut at the next meeting, with various members that see two cuts this year eyeing a later restart to easing (Daly / Kashkari specifically mentioned the fall/September respectively).

- In other communications, the latest Beige Book suggested that regional business contacts saw the biggest price increases from inflation are yet to come.

- The June meeting minutes noted "several participants commented that the current target range for the federal funds rate may not be far above its neutral level", pointing to an increasing number of participants that suspect the terminal rate may be higher than previously expected.

US TSYS: Trade Sentiment, Strong Earnings Add to Risk-On Tone

- Treasuries look to finish near session lows Wednesday, improved sentiment tied to trade and better than expected equity earnings added to the risk-on tone after Pres Trump announced deal with Japan late Tuesday.

- Financial Times article posited US/EU were closing in on a 15% deal added to the positive sentiment - despite WH advisor Navarro saying to take the FT story "with a grain of salt".

- Existing home sales fell more than expected in June, to 3.93M (seasonally-adjusted annualized rate), vs 4.00M expected and 4.04M in May (upwardly revised by 10k). That's a 9-month low, breaking an 8-month streak of sales above 4 million.

- MBA composite mortgage applications inched up 0.8% (sa) last week, essentially flat after -10% and +9.4% in the previous two weeks. New purchase applications outperformed after some rare trend underperformance since June, rising 3.4% after -11.8% compared to -2.6% after -7.4% for refis.

- Stocks surged (new record high for SPX eminis at 6393.75), US$ retreated back to early July levels (BBDXY -2.74 at 1193.06).

- Focus turns to Thursday's data: weekly claims, S&P Global US Mfg/Services PMIs and New Home Sales.

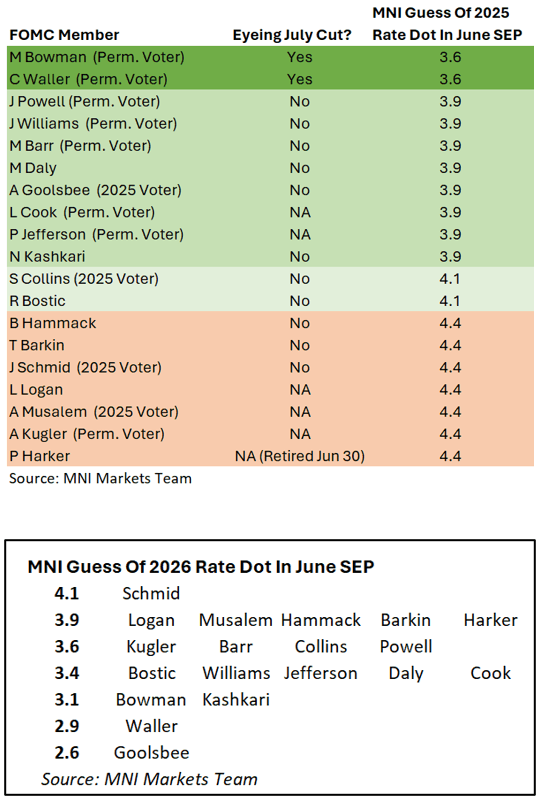

FED: Inter-Meeting FedSpeak: Cautious On Inflation, With 2 Key Exceptions (1/2)

Fed communications since the June FOMC meeting have been largely cautious on the inflation outlook, with little enthusiasm to resume easing until at least September if not beyond given prevailing uncertainty. We go into detail in our Inter-Meeting Fed Communications analysis - Download Full Report Here

- While this patient sentiment was reflective of the June meeting’s Dot Plot showing a split between participants eyeing either zero or two cuts by year-end, the limited incoming data since then doesn’t seem to have swayed views.

- The most notable development has been a newly-vocal minority of two on the 12-member FOMC who appear ready to argue for cuts to resume in July.

- Chair Powell largely took a July cut off the table from the outset, saying at the June FOMC meeting "it takes some time" for tariffs to be seen in prices he said then; "we feel like we're going to learn a great deal more over the summer on tariffs". He caused a minor stir on July 1 when he didn't refute the possibility of a rate cut at the July meeting: "Yeah, I really can't say - it's going to depend on the data. And we are going meeting by meeting. I mentioned, you know, how I'm thinking about that, but I wouldn't take any meeting off the table or put it directly on the table, it's going to depend on how the data evolve.

- To be sure, there are likely dissenters to a hold in July. Only two FOMC members have said that they would/could support a July rate cut, but both are permanent voters on the Board: Vice Chair Bowman ("I would support lowering the policy rate as soon as our next meeting ") Gov Waller (who delivered a July 17 speech titled "The Case for Cutting Now”).

- We could easily see two dissents to a likely July rate hold, and Bowman and Waller are likely the 3-2025 cut Dots in the June SEP.

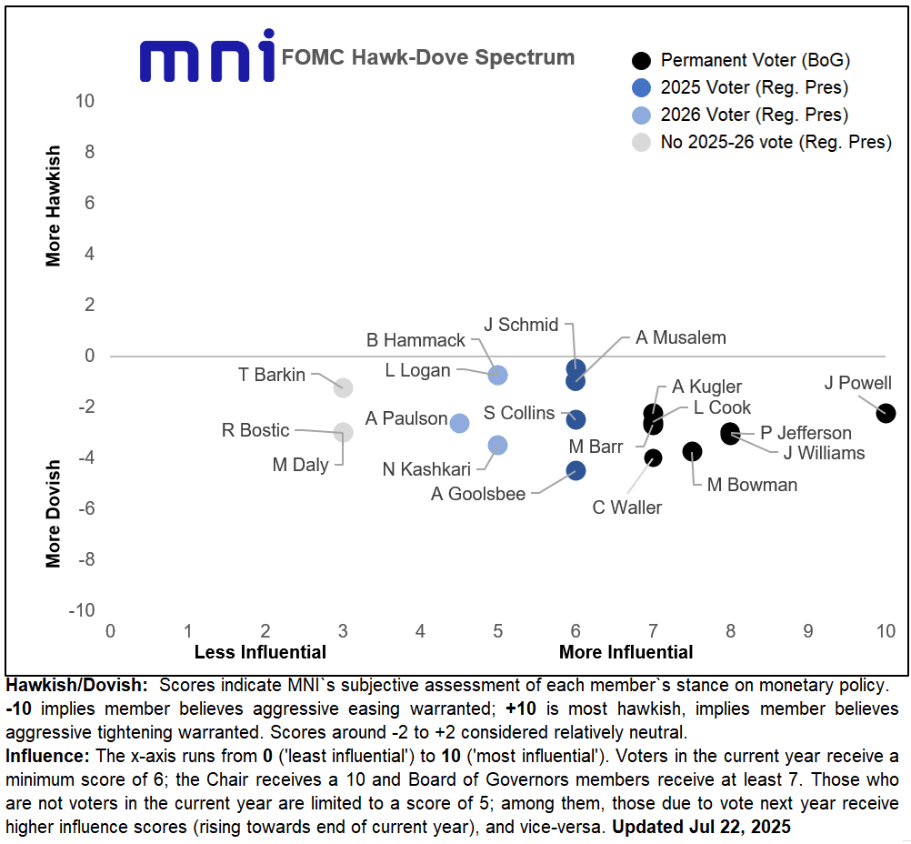

- Our FOMC Hawk-Dove Spectrum has shifted since pre-June FOMC to reflect some of the latest commentary on future easing.

T

T