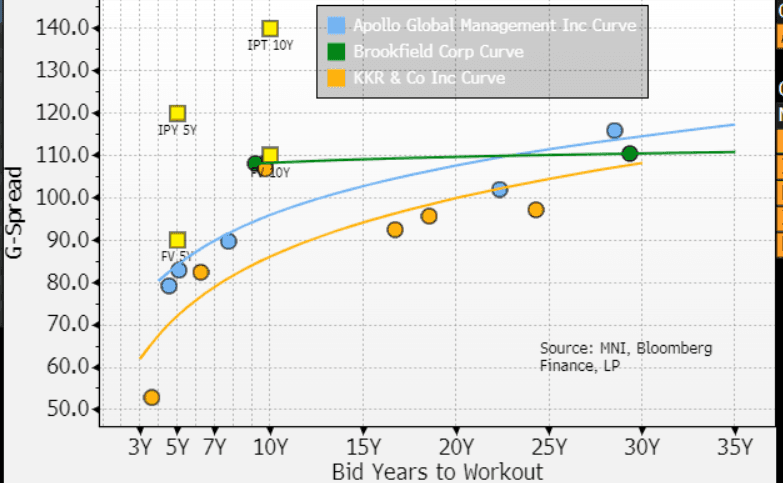

US CREDIT SUPPLY: BROOKFIELD ASSET MGMT (BAMCN) BCHMRK 5Y, LONG 10Y - Fair Value

NEW DEAL: BROOKFIELD ASSET MANAGEMENT LTD BENCHMARK 5Y, LONG 10Y - Fair Value

(BAMCN;NR/A-/A)

• USD 5Y Fixed (Nov. 15, 2030) IPT +120 Area - FV +90a

• USD Long 10Y Fixed (Jan. 15, 2036) IPT +140 Area - FV +110a

- We use KKR and APO has asset mgmt comps to BAM. Both are slightly higher rated. BAMCN should trade slightly wide to these two peers and this is reflected in our FVs. Our 10Y FV of +110a is just slightly wider than BAMCN's existing 5.795 4/24/35s.

• Issuer: Brookfield Asset Management Ltd (BAMCN)

• Format: SEC registered, senior unsecured

• Bookrunners: Citi, WFS

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY OPTIONS: BLOCK: Dec'25 2Y Put Condor

- 2,000 TUZ5 103.87/104.12/104.25/104.37 broken put condors, 0.5 net at 1048:37ET

ENERGY SECURITY: Oil Market Complacent on Geopol Risks in 2026: Trading Houses

Trading houses have warned that the oil market may be overly complacent towards geopolitical risk to oil supply in 2026.

- Speaking on a panel at the Energy Intelligence Forum, Torbjorn Tornqvist, CEO at Gunvor said there was possibly a bit of complacency on the geopolitical risk side for oil, with crude no longer carrying a significant geopolitical risk premium.

- Likewise, Trafigura’s Global Head of the Oil Ben Lobuck commented that the current decline of Brent prices to around $62/b is a result of the geopolitical concerns abating, with prices likely to go even lower.

- However, the risk of future spikes driven by supply security remains with Vitol’s CEO Russel Hardy commenting that the market is likely overly discounting chance of supply side events for next year.

- According to Hardy, the market now sees itself as better placed to weather the storm of any political shocks, having shrugged of a range of security issues in Q2.

- A lack of long-term disruption during earlier flare ups means that the market now sees little risk to Iranian output, and while Ukraine’s drone attacks are getting more precise, they are hitting Russian domestic supply rather than crude, Gunvor’s Tornqvist noted

- While current sentiment may be eschewing concerns for geopolitical related supply disruption. The Vitol CEO noted that key flashpoints represent significant production centres.

- “Whether it’s Iran, Russia, or Venezuela, they are big producers,” Hardy warned. Disruption to output in just one of these risk zones could see prices rise above those currently forecasted.

- “When a market gets wrong footed, that’s when it [oil market] gets punished price wise,” Gunvor’s Tornqvist cautioned

EGBS: Markets Optimistic Lecornu Will Survive, OAT/Bund Below 80bps

The 10-year OAT/Bund spread has tightened further since French PM Lecornu’s address concluded, now 4.5bps narrower on the session at ~78.5bps (the tightest since mid-September). Markets are cautiously optimistic that Lecornu’s Government will not fall to a censure vote after temporarily suspending pension reform until the end of 2027 (alongside abandoning the use of Article 49.3 to pass a budget).

- See our Political Risk team’s latest post above for more colour on what to watch from the Socialists.

- Zooming out, the OAT/Bund spread remains above the year-to-date average of ~73bps. Suspension of pension reform necessarily implies less fiscal consolidation.

- While Lecornu aims to bring the deficit below 5% GDP in 2026, the independent budget watchdog has also noted that the government’s growth forecasts and intended polices may be too optimistic.

- Breaking down the OAT/Bund spread into respective French and German swap spreads, today’s narrowing has clearly been driven by the OAT leg. The 10-year OAT swap spread is above -80bps for the first time since early September.

- It’s notable that throughout September, widening in the 10-year OAT/Bund spread was mostly driven by Bund outperformance versus swaps, with the OAT swap spread relatively steady around -85bps during this period.

- It highlights that markets have not been expressing French political/fiscal uncertainty solely via domestic bond markets (i.e. OAT swap spread narrowers), but also via the Bund (i.e. safe haven) leg.

Figure 1: 10-year OAT/Bund Spread Expressed As Swap Spread Differentials (Source: Bloomberg Finance L.P)