EURUSD TECHS: Bounce Erased, Confirmed as Corrective

* RES 4: 1.1835 High Feb 23 * RES 3: 1.1736 50-day EMA * RES 2: 1.1704 20-day EMA * RES 1: 1.1667 Hi...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURUSD TECHS: Impulsive Rally

- RES 4: 1.2081 High Jan 27 and key resistance

- RES 3: 1.2045 High Jan 28

- RES 2: 1.1975 High Jan 30

- RES 1: 1.1929 High Feb 10

- PRICE: 1.1900 @ 15:40 GMT Feb 10

- SUP 1: 1.1766 Low Feb 06

- SUP 2: 1.1749 50-day EMA

- SUP 3: 1.1693 76.4% retracement of the Jan 19 -0 27 bull leg

- SUP 4: 1.1670 Low Jan 22

Monday’s price action provides good evidence that the bearish correction in EURUSD has concluded, with the impulsive rally through 1.1900 marking a ~150 pip rally off Friday’s lows. This shifts focus to the scale of the recovery, with 1.1975 the next notable resistance into 1.20 and the cycle highs of 1.2081. Support to watch remains at the 50-day EMA, at 1.1749. A clear breach of this 50-day average would suggest scope for a deeper pullback.

BONDS: EGBs-GILTS CASH CLOSE: Gilts Strengthen, But Continue To Lag Peers

Gilts once again underperformed Bunds, within a broad curve flattening move across European FI Tuesday.

- Long-end Gilts continued their recovery following vocal support in Monday's session by government ministers for PM Starmer, thereby alleviating near-term fiscal concerns.

- Despite being apparently weighed down by heavy sovereign and corporate supply, Bunds continued to track global peers and outperformed Gilts.

- Indeed, EGBs and Gilts tracked a Treasury rally in afternoon trade, with US data including retail sales and labour costs coming in softer-than-expected.

- On the day, the German curve bull flattened, with the UK's twist flattening.

- Periphery/semi-core EGB spreads were little changed.

- Wednesday's global focus will be the US employment report, though we also get the ECB's latest wage tracker and plenty of sovereign supply including a French syndication.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.9bps at 2.069%, 5-Yr is down 2.3bps at 2.383%, 10-Yr is down 3.2bps at 2.808%, and 30-Yr is down 3.7bps at 3.49%.

- UK: The 2-Yr yield is up 1.7bps at 3.643%, 5-Yr is down 0.6bps at 3.894%, 10-Yr is down 2.1bps at 4.506%, and 30-Yr is down 2.1bps at 5.325%.

- Italian BTP spread down 0.6bps at 60.5bps / French OAT down 0.8bps at 59.8bps

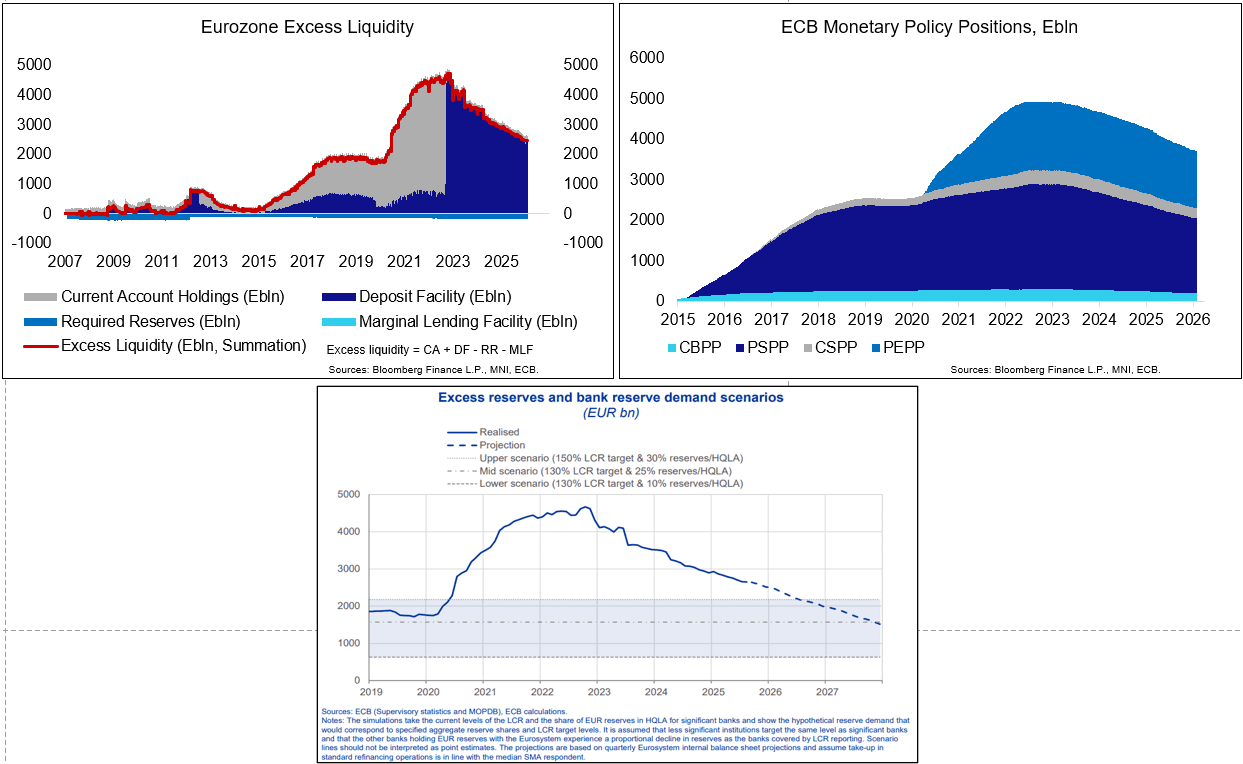

ECB: Balance Sheet Suggests Little Need For Liquidity Action in Eurozone

ECB balance sheet data confirms that excess reserves remain well above levels approaching scarcity across the Eurozone, leaving little pressure for the bank to act on the structural bond portfolio for now. In the near term, this puts the focus on the setup of a new repo facility which appears more targeted towards fostering the international role of the euro than impacting Eurozone money markets.

- Moves in excess liquidity can be bumpy in the short term but a downtrend remains intact, driven by the passive run-off of the ECB balance sheet. A noteworthy move at the turn of the year were higher "net autonomous factors" which contribute negatively to the liquidity calculation. Multiple positions moved at that time with revaluation accounts standing out with a E144bln jump; these are "unrealised gains on gold, FX, and securities [...] shown on the liabilities side of balance sheet."

- Eurozone excess liquidity decreased by roughly €34bln/month on average in 2025, bringing the measure to around €2.435trl, down by 49% from the series' high of €4.748trl in November 2022.

- The long-term liquidity decline since the peak was initially driven by a roll-off of the ECB's TLTROs (with the TLTRO III programme starting in 2019 with three-year maturities and with the final maturity in Dec 2024) but mostly comes on the back of the declining ECB's monetary policy positions (PEPP + APP), which are standing at a current €3.718trl combined.

When liquidity ultimately becomes "scarce" (or close to it) that will show in money market tensions and increased takeup in the ECB's standard refinancing operations, neither of which are striking at this stage.

- MRO take-up did reach E25bln on December 22 (tick-ups are usual towards year-end), indeed the largest allotment since 2017 but still very low by historical standards. Meanwhile, recent pressure in EUR repo markets hasn’t been viewed as concerning.

- This is contrary to the Fed & BoE which both have provided fresh liquidity support/increased focus on bank liquidity provisions in H2'25, after bank reserves in their respective jurisdictions moved towards / reached a less abundant state. Latest ECB projections see excess reserves hitting bank demand in mid-2026 in an "upper scenario" but not until late 2027 in a "mid scenario".

Recapping, last week's ECB press conference was followed by a Reuters report that the ECB "is working on opening up its liquidity facility to more countries, making it cheaper and easier to access in a bid to foster the international role of the euro [...] The move, the details of which are still being worked out and will likely be announced around the Munich Security Conference next week, will create standardised rules for gaining access to the ECB's repurchase agreements, the sources said". This came after President Lagarde mentioned a new framework around the ECB's repo lines being in the pipeline:

- "One of the attributes of a strong currency is to be the provider of liquidity. And while we are tied to the monetary purpose of what we do in terms of liquidity and we have to constantly assess the proportionality of what we do, it is a fact that we are looking at our liquidity framework and that the repo lines – to be distinguished from the swap lines – are in progress in terms of reframing them, opening up the access and making them more attractive to other national central banks outside the euro area and outside Europe. So this is in the works, and I hope to be able to announce a bit more in a few days."