EU CONSUMER CYCLICALS: Booking.com: 3Q results

(BKNG; A3/A-/NR)

Strong 3Q numbers and positive comments on current trading.

On AI, management continues to frame it as a tailwind, pointing to growth in connected bookings (cross-vertical flight + hotel), lower cancellations from more personalised matching, and reduced service costs (more bots). The key concern is if hotels will go to AI engines directly, bypassing Booking.com. Management's rebuttal is simple; providers already can - and do - do that with Google. It argues the payments and regulatory framework make end-to-end travel transactions complex, adding “if it were easy, Google would have taken this thing over a long time ago.” It also notes its loyalty programme (50% of bookings linked to one) and associated proprietary customer data. It hasn't been slow in integrating either: it was an early participant in 'apps in ChatGPT' that allows gpt users to query the site directly.

Equities are not concerned - Booking is the largest travel stock and trades on a 29x trailing P/E. We have no firm view on longer term prospects.

- Gross bookings $49.7b, +14% y/y, made up of:

- Room nights 323m (+8% y/y; Europe +HSD, US +HSD, Asia +LDD, RoW +LDD)

- Avg. Daily rates +1%

- Flight bookings +32%

- FX tailwind +4%

- 3Q revenue $9.0b, +12% y/y (+8% ex. FX)

- adj. EBITDA $4.2b, +15% y/y

- FCF $1.4b on WC changes. YTD at $7.7b, +6% y/y

- $16.5b of cash on hand vs. $17b of gross debt

- Alternative accommodation (competes with Airbnb): room nights +10% y/y; now 36% of total.

- Mobile app: ~mid-50% of total bookings (LTM).

- Direct channel: mid-60% of consumers come directly to Booking.com.

- Loyalty programme (Genius): mid-50% of room nights booked (LTM).

4Q Guidance:

- Gross bookings +11-13% with room nights +4-6%

- Revenue +10-12%

- adj. EBITDA +8-14%

leaving FY25 guidance at: - Revenue +12%, EBITDA +17-18%

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSY FUTURES: BLOCK: Dec'25 2Y Sale

- -6,000 TUZ5 104-04.38, post time bid at 0837:29ET, DV01 $238,200.

- The 2Y contract trades 104-04.38 last (+.75)

PIPELINE: Corporate Bond Roundup: SocGen, Scotia, Rentenbank on Tap

- Date $MM Issuer (Priced *, Launch #)

- 09/29 $1.4B Codelco WNG 2035 Tap +150a, 2055Tap +180a

- 09/29 $1.4B Waterbridge Starts $400M each 4Y, 8Y

- 09/29 $500M Fortitude Global Funding WNG 3Y +120a

- 09/29 $500M Starwood Property Trust 5.25NC

- 09/29 $Benchmark Societe Generale 11NC10 +160a

- 09/29 $500M Vakifbank WNG PerpNC5.25 8.5%a

- 09/29 $Benchmark Corebridge Funding 5Y +95a

- 09/29 $Benchmark Dominion Energy 2056 Taps

- 09/29 $Benchmark Scotiabank 60NC10 7.25%a

- 09/29 $Benchmark Rentenbank 5Y SOFR+41a

- 09/29 $Benchmark Kuwait 3Y, 5Y, 10Y investor calls

- 09/29 $Benchmark Egypt 3Y, 7Y Sukuk investor calls

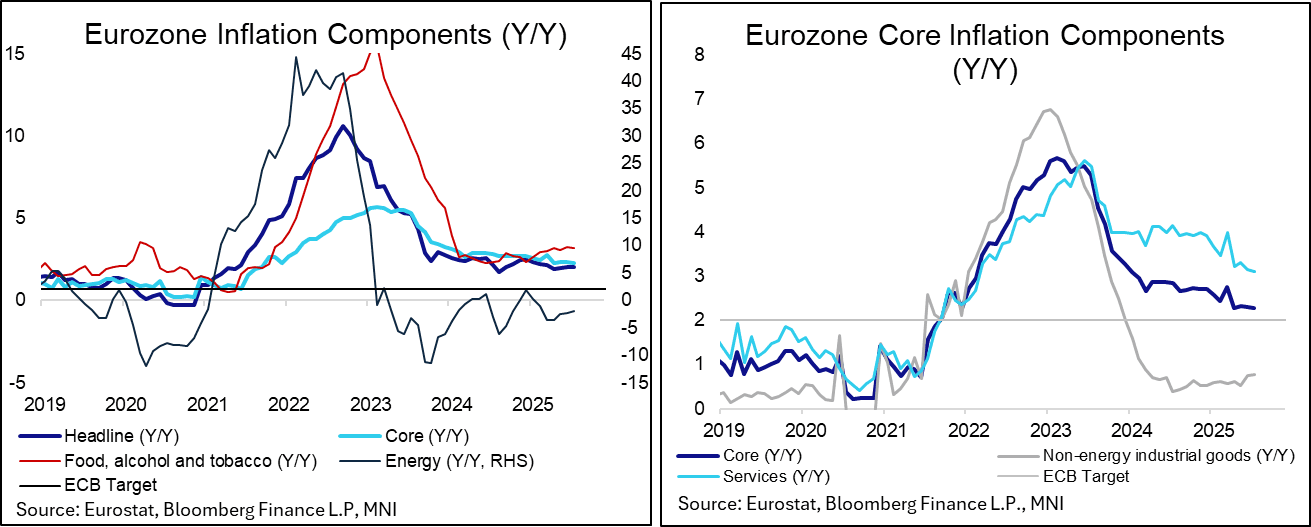

EUROPEAN INFLATION: MNI Eurozone Inflation Preview – September 2025

Energy And Services To Drive Headline Higher

- The Eurozone September flash inflation print is due on Wednesday morning, with data from Germany, France and Italy coming on Tuesday.

- Spain and Belgium released flash data Monday morning. Headline inflation is expected to rise across the four major economies, culminating in a 2.2% Y/Y median for the Eurozone-wide print (vs 2.0% prior). Core inflation is expected to be steady at 2.3% Y/Y.

- Across categories, the main driver in September will be the yearly rate of energy picking up to around –0.4% Y/Y (median of analyst previews MNI has seen) from –2.0% in August on the back of base effects. Meanwhile, the recent downtrend in services inflation is expected to temporarily halt with a small uptick to 3.2% Y/Y (vs 3.1% in August).

Core goods are seen marginally lower than last month at 0.6%-0.7% Y/Y (vs 0.8% prior), albeit with uncertainty around the impact of seasonality and weight changes relative to 2024. Analysts generally expect little change in food, alcohol and tobacco inflation at around 3.2%.