CHINA: Bond Futures Up on Liquidity Injection & PBOC Buying

Nov-20 02:57

- China's bond futures are up this morning following CNY110bn liquidity injection via the OMO and various news articles on PBOC resuming buying of government bonds. Whilst the latter is not new news, several onshore brokers have adjusted their forecast downwards by 10-15bps for the CGB 10-Yr.

- The bond market seems no longer in its sweet spot with issuance to support growth remaining high, asset allocation out of bonds into the AI/Tech led equity rally and a calming of US / China trade relations. This is likely a driver for the resumption of PBOC buying of government bonds though for now, their volumes are expected to be low.

- The PBOC announced this morning that will auction CNY120bn of 1-month MOF deposit on November 24 and CNY80bn of 21-day MOF deposit on November 24.

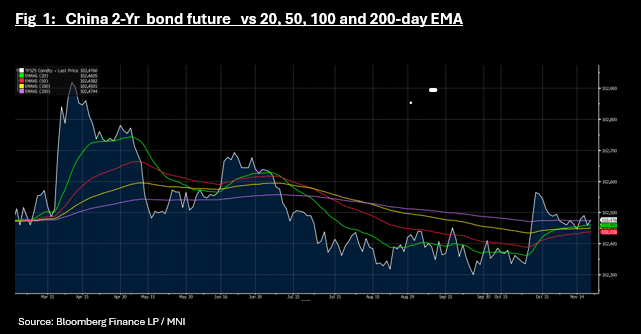

- The 10-Yr bond future is up +0.11 to 108.535, seemingly bouncing off the 20-day EMA of 108.42. It has failed to hold below the 20-day EMA since the end of September.

- The 2-Yr bond future is up +0.02 to 102.47, atop the 200-day EMA of 102.47 which it traded below briefly this week.

- Cash remains quiet with the CGB10-Yr at 1.80 and the CGB 2-Yr at 1.42%

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI EXCLUSIVE: Advisors Share Their Monetary Policy Outlook Ahead Of 5yr Plan

Oct-21 02:51

Advisors share their outlook for monetary policy ahead of China's Five-Year Plan reveal. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

STIR: BoJ Market Pricing: Wait-And-See Approach On Oct 30

Oct-21 02:43

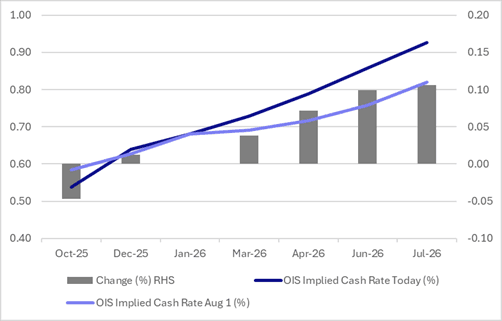

BoJ-dated OIS pricing is little changed across 2025 meetings compared to early August levels. Pricing is, however, firmer for 2026 meetings out to July.

- As far as the October 30 meeting is concerned, markets are positioned for a cautious, wait-and-see approach from the BoJ.

- Current OIS pricing implies just a 24% probability of a 25bp hike in October, rising to 65% by December and 82% by January.

- A full 25bp hike is not fully priced until March 2026.

Figure 1: BoJ-Dated OIS – Today Vs. August 1

Source: Bloomberg Finance LP / MNI

STIR: Market Less Certain Than Normal About Nov 4 Cut By RBA

Oct-21 02:38

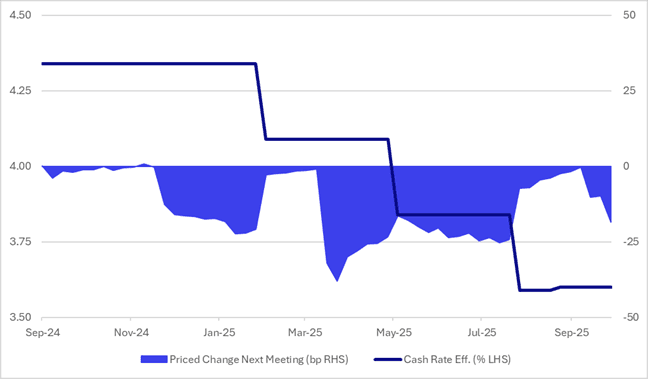

Despite firming slightly in recent days, RBA-dated OIS pricing remains 7–13bps softer across meetings compared with pre-jobs data levels last week.

- A 25bp rate cut in November is now assigned a 68% probability (peak 80%, pre-data 38%), with a cumulative 23bps of easing (peak 25bps, pre-data 13bps) priced by year-end.

- Compared with the lead-up to previous cuts in this easing cycle, the market appears less certain than usual about a November 4 move.

Figure 1: RBA-Dated OIS – Cash Rate Vs. Priced Change Next Meeting

Source: Bloomberg Finance LP / MNI