BONDS: Bond Futures test broader lows

Feb-08 12:16

- New intraday lows across the board in EGBs and US Treasuries, again all gradual moves with lower average volumes.

- Latest flow saw 6k TYH4 sold through that small initial 111.00 level.

- Below that 111.00 level, most will look at 110.22+, Monday's lows, following the 2 points fall, on the back of the NFP beat last Friday.

- But focus in Yield terms is on the 4.20% mark, today equates to ~110.16+.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OUTLOOK: Price Signal Summary - Short-Term Bear Threat In Gilts Remains Present

Jan-09 12:16

- In the FI space, Bund futures maintain a softer short-term tone and the contract is trading closer to its recent lows. Weakness below the 20-day EMA risks a deeper correction, which would open the key support at the Dec 8 low of 134.37. Momentum studies are pointing south, highlighting the short-term bearish threat. On the upside, a resumption of gains would open 138.84, the Dec 27 high and a bull trigger. Initial resistance is 136.24, the 20-day EMA.

- Gilt futures maintain a softer tone and the contract is trading closer to its recent lows. Last week’s move lower resulted in a break of the 20-day EMA, suggesting scope for a continuation of the bear cycle near-term. This has exposed support at 98.97, the Dec 6 high. On the upside, initial firm resistance to watch is at 101.98, the Jan 3 high. A break would ease bearish pressure.

PIPELINE: Monday's $12B Saudi Arabia 3Pt US$ Issuance Largest Since May'23

Jan-09 12:08

Saudi Arabia's $12B 3pt US$ issuance led Monday's supply, the largest issuer since May of 2023 when Pfizer issued $31B over 8 tranches. Incidentally, Saudi Arabia issued $6B Sukuk over two tranches in May'23 as well: $3B 6Y +80, $3B 10Y +100.

- Date $MM Issuer (Priced *, Launch #)

- 1/9 $5B KFW +5Y +42

- 1/9 $Benchmark OKB 5Y

- 1/9 $Benchmark Sumitomo Life PerpNC10

- Expected Wednesday:

- 1/10 $Benchmark Asian Infrastructure Investment Bank 5Y SOFR+56a

- $28.4B Priced Monday

- 1/8 $12B *Saudi Arabia $3.25B 6Y +90, $4B 10Y +110, $4.75B 30Y +170

- 1/8 $3.75B *Mercedes Benz 5pt: $700M 2Y +55, $650M 2Y SOFR+67, $800M 3Y +70, $850M 5Y +90, $750M 10Y +100

- 1/8 $2.55B *BPCE $650M 3Y +108, $1B 6NC5 +175, $900M 11NC10 +250

- 1/8 $2B *ANZ Banking Group $1.2B 3Y +63, $800M 3Y SOFR+81

- 1/8 $2B *Honda 3pt: $850M 2Y +60, $400M 2Y SOFR+71, $750M 10Y +93

- 1/8 $1.5B *SK Hynix $500M 3Y +145, $1B 5Y +167

- 1/8 $1.4B *Southern California Edison $500M 3Y +75, $900M 10Y +120

- 1/8 $700M *RGA Global Funding 7Y +160

- 1/8 $1.25B *Realty Income Group 5Y +95, 10Y +125

- 1/8 $750M *National Grid 10Y +142

- 1/8 $500M *Principle Life 3Y +90

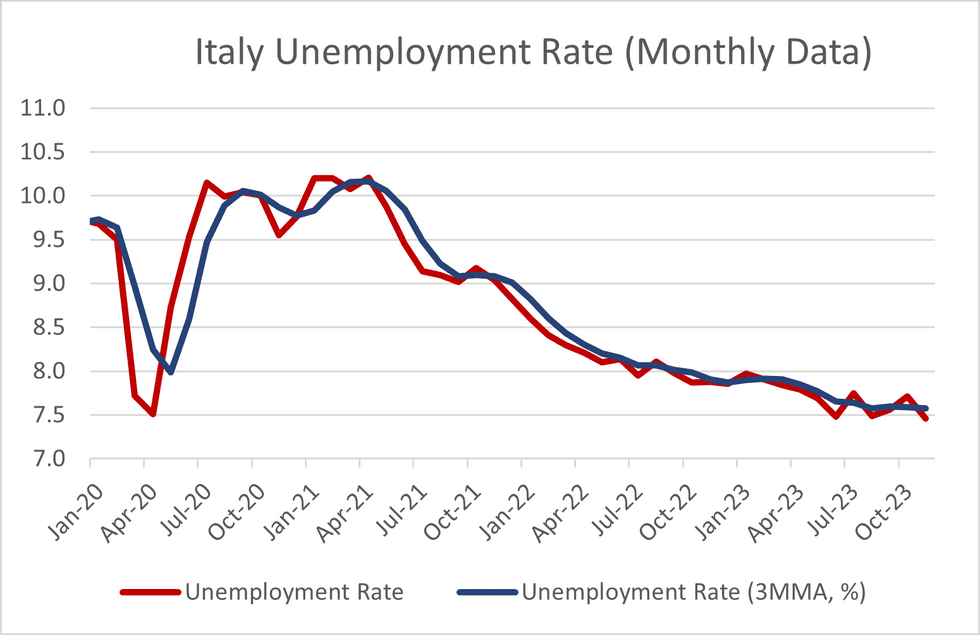

ITALY DATA: Downside Surprise In Unemployment Rate, But Longer-Term Trend Unclear

Jan-09 12:01

The Italian unemployment rate for November surprised to the downside, printing at an unrounded 7.46% (vs 7.8% cons, a downwardly revised 7.71% prior).

- Note that in October, the unemployment rate surprised consensus to the upside (at 7.8% vs a 7.4% expectations at the time), clouding the interpretation of this month's data somewhat.

- A 3M moving average suggests that the unemployment rate continues to be stable around 7.6% (November: 7.58%, October: 7.59%, September 7.60%).

- The fall in the unemployment rate (and number of unemployed persons) was met with a rise in employment, with the 3M/3M SAAR employment growth rate rising to 2.26% (vs 2.05% in October) and the employment rate ticking up a touch to 61.84% (vs 61.79% prior).

- Looking at demographics, the majority of the fall in unemployment and rise in employment was seen amongst women. The rise in employment was driven by those 35 or older, while all groups other than 25-34 year-olds saw a fall in unemployed people.

- Looking to the December data, both the PMIs and the latest EC survey indicated that employment will remain stable/rise slightly. The December Employment Expectations Indicator rose a touch to 104.2 (vs 104.0 prior). However, the 3MMA of this metric has been trending lower for the last 3-months.