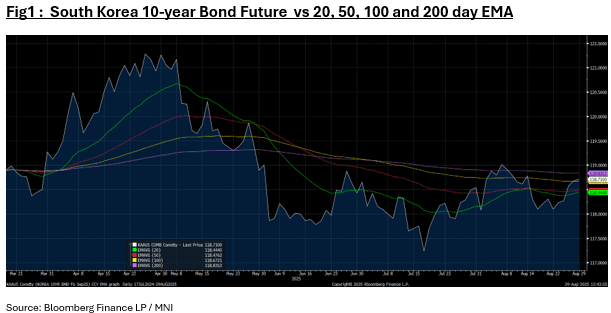

SOUTH KOREA: Bond Future Steady, Higher For Week

- Korea's 10-year bond future has delivered gains for five days straight, and is up again in Friday morning trade.

- Up +0.03 at 118.70, the gains this week has pushed the 10-year above the 100-day EMA of 118.67 and +0.61 for the week.

- The 3-year is lower by -0.03 at 107.35, yet up +0.10 for the week. The losses on Friday see it near the 20-day EMA of 107.34.

- The 10Yr KTB is at 2.83%, -3bp lower for the week.

- Next week is a big week for data with exports, PMI Manufacturing, CPI and 2Q GDP preliminary.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

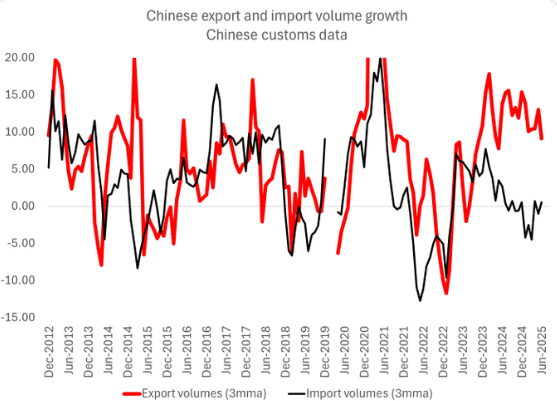

CHINA: Viewpoint On The Surge In China Exports

Lots has been written recently regarding the US-EU trade deal but one point does stand out. The EU chose not to have a trade war with the US as it is currently looking to improve the structure of its trade terms with China. Brad Setser has written a thread on X expanding on China’s Manufacturing Policy and the ramifications thereof:

- “Probably the most important chart for the world economy right now -- Chinese export growth in both q1 and q2 was close to 10%; Chinese import growth has been flat (q2) or negative (q1). With exports 20% of GDP, implies a huge net export contribution …” See Fig.1 below

- “This excellent FT story provides the narrative to go along with the hard data -- China's localities have tremendous incentives to subsidize the production of overcapacity in new and old sectors alike. & with internal demand weak, exports result.” https://www.ft.com/content/f7979a8f-874a-4b47-8304-d93d30171980

- “Combine weak internal demand, a weak CNY & overly enthusiastic support for new sectors inside China & China ends up distorting the entire global economy.”

- “A country (or economic block) that doesn't have an effective industrial policy of its own effectively will end up importing Chinese industrial policy and let China set the structure of big parts of its industry, as Europe is discovering.”

- “Chinese export growth cannot outperform global trade unless another region of the global economy under-performs … Europe clearly has been losing out.”

Fig.1: Chinese Export and Import Volume Growth

Source: MNI/@Brad_Setser

RBA: VIEW: Westpac Expects Cuts At Next Four SoMP Meetings

Q2 trimmed mean inflation printed at 0.6% q/q and 2.7% y/y after 0.7% & 2.9% in Q1. Westpac believes two consecutive prints at seasonally-adjusted 0.6-0.7% q/q show that underlying inflation is within the band and so the RBA can continue easing in August. It believes that will be followed by 25bp cuts in November, February and May – all Statement on Monetary Policy meetings that include updated staff forecasts.

- Westpac notes that Q2 CPI data “removes any awkwardness posed by inflation remaining too high for the RBA’s comfort, at the same time that the labour market might be starting to ease again”.

- “Further softening in the labour market would sit uncomfortably with a decision to hold the cash rate at restrictive levels when underlying inflation is so close to target.”

- “We expect the RBA to cut the cash rate by 25bps at its August meeting to 3.6%. With internal members likely switching their votes from hold to cut, we expect the external members who voted to hold in July will also switch to a vote to cut, leading to a unanimous decision.”

- “Assuming our expectations are borne out, that would take the cash rate to a trough of 2.85%. We think this is at the lower end of what could be regarded as neutral, and would reflect the RBA’s response to a path for underlying inflation that turns out a little lower than what it forecast in May.”

- RBA Deputy Governor Hauser speaks on Thursday and could give more information on “how the RBA staff are seeing the data and whether the ongoing disinflation revealed in today’s data is expected to continue”. “The Governor and Deputy Governor will not give guidance in public appearances between meetings. That would front-run the meeting and pre-empt the MPB’s decision.”

BOJ: MNI BoJ Preview - July 2025: Focus On Presser After Trade Deal

EXECUTIVE SUMMARY

- The two-day Bank of Japan (BoJ) policy meeting concludes on 31 July, with the central bank set to release its quarterly “Outlook for Economic Activity and Prices”, its monetary policy statement, and hold a press conference with Governor Kazuo Ueda.

- The BoJ is widely expected to keep its policy rate unchanged at 0.5% for a fourth consecutive meeting, amid signs of easing trade-related uncertainty since its June meeting.

- Most analysts continue to expect the next rate hike to occur in late 2025 or January 2026. However, timing remains fluid.

- Markets will pay close attention to Governor Ueda’s tone during the post-meeting press conference. Ueda has maintained a cautious stance since May, but if the forecasts and risk assessments are revised higher, there’s a high likelihood his tone may shift.

- However, with OIS markets pricing in a 65% chance of a 25bp rate hike by end-2025, the bar for a hawkish surprise is high. As a result, even a mild shift in tone could be interpreted as dovish, relative to expectations.

- Full preview here