EM LATAM CREDIT: Bolivia: Moody’s Rating Raised – Positive

(BOLIVI;Caa3pos/CCC-neg/CCC+)

Moody’s raised Bolivia’s senior unsecured credit rating to Caa3 with a positive outlook due to a government commitment to pay upcoming debt obligations, increased reserves, a debt exchange with local holders of external debt, multilateral financing support and an improved political environment. We agree the credit profile has improved substantially over the past six months, though we still have two ongoing concerns that need to be monitored, the cost of rising fuel prices as Bolivia is a net oil importer and maintaining popular support amid the impact from policy decisions such as removing fuel subsidies.

• BOLIVI 30s (2.9Y WAL) retreated ¼pt today to $95.90 YTW 9.13% G-Spd 530bp. The bonds are down ½ pt MTD but up 3pt YTD as the market factored in improving credit fundamentals. About 67% of $1.85bn outstanding 2028/30 bonds will be swapped for local debt instruments, reducing tradable float substantially, and the exchange will be conducted with locals only as they are large holders of external debt. That will lower future external debt payment obligations. A combination of future policy reforms, multilateral bank financing and eventual access to the international debt markets could lead to ratings upgrades for Bolivia and improved valuations approaching Ecuador (ECUA;Caa1/B-/B-) levels with ECUA 30s (2.3Y WAL) quoted $98, 7.89% YTW G-Spd 407bp.

• Moody’s cited a political willingness to make debt payments as well as an improvement in ability to pay with a rise in international reserves to $4.4bn in Jan. 2026, from $2.7bn July 2025, which was partly due to rising gold prices but also an increase in FX reserves to $500mn from $67mn. Multilateral loan financing will also be helpful, including $3.1bn from CAF and $4.5bn from the IDB over the next 2-4 years, to enable macroeconomic stabilization and policy reforms.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SECURITY: Oman FM Says "Good Progress" Made In US-Iran Talks

- Albusaidi, "Today’s indirect negotiations between [Iran and US] concluded with good progress towards identifying common goals and relevant technical issues. The spirit of our meetings was constructive. Together we made serious efforts to define a number of guiding principles for a final deal... Much work is yet to be done, and the parties left with clear next steps before the next meeting."

- The statement suggests the two sides may be getting closer to defining the shape of a new nuclear deal, if not the substantive details. As we noted previously, Iran has appeared primarily focused on the parameters of talks. SECURITY: Second Round Of Indirect US-Iran Nuclear Talks Underway In Geneva

- Indeed, Ali Vaez, Director of the Iran Project at the International Crisis Group, notes: "We seem to have moved from Washington and Tehran talking about talks to talking about what talks should address. If that's the case, it would constitute a step forward because of how divergent their positions have been on what an agreement should cover."

- Laurence Norman at WSJ puts a more pessimistic spin on the same post-talks statements: "I think we should be very careful in over-interpreting this. It sounds very much to me as if they have agreed the scope of what needs addressing in a deal. Not what the content of that scope will be."

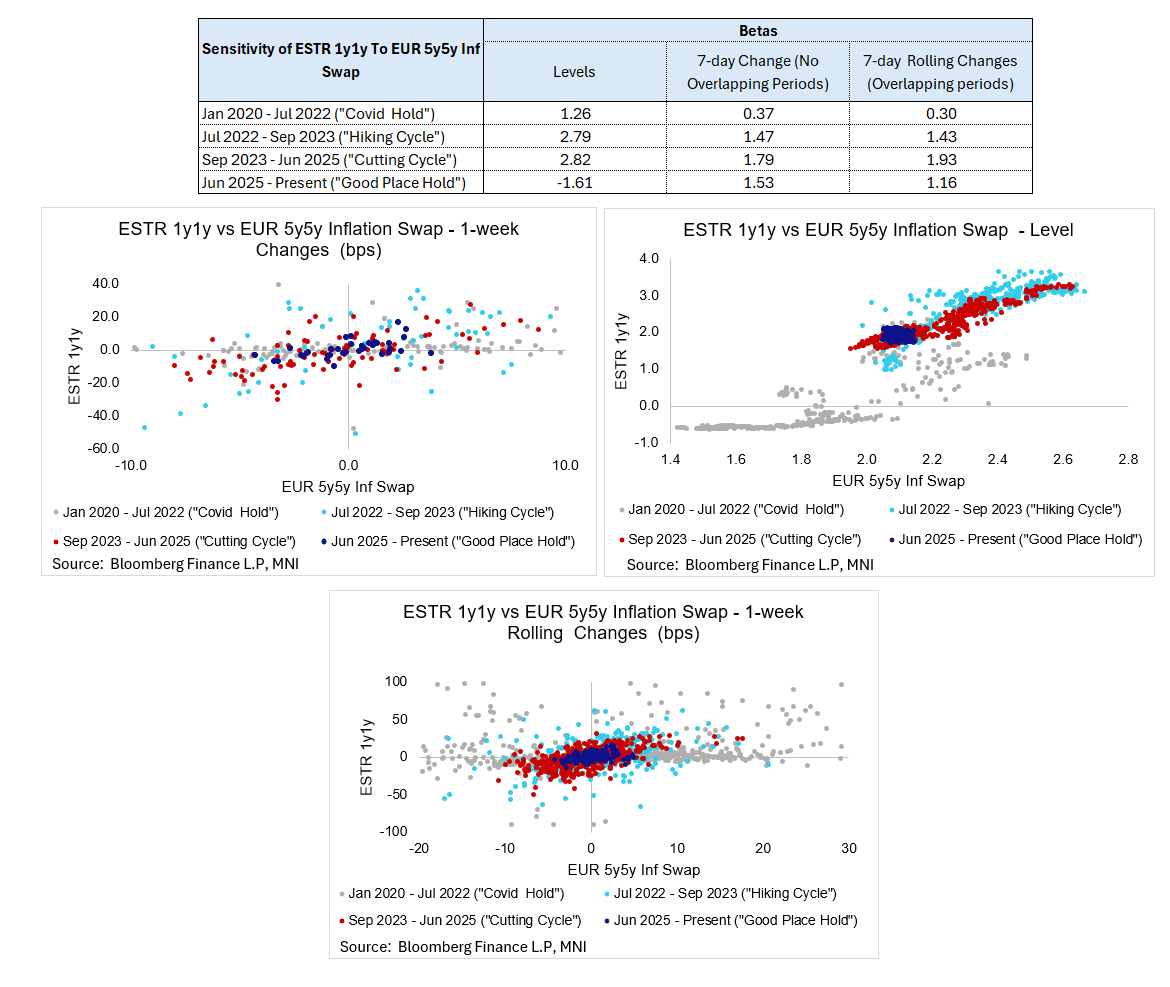

STIR: Sensitivity of ESTR 1y1y To 5y5y Inflation Swap Changes Has Declined

The ECB remains in its well-signalled “good place” on policy rates, and market-implied inflation expectations have been anchored around the 2% inflation target for some time now. That has seen the sensitivity of front-end EUR rates (e.g. ESTR 1y1y) to changes in EUR 5y5y inflation swaps decline considerably relative to the Sep-23 to Jun-25 cutting cycle. Looking ahead, it may require the onset of a fresh policy rate cycle (e.g. in response to a new shock or change in the existing balance of risks) for this sensitivity to increase again.

- The 5y5y EUR inflation swap is currently at 2.0962%, down from a year-to-date closing high of 2.1440 on February 2. Based on daily data since the last ECB cut, this 5y5y level has been associated with a 1.92% ESTR 1y1y rate. ESTR 1y1y is currently at 1.935%.

- ECB officials will have to weigh several "known unknowns" facing the inflation outlook over the coming years. Continued import penetration from China (and related EUR effective exchange rate dynamics) remains a downside risk to goods inflation in the near-term, but the impact of higher tariffs/deglobalisation forces on supply chains may provide some offset further out.

- Domestically, there remains uncertainty around the inflationary impulse from higher German fiscal spending, alongside the broader compensation/productivity outlook.

- A reminder that this week's Eurozone data calendar is headlined by the February flash PMIs and Q4 negotiated wages - both on Friday.

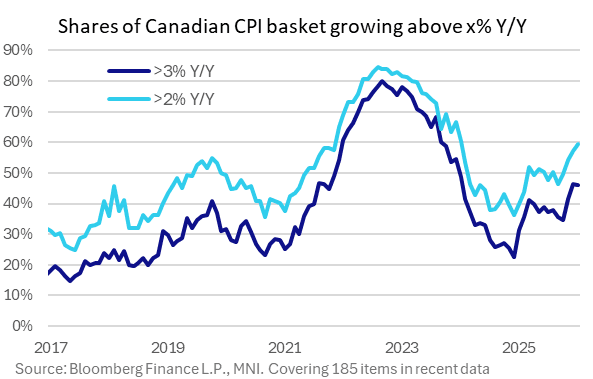

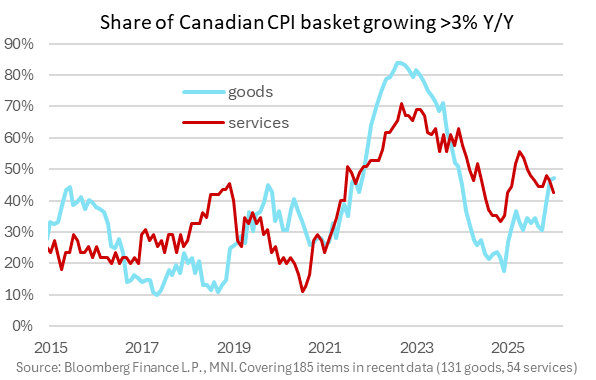

CANADA DATA: Upside Inflation Breadth Starting To Narrow, Goods Remains Elevated

January's CPI report showed a continuation in the divergence of inflation breadth between goods and services categories, even as core/underlying aggregate metrics continued to decelerate. The upside pressure isn't exactly narrow, but the reduction in outlying upside readings should provide some comfort that a broader surge in inflation isn't underway.

- Overall CPI breadth showed close to 60% of all items rising at a higher-than-2% Y/Y clip, after 57% in December and marking a 24-month high. However just 46% was rising faster than 3% (down from 47%) while the share rising at 4+% was steady at 38%. The latter is still elevated but is related to base effects from the prior year's sales tax holidays that are causing outsized gains across multiple categories.

- But there was a notable pickup the proportion of goods categories rising at 2+%, reaching 42% after 40% for a 24-month high, even with 3+% steady at 47%. This is above average and clashes with the overall subdued goods CPI aggregate readings showing fairly tame pressures, but again the jump the last 2 months is potentially base effect related (the share rising 4+% ricked up nearly 1pp to 28%, a 25-month high). This included a dropping out of the tax break for alcohol, toys, games, hobby supplies, and children's clothing. That said, several grocery food categories remained elevated Y/Y.

- For services though the improvement in breadth metrics continued. The proportion of items rising 2+% was 17%, down from 18% prior for a 6-month low, while 3+% was 43% (12-month low, 46% prior) and 4+% 10% (4-month low, 11% prior). A lot of this is shelter and energy-related, both of which are providing a pretty sizeable disinflationary impulse (the latter on carbon tax-related negative base effects), though a few food service related categories saw offsetting base effects here.