STIR: BoE Hike Pricing Picks Up To Week's Highs, ECB Steady Pre-Inflation Data

Sep-27 17:18

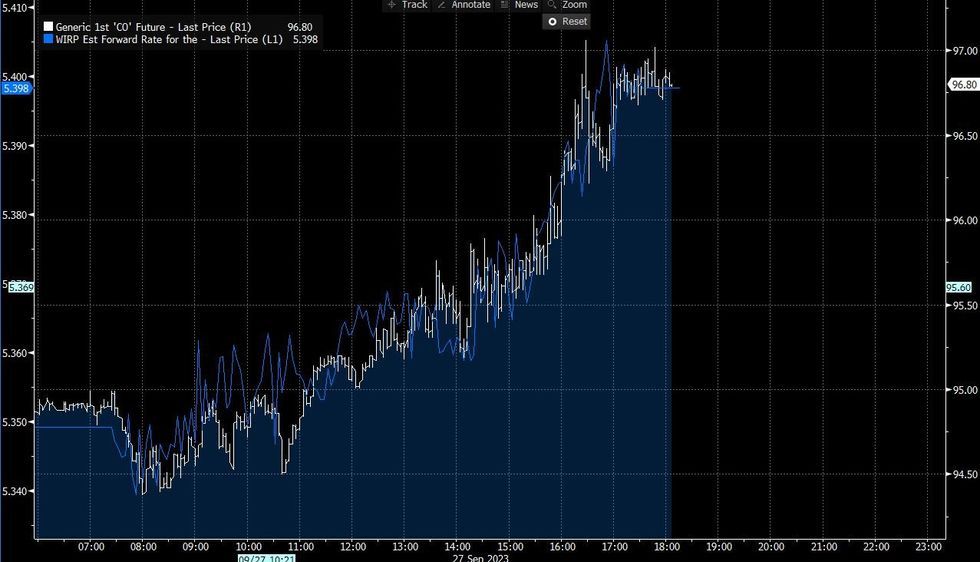

- BoE peak rate pricing picked up 4bp Wednesday to the highest since the the MPC hold on the 21st, with 21bp of further hikes implied to a 5.46% Bank Rate. Though there were no specific catalysts for the move, the rise in implied tracked a weaker GBP and rising oil prices in lockstep intraday. There's 10bp of hikes priced for the Nov 2023 meeting (40% probability of a 25bp hike). Cut pricing fell back sharply, with 73bp of reductions expected in the year following the peak in Mar 2024, vs 80bp at Tuesday's close (and the fewest implied cuts in 2 weeks).

- ECB terminal depo rate pricing was unchanged at 4.05% (5bp of hikes from current levels), with still virtually no chance seen of a hike at the next meeting in October, as we head into the September flash inflation round starting first thing Thursday. There's around 60bp of cuts priced between the end of the tightening cycle in Dec 2023 and end-2024, having been in a range of 60-70bp since late August.

Oil Prices And March 2024 OIS Implied PricingSource: BBG, MNI

Oil Prices And March 2024 OIS Implied PricingSource: BBG, MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US STOCKS: Equities Roundup: Real Estate, Communication Services Lead Rally

Aug-28 17:15

- Stocks are trading mildly higher after midday, near the middle of the session range, a relatively quiet start to the week with London out for a bank holiday. Currently, S&P E-Mini futures are up 28.75 points (0.65%) at 4442.75, Nasdaq up 110.5 points (0.8%) at 13700.4, DJIA up 237.5 points (0.69%) at 34585.55.

- Leading gainers: Real Estate, Communication Services and Materials sectors outperformed Monday, management and development shares supporting the former with CBRE Group +1.6%, CoStar Group +.95%.

- Media and entertainment shares led Communication Services with Warner Bros +2.7%, Charter Communication +2.56%, Paramount +1.2%. Meanwhile Materials led by metals and mining shares: Newmont +1.9%, Freeport McMoRan +1.5%.

- Laggers: Utilities, Health Care and Consumer Discretionary lagged the modest week opener rally. Gas companies weighed on Utilities sector: ATO -1.05%, CMS Energy -1.8%. Health Care: Pharmaceuticals lagged equipment and services: JNJ -1.52%, Merck -1.1% and Bristol Myers -0.95%. Tesla receded 0.7% after making strong gains late last week.

- Technicals: A sharp sell-off on Aug 24 in the E-mini S&P contract reinforces a bearish theme and signals the end of the Aug 18 - 24 corrective bounce. Short-term gains are considered corrective and attention is on support at 4350.00, the Aug 18 low and bear trigger. A break would confirm a resumption of the current bear cycle. Resistance to watch is 4504.75 - the base of a bull channel, drawn from the Mar 13 low - that was breached on Aug 16.

US TSYS/SUPPLY: Review 5Y Auction: On The Screws

Aug-28 17:05

Little reaction to the day's second note auction comes out on the screws: $46B 5Y note auction (91282CHX2): 4.400% high yield vs. 4.400% WI; 2.54x bid-to-cover vs. 2.60x in the prior month

- Indirect take-up at 67.92% vs. 64.38% prior; Direct take-up 18.25% vs. 22.13% prior; Primary dealer take-up 13.83% vs. 13.49%.

- The next 5Y auction is tentatively scheduled for Sep 27.

US TSYS: US TSY 5Y NOTE AUCTION: HIGH YLD 4.400%; ALLOTMENT 32.63%

Aug-28 17:01

- US TSY 5Y NOTE AUCTION: HIGH YLD 4.400%; ALLOTMENT 32.63%

- US TSY 5Y NOTE AUCTION: DEALERS TAKE 13.83% OF COMPETITIVES

- US TSY 5Y NOTE AUCTION: DIRECTS TAKE 18.25% OF COMPETITIVES

- US TSY 5Y NOTE AUCTION: INDIRECTS TAKE 67.92% OF COMPETITIVES

- US TSY 5Y AUCTION: BID/CVR 2.54