MNI EXCLUSIVE: BOC Policy Outlook Interview

Aug-29 19:22

MNI interviews ex-Quebec finance ministry staffer on BOC policy outlook -- On MNI Policy MainWire now, for more details please contact sales@marketnews.com

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

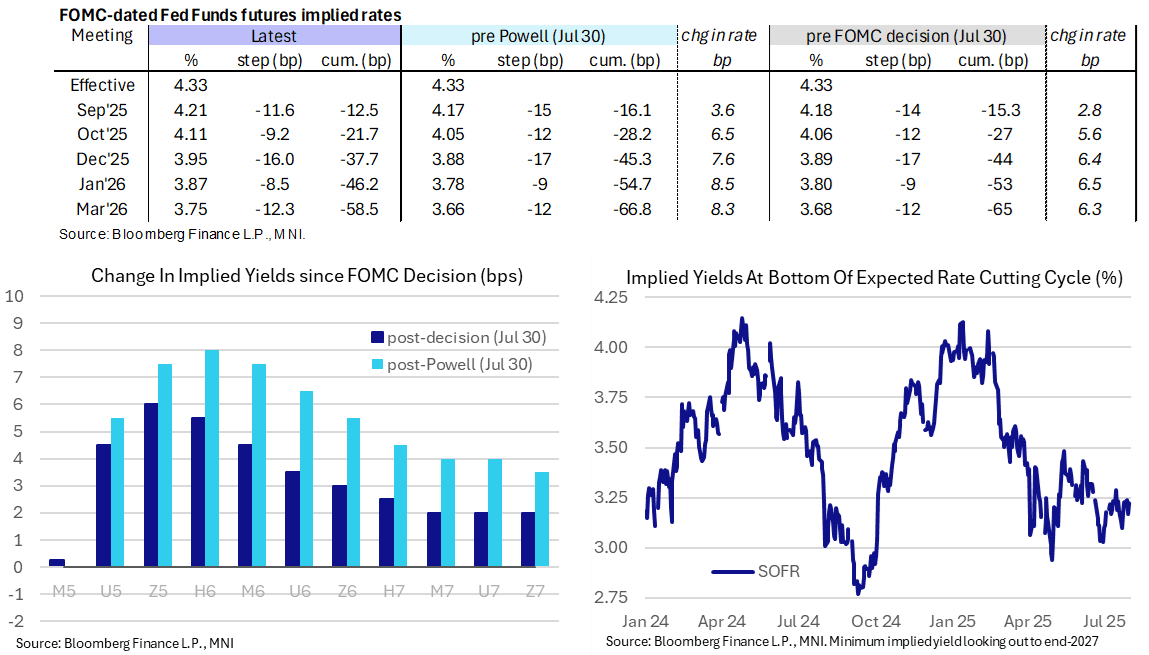

STIR: Hawkish Adjustment Extended Through Presser, 50/50 Sept Cut Odds

Jul-30 19:20

- The hawkish reaction in Fed rates extended throughout Powell’s conference, comfortably more than reversing the small dovish reaction to the initial decision statement.

- Fed Funds cumulative cuts from 4.33% effective: 12.5bp Sep (vs 16bp pre-Powell and 15.5bp pre decision), 21.5bp Oct, 37.5bp Dec (vs 44bp per decision), 46bp Jan and 58bp Mar (vs 65bp pre decision)

- Largest increases in SOFR implied yields through Powell’s press conference are in the H6, +8bp for the same move on the day and +5.5bp since the FOMC decision.

- The terminal implied yield remains in the H7, at 3.225% (+5.5bp on the day) but still easily within the 3.1-3.3% range seen through July.

- The moves were initially driven by Powell seeing modestly restrictive policy as appropriate, saying we have made no decisions about the September meeting and we’re still a ways from seeing where things settle down. Adding to this rhetoric, he later said it’s really hard to say whether will have enough information to cut in September.

US STOCKS: Late Equities Roundup: Retreating As Rate Cuts Cool

Jul-30 19:18

- Stocks sold off, extended lows after projected rate cuts into year end cooled (Dec'25 at -37.6bp vs. -46.6bp on the open) as Fed Chairman Powell continued to answer journals questions. Powell said it's "really hard to say" whether there will be enough information to cut in September."

- Currently, the DJIA trades down 298.93 points (-0.67%) at 44336.2, S&P E-Minis down 27 points (-0.42%) at 6379.75, Nasdaq down 17.5 points (-0.1%) at 21082.38.

- Leading decliners included IDEX -10.47%, Freeport-McMoRan -9.96%, Old Dominion Freight Line -9.36%, Trane Technologies -8.19%, Garmin -7.08%, Palo Alto Networks -5.58%, BXP Inc -5.48%, Verisk Analytics -5.45% and Carrier Global -5.30%.

- On the positive side, Teradyne still up +19.19% after reporting better than expected earnings this morning, Generac Holdings +19.14%, Humana +9.68%, Electronic Arts +7.19%, Bunge Global +5.46%, CVS Health +4.42%, Super Micro Computer +4.21% and American Electric Power Co +4.15%.

- Expected earnings after the close include: Ford Motor Co, Carvana Co, Albemarle Corp, Meta Platforms Inc, Robinhood Markets, QUALCOMM, Guardant Health Inc, Western Digital Corp, Cognizant Technology Solutions, Lam Research Corp, Microsoft, eBay and Allstate.

FOREX: Fed Tips Greenback into Rally Mode, Clearing Key Levels

Jul-30 19:18

- After a shakier start to the European session, the USD soon recovered through NY hours, with strong GDP and ADP Employment Change numbers shortly followed by a resolutely patient outlook from the Fed Chair Powell following the Fed rate decision. Resultantly, the USD Index made light work of resistance into the mid-June highs, testing the 100-dma to the upside for the first time since October 2024.

- Powell's patient approach on policy came despite renewed pressure from the White House to cut interest rates, as he stressed that the FOMC see modestly restrictive policy as "appropriate", despite two dissents at the meeting (Bowman and Waller). The chair also talked down any decisions about the September meeting - stressing that the FOMC is still a ways from seeing where things settle down. As a result, rates pricing through year-end and into the second half of 2026 tightened, helping underpin the dollar rally.

- Markets remained content to sell the EUR through phases of USD strength, resulting in EUR/USD showing well through the late-June lows. This week’s bearish price action has resulted in a move through key support at the 50-day EMA, at 1.1560 - which highlights a stronger reversal and opens 1.1431, a Fibonacci retracement.

- Soft Australian CPI data remained a weight for AUD throughout the day - AUD/JPY is again testing Y96.00, while AUD/USD has shown through the bottom-end of the up-trend channel drawn through the April-July range.

- With the Fed decision now cleared for markets, focus shifts to China's manufacturing and non-manufacturing PMI prints for July, regional German inflation metrics and the Bank of Japan rate decision.

- The BoJ is widely expected to keep its policy rate unchanged at 0.5% for a fourth consecutive meeting, amid signs of easing trade-related uncertainty since its June meeting. Markets will pay close attention to Governor Ueda’s tone during the post-meeting press conference. Ueda has maintained a cautious stance since May, but if the forecasts and risk assessments are revised higher, there’s a high likelihood his tone may shift.