OIL: CITGO Corpus Christi East refinery FCCU2 unit shut unexpectedly – rtrs

CITGO Corpus Christi East refinery FCCU2 unit shut unexpectedly – rtrs

- CITGO reported Friday its FCCU2 unit at the 165,000-b/d Corpus Christi East refinery in Texas experienced a sudden unplanned shutdown due to the loss of a control valve.

- The cause is under investigation while refinery process units are being stabilized.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

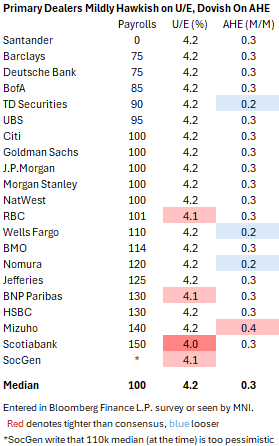

US LABOR MARKET: Payrolls Growth Seen Slowing Again After Public Sector Boost

- Nonfarm payrolls are expected at a seasonally adjusted 104k in July per the broad Bloomberg survey after a surprisingly resilient 147k in June which came along with rare upward revisions.

- The median primary dealer analyst eyes 100k whilst the Bloomberg whisper currently sits at 120k after little reaction to the stronger than expected ADP report for July.

- Government payroll growth is expected to be much softer after a surprise 73k surge in June, which we think was more likely down to seasonal adjustment quirks. There’s a wide range of primary dealer estimates for public payrolls growth in July, from +20k to -55k.

- Consensus sees private sector payrolls rising 100k after a disappointing 74k in June and the breadth of gains should again be watched. 59k of this came from the cyclically insensitive health & social assistance category, whilst roughly as many of the 250 industries increased on the month as those that decreased.

- Payrolls growth should continue to be viewed against long-run breakeven estimates of around the 100k mark although some, such as Deutsche Bank, see this potentially being as low as 50k owing to continued immigration curbs. Indeed, border encounters remain far lower than previous years, albeit plateauing since February, and ICE detention center populations have increased further.

- The unemployment rate is widely expected to tick up a tenth to 4.2% after a surprisingly low 4.11% in June as it pulled back from a cycle high of 4.244% in May. A faster-than-expected deterioration will be required for the final six months of the year to reach the FOMC's June Q4 median projection of 4.5%.

- AHE growth is widely expected at 0.3% M/M after a dovish surprise in June and hawkish surprise in May, which would see the Y/Y inch higher again after seven consecutive unrounded declines. Average hours worked should also be watched from an already low 34.2 in June.

- The full MNI Payrolls Preview will be published tomorrow morning to take into account of the upcoming FOMC decision and press conference.

BOC: MNI BoC Review-July 2025: Dour Outlook Keeps Door Open To Cuts

MNI's review of the July 30 BOC decision is here (PDF):

The Bank of Canada held its overnight rate at 2.75% at the July meeting as widely expected. Overall the decision was taken mildly dovishly by markets, which priced in a slightly higher possibility of a rate cut by year-end.

- While Gov Macklem noted in the press conference that the situation faced by Governing Council hadn’t really changed since the June meeting, the rate decision statement cast a dovish tilt on developments since the start of the year as a whole.

- In particular, the BOC noted “The unemployment rate has moved up gradually since the beginning of the year to 6.9% in June and wage growth has continued to ease. A number of economic indicators suggest excess supply in the economy has increased since January.” Indeed Macklem highlighted that output appeared to be permanently impaired by sustained US-Canada trade tariffs.

- With the BOC emphasizing excess supply increasing, while simultaneously playing down June’s data showing a pullback in the unemployment rate and continued high core inflation, the takeaway from the initial communications leaned dovish. This was reflected in rate markets that at one point post-decision added about one-quarter’s worth of a 25bp rate cut (6bp) by year end.

- A slightly more ambiguous dovish development was the inclusion in the rate statement of "If a weakening economy puts further downward pressure on inflation and the upward price pressures from the trade disruptions are contained, there may be a need for a reduction in the policy interest rate” which appeared in a slightly different form in Macklem’s press conference statement in June. That appeared to ensconce the easing bias more firmly in the official communications.

- That said, overall the communications were fairly balanced, perhaps to be expected given the high degree of uncertainty. Macklem and the statement for instance noted the resilience of the Canadian economy amid US-Canada tariff conflict.

- And as Macklem reiterated, “it's hard to be as forward looking as usual when you've got an unusual amount of uncertainty”, pointing out the multiple scenarios outlined in the updated Monetary Policy Report. He said “we're going to take our decisions one decision at a time, and our future decisions are going to depend what happens in the future.”

- Overall the BOC’s concern about growth appears to keep open the possibility of a rate cut, with some analysts continuing to eye potentially as soon as September – though as before, this is likely to require some bad news in trade developments and / or in the data.

SOFR OPTIONS: Midday Roundup: Two-Way Puts $ Vol Flow

Underlying futures still weaker but off this morning's lows, paring shorts ahead of the FOMC rate annc at the top of the hour. Projected rate cut pricing has cooled vs. early/pre-data (*) levels: Jul'25 at -0.8bp, Sep'25 at -15.2bp (-16.9bp), Oct'25 at -27.1bp (-29.1bp), Dec'25 at -44bp (-46.6bp). Year end projection well off early July level of appr -65.0bp.

- -6,000 0QU5 96.37 puts, 2.5 vs. 96.685/0.12%

- -3,000 SFRH6 96.25 straddles, 44.75

- +5,000 SFRZ5 96.62/97.75 call spds 2.75

- +2,500 SFRU5 95.87 straddles 13.5 over 96.12 calls

- +10,000 SFRH6 95.68 puts, 2.5 vs. 96.275/0.10%