US DATA: BLS Reschedules JOLTS For Thursday, NFPs/CPI Delayed A Few Days

Feb-04 17:01

The Bureau of Labor Statistics has rescheduled the following releases following the government-shutdown related delay - link

- JOLTS to Thu Feb 5 (was Feb 3) at 1000ET

- Nonfarm payrolls to Wed Feb 11 (was Feb 6) at 0830ET

- CPI (and Real Earnings) to Fri Feb 13 (was Feb 11) at 0830ET

- Presumably they both need a little more time to compile CPI - and in any case wouldn't have wanted the inflation and rescheduled Employment Situation report to clash.

- We also expect weekly jobless claims data to be published Thursday as usual.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US STOCKS: Early Equities Roundup: Reconstruction & Recovery Hopes Buoy O&G

Jan-05 16:55

- Stocks are trading stronger despite the spike in geo-political risk following US capture of Venezuela's Maduro over the weekend, DJIA marking new record highs early Monday (49,119.68 at the moment), Energy and Financial sector shares leading advances.

- Currently, the DJIA trades up 727.97 points (1.5%) at 49112.67, S&P E-Mini Futures up 59.5 points (0.86%) at 6960.5, Nasdaq up 225.8 points (1%) at 23462.97.

- Energy sector shares apparently surged on hopes they may benefit from future oil infrastructure reconstruction in Venezuela and potential recovery of assets by Chevron and ExxonMobil (while crude gained slightly in comparison: WTI +.98 at 58.30): SLB Ltd +9.50%, Halliburton +8.82%, Valero Energy +8.31%, Phillips 66 +6.01%, Marathon Petroleum +5.40% and Chevron +4.88%.

- Financial sector shares followed suit, broken down in two categories (services and banks): Coinbase Global +7.25%, Robinhood Markets +6.19%, Moody's +5.71%, Block +5.26% and Interactive Brokers Group +5.21%; Goldman Sachs Group +4.18%, Bank of New York Mellon +4.02%, Citigroup +3.93% and Blackrock +3.69%.

- Reminder, the next earnings cycle kicks off in earnest next week with Bank of NY Mellon, JPM reporting on Tuesday January 13, Bank of America, Wells Fargo and Citigroup on Wednesday, Goldman Sachs, Blackrock and Morgan Stanley on Thursday.

- Conversely, Utilities and Health Care sector shares underperformed in the first half: Constellation Energy -3.81%, NRG Energy -3.68%, Sempra -3.28%, NiSource -2.80% and Vistra -2.79% weighed on the former. Pharmaceuticals weighed on the Health Care sector: AbbVie -4.53%, Eli Lilly & Co -3.79%, Gilead Sciences -3.48%, Biogen -2.83% and Amgen -2.34%.

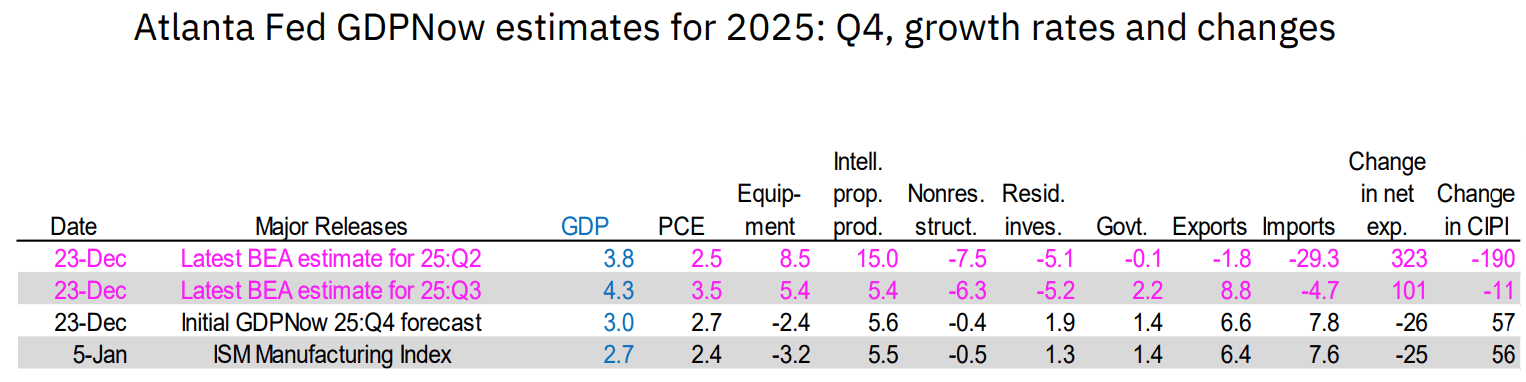

US DATA: Atlanta Fed GDPNow Estimate Downgraded After Soft ISM Manufacturing

Jan-05 16:47

The Atlanta Fed's GDPNow estimate for Q4 2025 has been marked down to 2.7% Q/Q SAAR (2.68% unrounded) from 3.0% in its prior update on Dec 23 (2.97% unrounded) and 4.3% in Q3.

- The major data development between then and now was today's relatively soft ISM Manufacturing index, which saw the growth forecast for equipment investment downgraded to -3.2% Q/Q SAAR from -2.4% (and +5.4% in Q3), while personal consumption expenditures were downgraded to 2.4% from 2.7% (3.5% in Q3).

- Combined, those two downgrades shaved off 0.26pp from the overall GDP estimate.

- We get the next GDPNow update on Thursday, after the publication of ISM Services, international trade, and wholesale trade among other data points.

FOREX: Dollar Holds ISM Losses, But Major Pairs Still Rangebound

Jan-05 16:33

Headed through the London close, the USD Index trades close to the lowest levels of the day, leaving markets holding close to the entirety of the ISM-triggered move. This keeps EURUSD above 1.17 and GBPUSD above 1.35 through the close. Despite the impressive intraday reversal, both pairs are still well inside the recent range, however, leaving notable resistance levels untroubled for now.

- For some, today marks the first full trading session of the year, and it is worth noting the somewhat erratic price action in GBPUSD headed through the WMR fix both today, Friday and (to a lesser extent) on December 31st, all of which saw a sizeable bid in GBP (excepting Dec31, where GBP was sold) through the fix, before a partial reversal.

- AUDUSD's clearance of 0.67 ahead of the close today keeps the short-term outlook bullish to keep focus on the bull trigger into 0.6728, the Dec 29 and range high. CPI data due Wednesday should prove influential here, marking the new monthly series and a direct input into the February 3rd RBA decision.

Trending Top

Jun-25 06:23