US TSY FLOWS: BLOCK BUY TYM6

BUY 3799 of TYM6 traded at 108-23+, post-time 13:01:31 AEST (DV01 $243,590). The contract closed at ...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

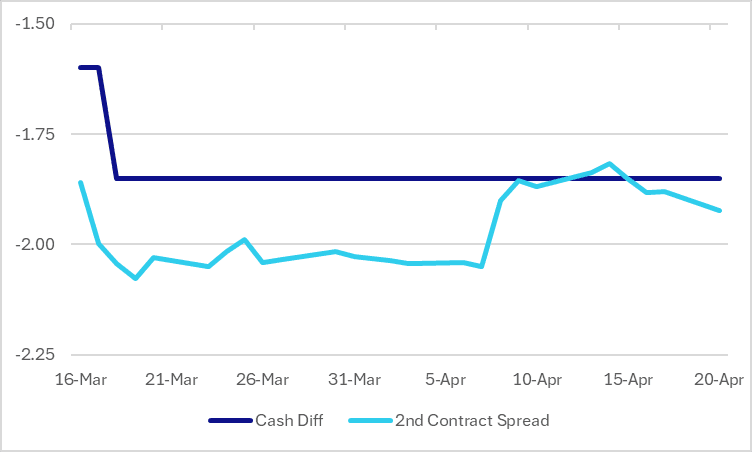

STIR: Will Market Fade Front End Pricing: RBNZ Vs RBA

While the next move by the RBA and RBNZ is most likely tightening, potential divergent timelines in our opinion have created a relative value opportunity in the OIS market.

- The RBA is expected to front-load tightening, driven by its view that demand has been too strong and is behind the recent inflation rise. It appears less data-dependent in the near term and inclined to reverse prior easing.

- The RBNZ, in contrast, has been signalling patience and gradualism, with future moves heavily dependent on incoming data. RBNZ Governor Breman was very clear that the MPC is focused on the medium-term and that the OCR path will depend on how growth and expectations develop and impact medium-term inflation.

- While markets broadly align with expectations of rates returning to around 3%, they appear to pricing hikes too aggressively and too early, with a full hike by July versus a more RBNZ-consistent September timeframe.

- This mismatch creates a potential opportunity: NZ front-end rates look too hawkish relative to the RBNZ’s guidance, especially versus Australia.

- One possible expression that could be considered is to fade front-end RBNZ pricing versus the RBA by way of the 2nd meeting date contract spread. A paid viewpoint of the Jun-26 RBA versus Jul-26 RBNZ OIS spread around current levels (-192bps), with scope to gravitate towards -210bps possible if the above macro views unfold.

Figure 1: NZ-AU – Cash Differential Vs. 2nd Meeting Date Contract Spread

Source: Bloomberg Finance LP / MNI

NEW ZEALAND: Little Iran Impact Expected In Q1 CPI Data, Consensus At 2.9%

Q1 CPI prints on 21 April with the RBNZ’s measure of core from its sector factor model following later that day. Given materially higher fuel prices due to the Iran War were not seen until mid-March, there’s likely to be little impact on Q1. The RBNZ forecast Q1 inflation of 2.8% y/y in February but revised that to 3.0% at its April decision given recent data and geopolitical developments. Q2 CPI data are likely to show a larger effect from the conflict with the RBNZ forecasting headline at 4.2% but there will be updates at the 27 May meeting. It is focused on the medium-term effect though.

- Bloomberg consensus is forecasting Q1 headline CPI to rise 0.8% q/q and 2.9% y/y following Q4’s 0.6% q/q & 3.1% y/y, just above the top of the RBNZ’s 1-3% band. Projections range from 0.7-1.1% q/q and 2.8-3.3% y/y.

- Most quarterly forecasts are around 0.7-0.8% q/q. ANZ and Westpac expect 0.7% q/q with annual inflation rising 2.9% and 2.8% respectively. ASB and BNZ project 0.8% q/q but 2.9% and 3.0% y/y. Kiwibank is higher at 3.1% y/y.

- ASB believes that inflation will remain around 4% for most of this year with it not returning to the target band until mid-2027. As a result, it is forecasting rates hikes at every meeting from September until the OCR reaches 3.25% in February 2027.

- In February, the RBNZ forecast Q1 non-tradeables inflation to rise 1.0% q/q and 3.4% y/y. ANZ is in line with the central bank but the others are lower with ASB & Westpac expecting 0.8% q/q and BNZ 0.9% q/q.

- Tradeables CPI projections are in a wide range of 0.2% to 0.8% q/q with consensus at 0.6%. BNZ is in line with consensus, while ASB is higher at 0.7% but ANZ and Westpac expecting 0.4% and 0.2% q/q respectively.

CROSS ASSET: Risk Sentiment Off Earlier Lows As US/Iran Developments Eyed

Risk sentiment is comfortably away from earlier Asia Pac lows, as markets await further developments around the US/Iran conflict. US equity futures have pared losses back to around 0.50% for Eminis (we opened down around 0.9%). Likewise for the USD, which is still up modestly for the session, but comfortably off earlier highs. AUD/USD got to lows of 0.7117, but is now back to 0.7150. Oil futures remain +5% higher, but Brent was last near $94.75/bbl, after touching $97.50/bbl in the first part of trade.

- Market price action still appears to be trading conflict risks with a glass is half full approach, i.e. we are still closer to the end of the conflict rather than significant further escalation.

- Near term focus will likely rest on whether we see further action around the US naval blockade, after the earlier incident of firing and boarding an Iranian ship. Iran officials stated they responded by launching drone attacks against US ships. Further actions of this nature are likely to drive fresh market risk off.

- Beyond that will be focus on whether further talks between both sides take place, with conflicting reports as to whether talks will go ahead. This comes ahead of the 10-day ceasefire period ending on Apr 22.