CRYPTO: Bitcoin-Could Not Go Up As The USD Fell, But It Is Falling As It Bounces

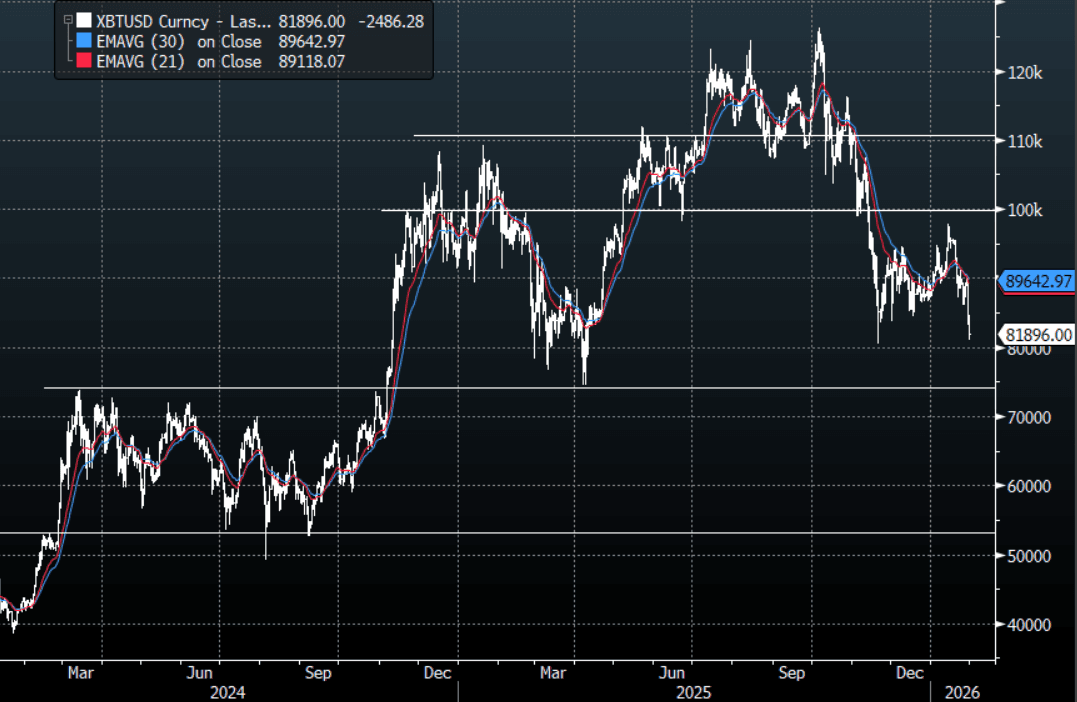

Bitcoin had a range overnight of $83,240.52 - $88,338.31, Asia is currently trading around $81900, -3%. Bitcoin and Crypto tried really hard to participate in the “debasement trade” but could not break higher as the Metals went parabolic and the USD cratered. Yet the first sign of a bounce in the USD and Crypto gets hammered lower, this is not the price action of an asset that has put in its low. The price action does not look great and it looks set to test the very important $75-$80k area. The $75k area remains of key interest as it is the break even point for MicroStrategy Bitcoin holdings the largest Bitcoin Treasury Company and the market will be watching to see if there is any signs of it having to sell out any of its inventory should it break below there. Bitcoin remains in a Bear trend and a break back below $75k could signal a deeper pullback to the $50-$60 area.

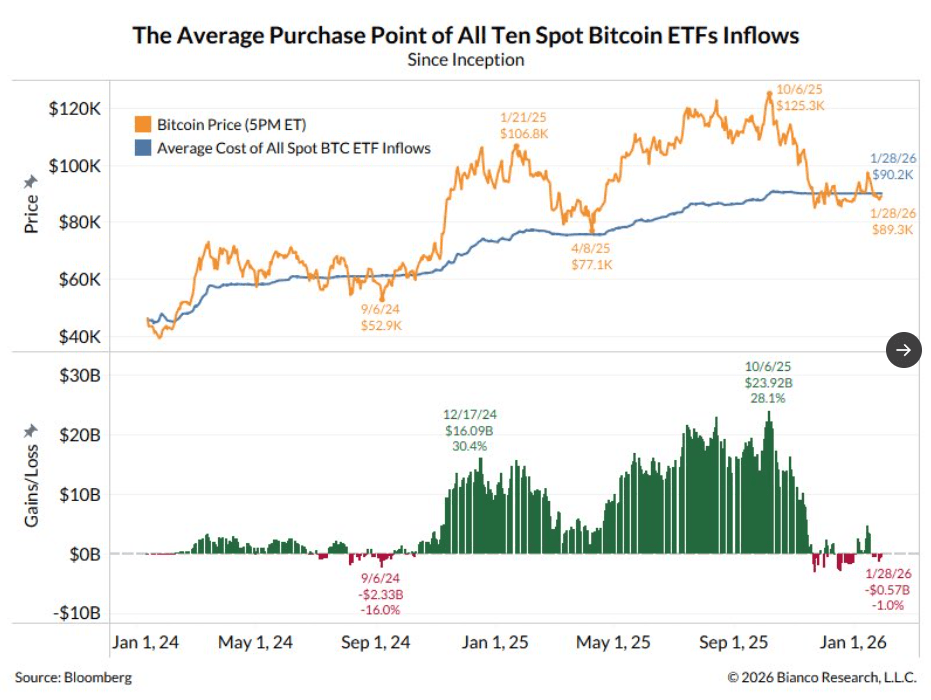

- Jim Bianco on X: “Bitcoin breakeven update. The average purchase for all the flows into all the spot $BTC since inception (January 2024) is $90,200. With today’s plunge, the AVERAGE $BTC ETF holder is about $5,000 (or ~7% underwater).” See graph below.

- “The largest Digital Asset Treasury (DAT) is Strategy (formally Microstrategy, $MSTR) has an average purchase price of $76,020.”

- Treasury companies have been consistently adding bitcoin but the price continues to trade heavy, is there a point at which they need to start paring back ?

- Bitcoin’s Average True Range(ATR) for the last 10 Trading days: $3,081

Fig 1: Bitcoin Average Purchase Point Of ETF Inflows

Source: MNI - Market News/Bloomberg Finance L.P/Bianco Research

Fig 1: Bitcoin spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CHINA DATA: Activity Returns To Growth, Export Orders Continue Contracting

The official China PMIs for December showed an improvement in activity with both manufacturing and non-manufacturing returning to growth. The composite PMI rose to 50.7 from 49.7, which had been the first move below the breakeven 50-level since December 2022.

- The manufacturing PMI improved to 50.1 up from 49.2 and higher than expected. While one month doesn’t make a trend, December may signal the end of the contraction in activity in the sector that began in April. Confidence in the outlook picked up to 55.5 from 53.1.

- The recovery was driven by higher output but also new orders which returned to positive territory at 50.8. Orders growth was driven by the domestic economy with export orders continuing to contract but at a slower pace than most of the year.

- The outcome was confirmed by the RatingDog December manufacturing PMI at 50.1 up from 49.9.

- Non-manufacturing also shifted slightly into growth territory at 50.2 from 49.5, which was also stronger than consensus. Most components continued to contract though but at a slower pace than last month but expectations were very positive at 56.5. New orders remained weak at 47.3 but up from 45.7, while export orders deteriorated to 47.5 from 47.9.

- Manufacturing and non-manufacturing selling prices continued to decline in December despite positive input cost inflation. This signals that China’s inflation rate is likely to remain close to zero.

MNI: CHINA DEC RATINGDOG MANUFACTURING PMI 50.1 VS 49.9 IN NOV

- CHINA DEC RATINGDOG MANUFACTURING PMI 50.1 VS 49.9 IN NOV

MNI: **CHINA DEC MANUFACTURING PMI 50.1 VS 49.2 IN NOV

- **CHINA DEC MANUFACTURING PMI 50.1 VS 49.2 IN NOV