INDONESIA: BI Stares at 17,000 as Independence Concerns Rise Again

Mar-13 04:01

- USDIDR steadily climbed this week towards a key psychological level as external shocks and domestic fiscal worries collided.

- The Rupiah has been under pressure again this week, despite strong BI intervention earlier.

- The primary narrative has been record-high oil prices, USD strength, and renewed investor jitters over the independence of Bank Indonesia in the face of a challenging market backdrop.

- The pair broke weaker Monday, triggered by the escalation in the Strait of Hormuz, which immediately translates to a higher cost of imported oil.

- BI intervened in both spot and domestic non-deliverable forward (DNDF) markets mid-week but only briefly stabilized the pair around 16,860.

- This as the release of FX reserves data shows the pace of their use is growing.

- As oil rose to US$100 USDIDR broke north of 16,900 with forecasters worrying about scenarios where the fiscal deficit expands significantly to cover fuel subsidies.

- Today USDIDR is weaker again, up +47 to be near 16,936 / 16942 and but only sitting on modest Rupiah losses for the week.

- The moves have echoes of 2022 when the BI was forced to raise rates to defend the currency. It's different this time given the Government of the day and their desire for lower rates to support growth.

- Next week the BI meets and questions of its independence are being raised again.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

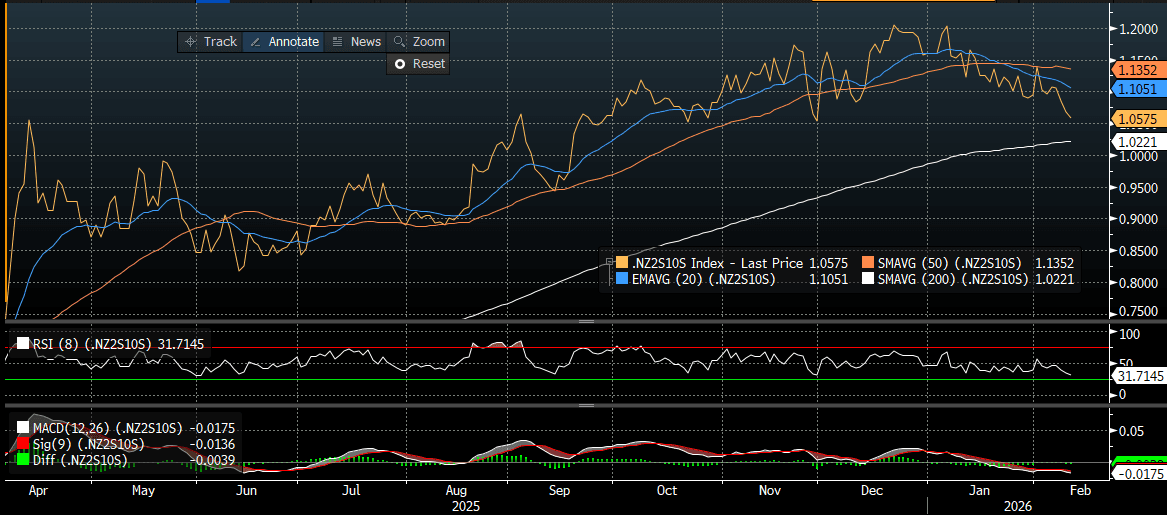

BONDS: NZGBS: Bull-Flattener Leaves Curve At Its Flattest Since Nov

Feb-11 03:58

NZGBs closed showing a bull-flattener, with benchmark yields 2-4bps lower.

- Nevertheless, NZGBs underperformed ACGBs with the NZ-AU 10-year yield differential 2bp wider on the day.

- There has no cash US tsys dealings in today’s Asia-Pac session, with Japan out on holiday.

- (Bloomberg) “New Zealand’s government has started an independent review of New Zealand’s monetary policy response to the Covid-19 pandemic. Purpose of the review is to identify lessons New Zealand could learn to improve the monetary policy response to future major events.”

- Swap rates closed 2-5bps lower, with the 2s10s curve flatter. At 1.06, the curve is at its flattest since late November (see chart).

- RBNZ-dated OIS pricing closed little changed across meetings. No tightening is priced for February, while December 2026 assigns 43bps.

- The local calendar will be light until Friday's release of BusinessNZ Manufacturing PMI, Net Migration and RBNZ Inflation Expectation data.

- Tomorrow, the NZ Treasury plans to sell NZ$250mn of the 1.50% May-31 bond and NZ$200mn of the 4.5% May-35 bond.

Bloomberg Finance LP

OPTIONS: +$3bn In USD/JPY Options So Far Today, O/N Vol Elevated Ahead Of NFP

Feb-11 03:45

In the FX option space, JPY volumes have dominated so far in Wednesday trade, with around $3.1bn in total volumes so far. This is 46.6% of total volumes, per DTCC via BBG and comes despite onshore markets in Japan being out today. Next on the volumes list is USD/TWD with 10.8% of total volumes. AUD/USD, which has broken above 0.7100 for the first time since 2023 just under $600mn in FX options volumes so far today (around 9.5% of total).

- For USD/JPY, the larger volume transactions ($100mn or more), are mostly for puts, with a variety of strike levels. A 143 strike, expiry end April this year was executed for +200mn per DTCC. This comes as USD/JPY continues to unwinds its pre-election bounce, amid signs that government wants to earn the markets trust around fiscal policy etc. Softer US yields are also weighing on USD/JPY.

- USD/JPY risk reversals are rolling back over, but are above late Jan lows. The 1 month is around -1.64.

- In the vol space, overnight vol is elevated near 16.45%, which reflects the upcoming US payrolls print later. Other implied vol measures are sub 10%.

CHINA: CPI Misses With LNY Distortions

Feb-11 03:22

- CPI YoY in January rose just 0.2%, missing the consensus forecast of 0.4% and down from 0.8% in December. The MoM edged up 0.2%, matching the December pace but falling short of the 0.3% forecasts. Core CPI slowed to 0.8% YoY, down from 1.2% driven by base effects and food prices.

- PPI remained negative, reflecting continued pressure on industrial profitability. Down 1.4% YoY, it was an improvement over December's 1.9% decline. However this is the 40th consecutive month of declines, reflecting weak domestic demand and overcapacity in manufacturing.

- Calls for monetary policy intervention remain with the PBOC pledging in its latest quarterly report to employ “flexible and efficient” cuts to interest rates and RRR to maintain an accommodative financial environment emphasizing a deepening coordination with fiscal policy to lower financing costs and boost domestic demand, according to Shanghai Securities News. Undoubtedly expectations will grow ahead of the National People's Congress in March.

- China bond futures are up modestly, the 10-Yr up +.06 at 108.53 and the 2-Yr flat at 102.47. The 2-Yr NDIRS has broken below major moving averages and could test the December lows.

- CGB 10-Yr is modestly lower in yield at 1.80% following liquidity injections this morning during the OMO.

- Look for further liquidity support ahead of the LNY and the 10-Yr to test below 1.80% .

CNY 2-Yr NDIRS vs 20, 50, 100 and 200-day EMA

source: Bloomberg Finance LP / MNI