FED: Beige Book: Very Slight Improvement In Labor Market (2/3)

The February Beige Book showed a very slight improvement in the employment column compared with Janu...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDJPY TECHS: Gains Considered Corrective For Now

- RES 4: 159.45 High Jan 14 and the bull trigger

- RES 3: 159.23 High Jan 23

- RES 2: 157.43 Low Jan 23

- RES 1: 155.76 50-day EMA

- PRICE: 155.54 @ 16:11 GMT Feb 2

- SUP 1: 152.10 Low Jan 27 and the bear trigger

- SUP 2: 151.98 38.2% of the Apr 22 ‘25 - Jan 14 bull cycle

- SUP 3: 151.54 Low Oct 29 ‘25

- SUP 4: 150.99 Trendline support drawn from the Apr 22 ‘25 low

Short-term trend conditions in USDJPY are unchanged and a bear cycle remains intact. However, a corrective cycle is in play and the latest recovery is allowing a recent oversold condition to unwind. Firm resistance to watch is at 155.76, the 50-day EMA. A clear break of this average would signal a possible bullish reversal. Key short-term support has been defined at 152.10, the Jan 27 low. A break would resume the recent downtrend.

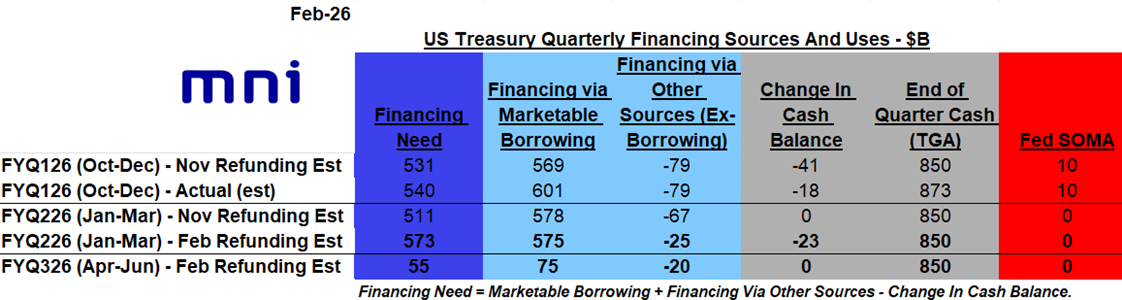

US TSYS/SUPPLY: Quarterly Financing Estimates Set To Come In Largely Steady

The February Refunding round starts at 1500ET today with the US Treasury’s update on financing requirements for the current (Jan-Mar) and next (Apr-Jun) quarters, at which is expected to largely maintain its borrowing projections for the current quarter.

- MNI’s expectations are in the table below. We would say that risks to our estimates are largely to the downside, i.e. Treasury expects to borrow/finance less than we have penciled in.

- Oct-Dec marketable borrowing will have been around $600B, not far from the original $569B estimate made in the November refunding round, and that is set to fall to around $575B in the Jan-Mar quarter (basically unchanged from the previous estimate; we’ve seen estimates ranging from $450-650B).

- The April-June quarter sees the lowest borrowing of the year as usual, which we estimate to come in at $75B (we’ve seen ranges from slightly negative, to over $200B).

- These figures assume that Treasury continues to target a $850B end-quarter TGA cash pile.

- Below are some sell-side expectations.

- CIBC: $640B borrowing requirement Jan-Mar, $96B Apr-Jun (assuming $850B end-quarter TGA).

- Deutsche: Net borrowing of $555B in Jan-Mar, $25B in Apr-Jun (assuming $850B cash end quarter TGA).

- Goldman Sachs: marketable borrowing of $640bn for Q1. Assuming a $850bn TGA target, for Q2 expect marketable borrowing of $290bn

- JPMorgan: $498B in marketable borrowing in Q1, $102B in Q2, assuming $850B TGA

- TD: $561bn in marketable borrowing for Q1 and $19bn in Q2. We assume a TGA target at $850bn for both quarters.

- Wells Fargo: Marketable borrowing $609B in Q1, $228B in Q2

US: FED Reverse Repo Operation

RRP usage inches up to $10.415B with 8 counterparties this afternoon vs. $9.629B Friday. Compares to December 12 low of $0.838B (lowest level since mid-March 2021); this years highest excess liquidity measure: $460.731B on June 30.